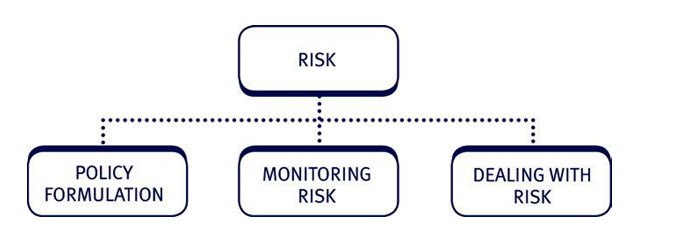

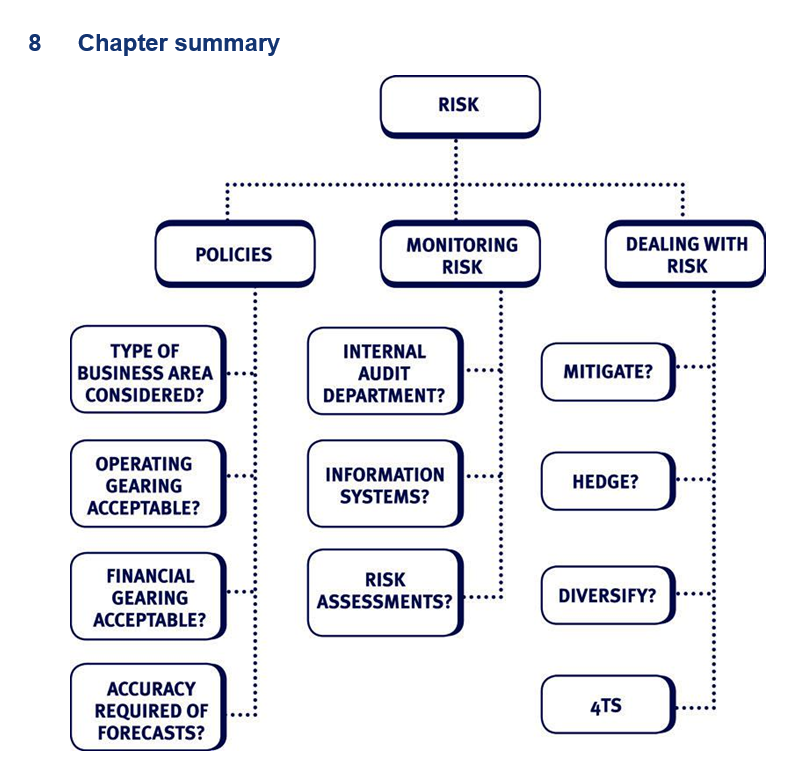

Risk policy formulation

An important part of the financial manager’s role and responsibility is considering how risk is to be managed.

The control and mitigation of risk costs money and takes up management time, so it is critical that we can understand the benefits of risk management and compare these to the costs to assess whether a risk management strategy is worthwhile.

Strategic Business Leader (SBL) covered managing and controlling risk in some detail. This section initially introduces an overview of risk management in relation to capital investment projects, then explains some specific examples of risks. More detailed techniques for risk management, such as the use of derivatives and Value at Risk (VaR), are covered later in the chapter.

Student Accountant article

Read the examiner’s ‘Risk Management’ article in the Technical Articles section of the ACCA website for more details on why companies need to manage risk.

The theory of risk management

Risk management is about decisions made to change the volatility of returns a corporation is exposed to, for example changing a company’s exposure to floating interest rates by swapping them to fixed rates for a fee.

Since business is about generating higher returns by undertaking risky projects, important management decisions revolve around which projects to undertake, how they should be financed and whether the volatility of a project’s returns (its risk) should be managed.

The volatility of returns of a project should be managed if it results in increasing the value to a corporation. Given that the market value of a corporation is the net present value (NPV) of its future cash flows discounted by the return required by its investors, then higher market value can either be generated by increasing the future cash flows or by reducing investors’ required rate of return (or both).

A risk management strategy that increases the NPV at a lower comparative cost would benefit the corporation.

Risk and stakeholder conflict

- Shareholders will invest in companies with a risk profile that matches that required for their portfolio.

- Management should thus be wary of altering the risk profile of the business without shareholder support.

- An increase in risk will bring about an increase in the required return and may lead to current shareholders selling their shares and so depressing the share price.

- Inevitably management will have their own attitude to risk. Unlike the well-diversified shareholders, the directors are likely to be heavily dependent on the success of the company for their own financial stability and be more risk averse as a consequence.

Risk and policy decisions

The financial manager will need to make policy decisions in the following areas:

- Type of business area

- Operating gearing

- Financial gearing

- Accuracy of forecasts.

Risk and policy decisions

Type of business area

Based on the risk appetite of the firm, decisions must be taken about those types of activity suitable for investment. This will involve decisions about the acceptability of:

- economic volatility of the industry

- degree of seasonality

- intensity of competitor action.

Operating gearing

The level of operating gearing of the firm is the proportion of fixed costs to variable in the cost structure. Whilst some industries are destined to have higher levels of operating gearing than others (compare the travel industry with manufacturing for example), policy decisions about what level is acceptable will drive choices about factors such as:

- outsourcing v. providing internally

- leasing v. buying

full-time staff v. freelance providers

Financial gearing

More fully discussed elsewhere, increasing debt levels can reduce the cost of finance but increases the risks of bankruptcy as the same time. Directors must decide what level of gearing they are prepared to accept.

Accuracy of forecasts

The success of any planned investment programme will rely heavily on the accuracy of forecasts of future cash flows (in and out) and an NPV assessment also relies on an accurate calculation of the discount rate.

The sensitivity of these forecasts can be calculated, and the probability of the variation assessed, but in the end the directors must decide what level of risk they are willing to accept in order to accept or reject the project.

2 The risk framework

All projects are risky. When a capital investment programme commences, a framework for dealing with this risk must be in place.

This framework must cover:

- risk awareness

- risk assessment and monitoring

- risk management (i.e. strategies for dealing with risk and planned responses should unprotected risks materialise).

Risk awareness

In appraising most investment projects, reliance will be placed on a large number of estimates. For all material estimates, a formal risk assessment should be carried out to identify:

- potential risks that could affect the forecast

- the probability that such a risk would occur. Risks may be:

- strategic

- tactical

Once the potential risks have been identified, a monitoring process will be needed to alert management if they arise.

Different types of risk

Strategic risks are those affecting the overall direction and outcome of the project, such as changes in macroeconomic factors or changes in corporate policies.

Tactical risks affect the way the various parts of the project are interlinked, the way resources are acquired or the way in which the business functions involved in the project are run.

Operational risks are those affecting the day to day running of the project.

Examples of risk for an investment project

Some strategic, tactical and operational risks that would affect the estimates on a typical investment project might be:

Strategic:

- brand awareness in the new sector

- risk of recession

- political changes.

Tactical – changes to forecasts based on:

- supply chain changes

- major payment timings

- intended sales of machinery

- contractor overruns on time or amounts spent. Operational – changes occurring because:

- production breakdown

- breakdown of the supply chain

- failure of the distribution network

failure to recruit staff with the necessary skills

Risk assessment and monitoring

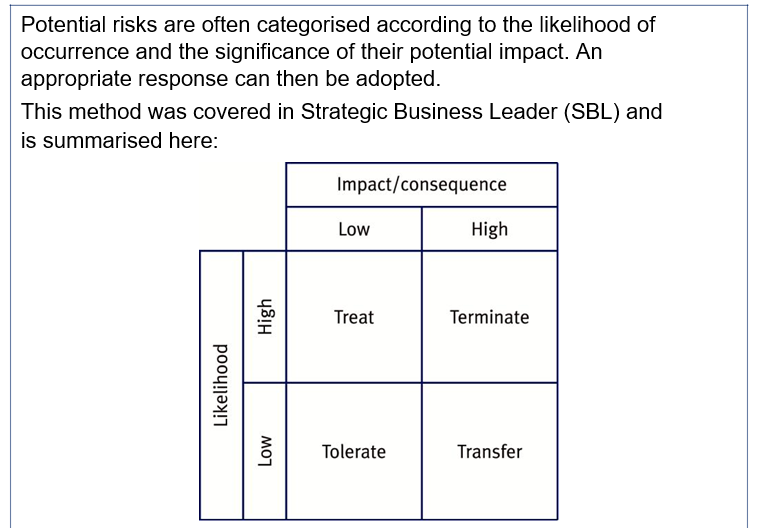

A useful way to manage risk is to identify potential risks (usually done in either brainstorming meetings or by using external consultants) and then categorise them according to the likelihood of occurrence and the significance of their potential impact.

Decisions about how to manage the risk are then based on the assessment made.

These assessments may be time consuming and the executive will need to decide:

- how they should be carried out

- what criteria to apply to the categorisation process and

- how often the assessments should be updated.

The essence of risk is that the returns are uncertain. As time passes, so the various uncertain events on which the forecasts are based will occur. Management must monitor the events as they unfold, reforecast predicted results and take action as necessary. The degree and frequency of the monitoring process will depend on the significance of the risk to the project’s outcome.

Specific risk assessment and monitoring methods Internal audit

Many companies set up internal audit departments to assist them in their responsibility to monitor and manage risk.

It is not the job of the internal audit department to monitor results and perform risk assessments, but they can provide valuable support in the creation and successful running of such monitoring systems.

Information systems

Information systems play a key part in effective risk monitoring. Once risk factors have been identified, information systems must be put in place to ensure that any changes affecting project estimates are:

- recorded

- brought to the attention of the responsible manager

- dealt with in an appropriate way.

This will usually include:

- management information systems (MIS)

- executive information systems (EIS).

These systems are expensive to set up and the executive team must decide on the extent to which they wish to use them and the scope required.

The difference between them is:

- Management information systems – feeding back operational data to allow for action to prevent or mitigate risk.

- Executive information systems – bringing senior executives up-to-date with external information such as competitor action, currency fluctuations and economic forecasts as well as providing summarised operational data.

3 Risk management

Strategies for dealing with risk

Risk can be either accepted or dealt with. Possible solutions for dealing with risk include:

- mitigating the risk – reducing it by setting in place control procedures

- hedging the risk – taking action to ensure a certain outcome

- diversification – reducing the impact of one outcome by having a portfolio of different ongoing projects.

More on mitigation, hedging and diversification Mitigation

- All companies should have in place a comprehensive system of controls. These controls play an essential role in good corporate governance and mitigate risk by working to prevent, or detect and correct potential risks before they become a problem.

- Management would be expected to implement controls over most material risks subject to the following:

– The cost of the control should not be disproportionate to the potential loss.

– For non-routine events it may be more practical to devise a specific strategy for dealing with the risk should it arise.

Hedging the risk

- Hedging is a strategy, usually some form of transaction, designed to minimise exposure to an unwanted business risk, commonly arising from fluctuations in exchange rates, commodity prices, interest rates etc.

- It will often involve the purchase or sale of a derivative security (such as options or futures) in order to reduce or neutralise all or some portion of the risk of holding another security. This is dealt with in detail later in this chapter.

- A perfect hedge will eliminate the prospects of any future gains or losses and put the company into a risk-free position in respect of the hedged risk.

- This strategy may be chosen where the downside risk would have serious negative consequences for the firm, and the costs of hedging (including the chance to participate in any upside) are outweighed by the benefits of certainty.

Diversification

- This involves reducing the impact of one outcome by having a portfolio of different ongoing projects.

- Within the context of a single project, this may take the form of selling to a number of different customers to reduce reliance on a single one or sourcing from a number of different suppliers.

- For businesses operating internationally, it may involve locating key parts of the business in different countries.

- Diversification would be chosen wherever reliance on a single source of resource has been identified as a potential risk.

The 4T approach to risk management

A company can adopt four possible approaches to a risk, known as the

4T approach:

- Tolerate it.

- Transfer it.

- Terminate it.

- Treat it (i.e. by mitigating it, hedging or diversifying).

Appropriate responses would be matched to the risk as shown above.

Tolerate

Accept that the risk might occur but do not put in place any systems to manage it. For example, a power failure may cause a serious production stoppage but few firms would consider acquiring a back-up generator. However a call centre, heavily reliant on its computer system, may decide that it would be worthwhile.

Transfer

The risk is passed on elsewhere. This can be achieved by activities such as:

- insuring against the risk (for example against the risk of fire)

- taking out fixed price contracts (such as with construction companies or suppliers)

- outsourcing production (buying in from a range of providers rather than relying on own production).

Terminate

This can mean deciding against the activity altogether, but in the context of a project, would mean identifying at what point it would be better to ‘bail out’ rather than proceed with the project – i.e. when the NPV of the revised future cash flows is negative.

Treat

A risk is treated when controls are in place to reduce either:

- the likelihood or

- the consequences of the event occurring.

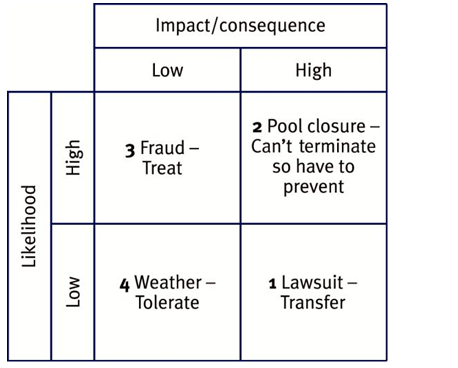

Illustration of the 4T approach

- A leisure company has just approved a large-scale investment project for the development of a new sports centre and grounds in a major city. The forecast NPV is approximately $6m, assuming a time horizon of five years, steady growth in business and constant returns in perpetuity thereafter.

Required:

Explain what the company would need to do, to ensure that the risks associated with the project are properly managed?

- A number of specific risks have been identified:

- A potential lawsuit may be brought for death or injury of a member of the public using the equipment. No such event has ever occurred in the company’s other centres.

- The loss of several weeks’ revenue from pool closure for repairs following the appearance of cracks in the infrastructure. This has occurred in several of the other centres in the past few years.

- Income fraud as a result of high levels of cash receipts.

- Loss of playing field revenue from schools and colleges because of poor weather.

Required:

Suggest how these risks could be best managed.

Solution

- (i) Risk awareness – The potential risks associated with the project at strategic, tactical and operational levels should be identified. The fact that the company has carried out such projects before should make this task relatively straightforward.

- Risk monitoring – Information systems should be put into place to ensure that all material risk factors are continuously monitored. The impact of any changes likely to the affect the success of the project can then be identified and action taken as necessary. The forecast growth and return figures are undoubtedly critical to the success of the project and the underlying assumptions such as economic predictions, local demographics, competitor activity and recreational trends should be carefully monitored and assessed.

- Risk management – Risks identified can be categorised according to the likelihood of occurrence and the significance of the impact, in order to decide how best to manage them.

- The identified risks could be mapped as shown below:

- The risk of a lawsuit should be dealt with my taking out indemnity insurance. The risk is then transferred to the insurance company.

- The risk of pool closure is serious and since a provision of a pool is clearly essential for the sports centre, the risk must be treated instead. This would mean putting in place a series of controls over the building process to prevent later cracks from occurring.

- The risk of fraud is exactly the type of risk that a good internal control system would be designed to prevent.

Bad weather will always be a risk when dealing with outdoor activities and is probably best accepted and the lost revenues factored into the initial forecasts.

Specific types of risk

Political risk

Political risk is the risk that a company will suffer a loss as a result of the actions taken by the government or people of a country. It arises from the potential conflict between corporate goals and the national aspirations of the host country.

This is obviously a particular problem for companies operating internationally, as they face political risk in several countries at the same time.

Sources, measurement and management – Political risk Sources of political risk

Whilst governments want to encourage development and growth there are also anxious to prevent the exploitation of their countries by multinationals.

Whilst at one extreme, assets might be destroyed as the result of war or expropriation, the most likely problems concern changes to the rules on the remittance of cash out of the host country to the holding company.

Exchange control regulations, which are generally more restrictive in less developed countries for example:

- rationing the supply of foreign currencies which restricts residents from buying goods abroad

- banning the payment of dividends to foreign shareholders such as holding companies in multinationals, who will then have the problem of blocked funds.

Import quotas to limit the quantity of goods that subsidiaries can buy from its holding company to sell in its domestic market.

Import tariffs could make imports (from the holding company) more expensive than domestically produced goods.

Insist on a minimum shareholding, i.e. that some equity in the company is offered to resident investors.

Company structure may be dictated by the host government – requiring, for example, all investments to be in the form of joint ventures with host country companies.

Discriminatory actions

Super-taxes imposed on foreign firms, set higher than those imposed on local businesses with the aim of giving local firms an advantage. They may even be deliberately set at such a high level as to prevent the business from being profitable.

Restricted access to local borrowings by restricting or even barring foreign-owned enterprises from the cheapest forms of finance from local banks and development funds. Some countries ration all access for foreign investments to local sources of funds, to force the company to import foreign currency into the country.

Expropriating assets whereby the host country government seizes foreign property in the national interest. It is recognised in international law as the right of sovereign states provided that prompt consideration at fair market value in a convertible currency is given. Problems arise over the exact meaning of the terms prompt and fair, the choice of currency, and the action available to a company not happy with the compensation offered.

Measurement of political risk

When considering measurement, distinctions are sometimes made between macro and micro political risk.

Micro political risks are ones that are specific to an industry, company or project within a host country. For example, the tobacco industry has faced increasing global opposition since the 1970s, nowhere more so than in the USA. There are increasing threats that tobacco will be classified as a drug and that companies supplying tobacco may face continuing litigation. This has been a consequence of a change in the social and political climate in the USA and elsewhere.

By contrast Iraq at the moment presents political risks for almost any organisation who may wish to operate there in terms of the threat of loss of assets or personnel. This therefore represents macro political risk.

Different methods may be appropriate to measuring different types of risk. Traditional methods for assessing political risk range from comparative techniques such as rating and mapping systems to the analytical techniques of special reports, expert systems and probability determination, through to use of econometric techniques of model building. More recently, option-pricing techniques (using real options) have been applied to the evaluation of political risk associated with foreign direct investment.

Some examples of methods used to measure political risk are indicated below:

- ‘Old hands’ – Experts on the country provide advice upon the risk of investment in a specific country. Experts may include those with existing businesses, academics, diplomats or journalists. The value of the advice depends on how directly it can be applied to the investment under consideration.

- ‘Grand tours’ – The home firm may send a selection of employees to the potential investment country to act as an inspection team. The employees meet government officials, business people and local leaders to gain an understanding of the country first hand. However, this technique is generally considered inferior to the use of advice from well-established experts as outlined above.

- Surveys – Commercially produced country political risk indices are available. These are produced by groups of experts using Delphi techniques via the ranking of key risk variables. The experts individually answer a comprehensive questionnaire. Their answers are then collected, aggregated and returned to the experts, who have the chance to change their minds having seen the answers of their peers.

- Quantitative measures – Measures such as GNP and ethnic fractionalisation are combined to give countries an overall score. Commercially produced indices are available. One is the business environment risk index (BERI). This index gives each country a score out of 100, where a low score indicates unacceptable business conditions. Also, the Economist Intelligence Unit (EIU)’s Country Risk Model allows users to quantify the risk of cross-border transactions such as bank loans, trade finance, and investments in securities. Often some form of sensitivity or simulation analysis is incorporated to examine the effect of different possible scenarios. A general risk index offers a cost effective overview of potential investment climates but cannot take account of the variations in risk on individual projects. It should also be borne in mind that the scoring systems are essentially subjective.

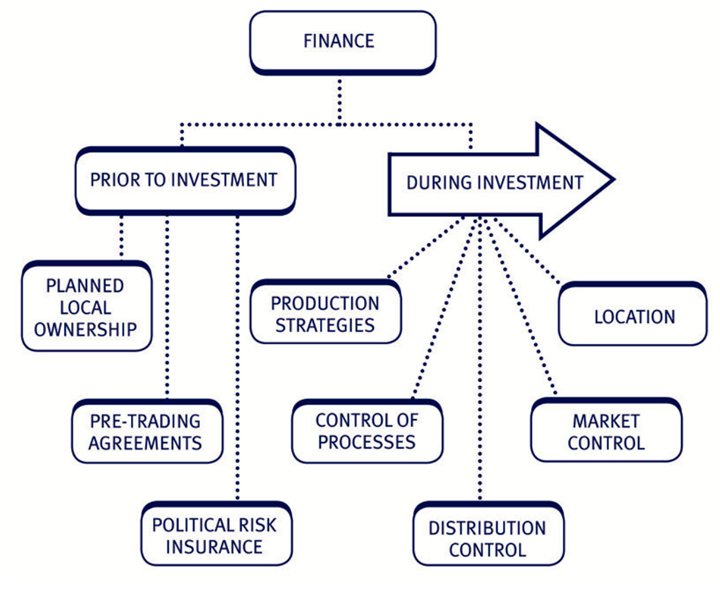

- Planned local ownership

Target dates can be set on which proportions of company ownership will pass to the local nationals. These should be spread into the long term so that local authorities can see the eventual benefits that will be gained through allowing successful foreign investments.

- Pre-trading/concession agreements

Prior to making the investments, agreements should be secured with the local government or other authority regarding rights, responsibilities, remittance of funds and local equity investments. This attempts to solve anticipated problems and prevent misunderstandings at some later date.

The biggest problem with this policy is that host governments in developing countries are very volatile; consequently, agreements made with previous administrations can be repudiated by the new government.

Wells (1977) argues that the terms of concession agreements will normally change even with the same host government as:

The terms and conditions required to entice a company to invest in a particular country are different from the terms and conditions required to a company remain, once it has committed and developed its investment. (Remember sunk costs)

If the multinational is more successful than both parties anticipated in the beginning of the investment, thus the government may want their share of the windfall.

The agreement will cover transfer of capital, transfer of remittances, transfer of products, access to local capital markets, transfer pricing, taxation and social and economic obligations.

- Political risk insurance

It may be possible to transfer the risk by taking out insurance. In the UK, the Export Credits Guarantee Department (ECGD) provides protection against various threats including expropriation and nationalisation, currency inconvertibility, war and revolution.

During investment

Political risk can be managed on a continuous basis through consideration of the following areas:

- Production strategies

The decision here is to find the balance between:

– contracting out to local sources (local sourcing) and losing control

– producing directly in the host country (increasing investment in host country)

– importing from outside the host country (foreign sourcing).

By using local materials and labour it becomes in the interest of the country for the company to succeed. However, following success the locals may then have the knowledge to continue operations alone. Chrysler in Peru imported 50% of components from abroad and thus avoided expropriation of its plant because the plant was worthless without the foreign sourced Chrysler parts.

- Control of patents and processes

Coca Cola is a prime example of how control of patents reduces political risk. The secret ingredient in Coca Cola has never been divulged. Therefore, Coca Cola can quite happily set up bottling plants worldwide, as the plants are worthless to any host government as they would not be able to create ‘the taste of Coca Cola’. Patents can be enforced internationally.

- Distribution control

Control and development of such items as pipelines and shipping facilities will deter expropriation of assets.

- Market control

Securing markets through copywriting, patents and trademarks deters political intervention as the local markets come to depend on ‘protected’ goods.

- Location

Oil companies frequently mine oil in a politically unstable area but refine it in western Europe. Expropriation of assets would not therefore benefit the less stable countries.

Financing decisions

Political risk may be mitigated by choosing the right location for raising funds:

- Local finance

As the foreign investment grows, further finance can be raised locally to maintain the authorities’ interest in the success of the business – any damaging intervention would also damage the local institutions. Also the wealthier locals who provide this finance often have considerable power. As a result there is less likelihood of others expropriating the assets. However, the cost of such funds may be relatively more expensive and many governments restrict the ability of multinational to borrow from local money and capital markets.

- Borrow worldwide

A multinational also has the option of financing worldwide, using institutions from several countries. This discourages expropriation because if the host government intervenes in the company’s operations, default on the loans may cause a diplomatic backlash from a number of countries, not just the multinational’s own parent country. However, it is important to take account of the new risks associated with, for example, foreign exchange and tax, that may be introduced where funds are borrowed overseas.

Economic risk

Economic risk is the variations in the value of the business (i.e. the present value of future cash flows) due to unexpected changes in exchange rates. It is the long-term version of transaction risk which is covered in detail in the hedging chapters.

In a broader sense, economic risk can also be defined as the risk facing organisations from changes in economic conditions, such as economic growth or recession, government spending policy and taxation policy, unemployment levels and international trading conditions.

It affects:

- the affordability of exports and therefore competitiveness

- the affordability of imports and therefore profitability

- the value of repatriated profits.

Examples and management of economic risk

Economic risk is the possibility that the value of the company (the present value of all future post-tax cash flows) will change due to unexpected changes in future exchange rates. The size of the risk is difficult to measure as exchange rates can change significantly and unexpectedly. Such changes can affect firms in many ways:

- Consider the example of a US firm, which operates a subsidiary in a country that unexpectedly devalues its currency. This could be ‘bad news’ in that every local currency unit of profit earned would now be worth less when repatriated to the US. On the other hand it could be ‘good news’ as the subsidiary might now find it far easier to export to the rest of the world and hence significantly increase its contribution to parent company cash flow. The news could, alternatively, be neutral if the subsidiary intended to retain its profits to reinvest in the same country abroad.

- An exporter may suffer different forms of economic risk:

Direct: If the firm’s home currency strengthens, foreign competitors are able to gain sales at their expense because their products become more expensive (unless the firm reduces margins) in the eyes of customers both abroad and at home.

Indirect: Even if the home currency does not move vis-à-vis the customers’ currency the firm may lose competitive position. For example, suppose a South African firm is selling into Hong Kong and its main competitor is a New Zealand firm. If the New Zealand dollar weakens against the Hong Kong dollar, the South African firm has lost some competitive position.

Although economic exposure is difficult to measure it is of vital importance to firms as it concerns their long-run viability. Economic exposure is really the long-run equivalent of transaction exposure, and ignoring it could lead to reductions in the firm’s future cash flows or an increase in the systematic risk of the firm, resulting in a fall in shareholder wealth.

Managing economic risk

Note that the recommended methods of mitigating economic exposure, are also suggested as ways of mitigating political exposure:

- Diversification of production and supply.

- Diversification of financing.

If a firm manufactures all its products in one country and that country’s exchange rate strengthens, then the firm will find it increasingly difficult to export to the rest of the world. Its future cash flows and therefore its present value would diminish.

However, if it had established production plants worldwide and bought its components worldwide (a policy which is practised by many multinationals, e.g. Ford) it is unlikely that the currencies of all its operations would revalue at the same time. It would therefore find that, although it was losing exports from some of its manufacturing locations, this would not be the case in all of them. Also if it had arranged to buy its raw materials worldwide it would find that a strengthening home currency would result in a fall in its input costs and this would compensate for lost sales.

Diversification of financing

When borrowing internationally, firms must be aware of foreign exchange risk. When, for example, a firm borrows in Swiss francs it must pay back in the same currency. If the Swiss franc then strengthens against the home currency this can make interest and principal repayments far more expensive. However, if borrowing is spread across many currencies it is unlikely they will all strengthen at the same time and therefore risks can be reduced. Borrowing in foreign currency is only truly justified if returns will then be earned in that currency to finance repayment and interest.

International borrowing can also be used to hedge off the adverse economic effects of local currency devaluations. If a firm expects to lose from devaluations of the currencies in which its subsidiaries operate it can hedge off this exposure by arranging to borrow in the weakening currency. Any losses on operations will then be offset by cheaper financing costs.

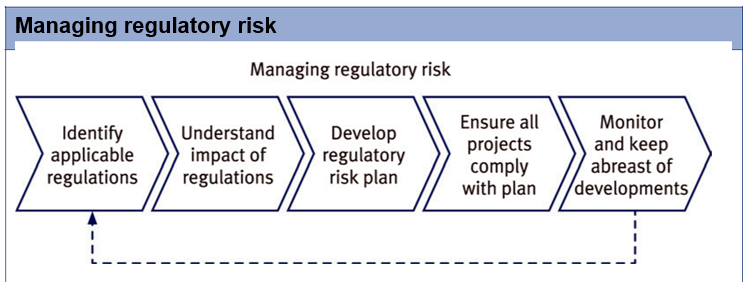

Regulatory risk

Regulatory risk is the potential for laws related to a given industry, country, or type of security to change and affect:

- how the business as a whole can operate

- the viability of planned or ongoing investments. Regulations might apply to:

- businesses generally (for example, competition laws and antimonopoly regulations)

- specific industries (for example, catering and health and safety regulations, publishing and copyright laws).

Whilst larger companies may have the resources to set up a permanent regulatory team, smaller firms may:

- incorporate the role within the internal audit department

- consult a firm specialising in regulatory risk.

In practice, research suggests that many firms do not commit sufficient resources to this area and are exposed to a high degree of regulatory risk.

Associated with regulatory risk is compliance risk.

Compliance risk is the risk of losses, such as fines or even temporary closure, resulting from non-compliance with laws or regulations.

Measures to ensure compliance with rules and regulations should be an integral part of an organisation’s internal control system.

Fiscal risk

Fiscal risk from a corporate perspective is the risk that the government will have an increased need to raise revenues and will increase taxes, or alter taxation policy accordingly. Changes in taxation will affect the present value of investment projects and thereby the value of the company.

Managing fiscal risk

The primary requirement of a fiscal risk management strategy is an awareness of the huge impact tax can make to the viability of a project. Tax should be factored in to the calculations for all significant investment appraisal projects.

It is important not only to ensure that the tax rules being applied are up-to-date, but that any potential changes in the tax rules are also considered. Investment projects may be intended to run for many years and future changes (particularly those intended to close ‘loop holes’ in the taxation system) could wipe out the expected benefits from the project.

Many larger firms will maintain a full time taxation team within the finance function to deal with the tax implications of investment plans. Smaller companies are more likely to employ external tax experts. In either case, a relevant tax expert should always be involved in the analysis of the project and its sensitivity to the taxation assumptions should be carefully modelled.

Test your understanding 1

M plc is a mineral extraction company based in the UK but with plants based in many countries worldwide. Following recent discovery of mineral reserves in Mahastan in Central Asia, M plc has acquired a licence to extract the minerals from the recently elected Mahastani government and plans to commence work on the plant there within the next six months.

In the past ten years, Mahastan has seen significant unrest, following the deposing of the previous dictator in a military coup. However, the recent election of the newly fledged democracy is hoped to be the beginning of a new era of stability in the region. The currency of Mahastan is the puto.

It is not traded internationally and the preferred currency for international business is the US dollar. There are currently no double tax treaties between Mahastan and the rest of the world, but the prime minister has signalled his intention to develop them within his first term of office to encourage inward investment.

Required:

Assess the exposure of M plc to political, economic, regulatory and fiscal risk and suggest how these risks may be mitigated.

Other types of risk

It is important to read the financial press to keep abreast of recent developments in risk management.

Risk management is a constantly evolving process. Financial managers need to understand the threats from emerging risks such as:

- global terrorist risk

- computer virus risks

- spreadsheet risk – for example, Fannie Mae’s $1.136 billion underestimate of total stockholder equity in 2003 was the result of errors in a spreadsheet used in the implementation of a new accounting standard.

Policies will need to be kept up to date, so that these newer risks are managed properly.

5 Incorporating risk into investment appraisal

Overview of methods

The input variables in an investment appraisal are all estimates of likely future outcomes. There are several methods of incorporating risk into an investment appraisal, for example:

- expected values (probability analysis)

- use of the CAPM model to derive a discount rate

- sensitivity analysis, and simulation.

These methods have all been covered in Financial Management (FM), but some more details on probability analysis, sensitivity and simulation follow below.

Probability analysis

If the outcome from an investment is uncertain, but the probability associated with each of the possible outcomes is known, an expected value calculation can be used.

The expected value is calculated as the sum of (each outcome multiplied by its associated probability).

For example, if sales are expected to be either $1,000,000 or $1,500,000 with probabilities of 35% and 65% respectively, the expected sales can be calculated as:

($1,000,000 × 0.35) + ($1,500,000 × 0.65) = $1,325,000

The main problem with the expected value calculation is that the value might not correspond to any of the possible outcomes, so although the calculation gives a useful long-run average figure, it is not useful for one-off calculations.

More on the use of probability analysis

Probability analysis can be applied to potential cash flows of a project (as demonstrated in the simple example above regarding the sales figure). However, it can also be applied to other uncertain estimates, such as units of activity or even cost of capital.

After probabilities have been used to calculate an expected value figure for one or more of these variables, the project can then be appraised as normal, using methods such as NPV.

If several uncertain variables have been estimated using probability analysis, it is important to note that the potential for inaccuracy in the final NPV calculation is increased. Then, techniques such as sensitivity analysis and simulation (see below) come into play.

Conditional probabilities

In complex cases of uncertainty, conditional probabilities may be useful. Here, the probability of one outcome is dependent (conditional) on another outcome. The expected value is now found by multiplying the relevant probabilities together.

Example:

There is a 60% chance that sales levels will be high ($3 million) in year 1, and hence a 40% chance that year 1 sales will be low ($1 million).

If sales in year 1 are high, the sales in year 2 will be either $5 million (30% probability) or $4 million (70% probability).

If sales in year 1 are low, the sales in year 2 will be either $0.5 million (80% probability) or $1.5 million (20% probability).

Solution

The expected sales in year 1, which should be entered in year 1 of the investment appraisal, is:

(0.60 × 3m) + (0.40 × 1 m) = $2.2 million

Then, the expected sales in year 2, which should be entered in year 2 of the investment appraisal, is:

(0.60 × [(0.30 × 5m) + (0.70 × 4m)]) + (0.40 × [(0.80 × 0.5m) + (0.20 ×

1.5m)]) = $2.86 million

Student Accountant article

The article ‘Conditional probability’ in the Technical Articles section of the ACCA website provides further details on this topic.

Sensitivity analysis

Sensitivity analysis measures the change in a particular variable which can be tolerated before the NPV of a project reduces to zero.

It can be calculated as

(NPV of project)/(PV of cash flows affected by the estimate) × 100%

Illustration of sensitivity analysis

| AVI Co is evaluating a new investment project as follows: | |||||

| $000 | t | t | t | t | t4 |

| Sales | 1,000 | 1,000 | 1,000 | 1,000 | |

| Costs | 600 | 600 | 600 | 600 | |

| ––––– | ––––– | ––––– | ––––– | ||

| 400 | 400 | 400 | 400 | ||

| Tax (30%) | (120) | (120) | (120) | (120) | |

| ––––– | ––––– | ––––– | ––––– | ||

| Net | 280 | 280 | 280 | 280 | |

| CapEx | (600) | ||||

| Tax relief on | |||||

| depreciation | |||||

| (30%) | 45 | 45 | 45 | 45 | |

| ––––– | ––––– | ––––– | ––––– | ––––– | |

| Free cash flow | (600) | 325 | 325 | 325 | 325 |

| ––––– | ––––– | ––––– | ––––– | ––––– | |

| DF @ 10% | 1 | 0.909 | 0.826 | 0.751 | 0.683 |

NPV = $430,000

Sensitivity to sales

- (NPV/PV of cash flows affected by the estimate of sales) × 100%

- [430/(1,000 × (1 – 0.30) × 3.170)] × 100%

- 4%

i.e. if sales were to fall by 19.4% (to $806,000 per annum) then the NPV would be zero.

Sensitivity to tax rate

- (NPV/PV of cash flows affected by the estimate of tax rate) × 100%

- [430/((45 – 120) × 3.170)] × 100%

- 181%

i.e. if the tax rate were to rise by 181% (from 30% to 30 × 2.82 = 84.6%)

then the NPV would fall to zero.

Sensitivity to discount rate

This cannot be calculated using the standard formula. Instead, the IRR of the project is calculated and the difference between the existing cost of capital and the IRR indicates the sensitivity to the discount rate.

Interpretation of sensitivity calculations

AVI Co would initially be inclined to accept the project due to its positive NPV. However, before making a final decision, the sensitivities would be considered. Any factors with small percentage sensitivities will have to be carefully assessed, because if the estimates of these factors turn out to be incorrect, the result may be a negative NPV.

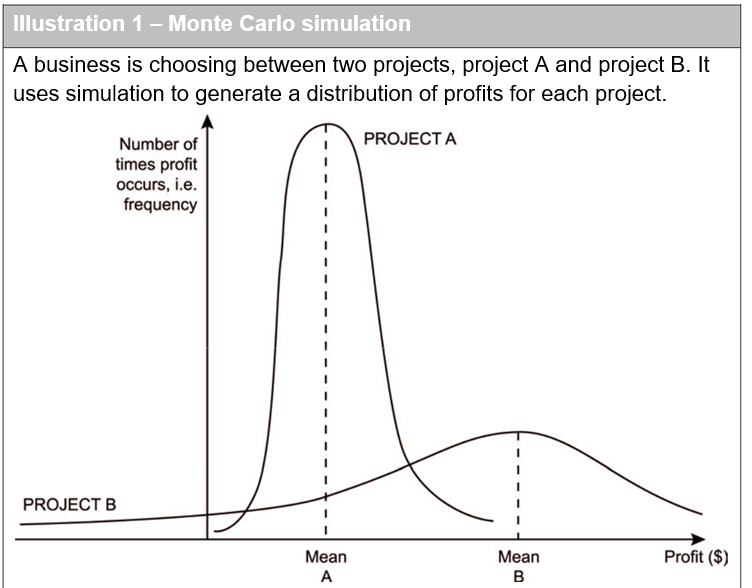

Simulation

The main problem with sensitivity analysis is that it only allows us to assess the impact of one variable changing at a time. Simulation addresses this problem by considering how the NPV will be impacted by a number of variables changing at once.

Simulation employs random numbers to select specimen values for each variable in order to estimate a ‘trial value’ for the project NPV. This is repeated a large number of times until a distribution of net present values emerge.

By analysing this distribution, the firm can decide whether to proceed with the project. For example, if 95% of the generated NPVs are positive, this might reassure the firm that the chances of suffering a negative NPV are small.

Monte Carlo simulation assumes that the input variables are uncorrelated. However, more sophisticated modelling can incorporate estimates of the correlation between variables.

More details on Monte Carlo simulation

The assessment of the volatility (or standard deviation) of the net present value of a project entails the simulation of the financial model using estimates of the distributions of the key input parameters and an assessment of the correlations between variables.

Some of these variables are normally distributed but some are assumed to have limit values and a most likely value. Given the shape of the input distributions, simulation employs random numbers to select specimen values for each variable in order to estimate a ‘trial value’ for the project NPV.

This is repeated a large number of times until a distribution of net present values emerge.

By the central limit theorem the resulting distribution will approximate normality and from this project volatility can be estimated.

In its simplest form, Monte Carlo simulation assumes that the input variables are uncorrelated. However, more sophisticated modelling can incorporate estimates of the correlation between variables.

Other refinements such as the Latin Hypercube technique can reduce the likelihood of spurious results occurring through chance in the random number generation process.

The output from a simulation will give the expected net present value for the project and a range of other statistics including the standard deviation of the output distribution.

In addition, the model can rank order the significance of each variable in determining the project net present value.

Example of Monte Carlo simulation

The MP Organisation is an independent film production company. It has a number of potential films that it is considering producing, one of which is the subject of a management meeting next week. The film which has been code named CA45 is a thriller based on a novel by a well-respected author.

The expected revenues from the film have been estimated as follows: there is a 30% chance it may generate total sales of $254,000; 50% chance sales may reach $318,000 and 20% chance they may reach $382,000.

Expected costs (advertising, promotion and marketing) have also been estimated as follows: there is a 20% chance they will reach approximately $248,000; 60% chance they may get to $260,000 and 20% chance of totalling $272,000.

In a Monte Carlo simulation, these revenues and costs could have random numbers assigned to them:

| Sales Revenue | Probability | Assign Random Numbers |

| (assume integers) | ||

| $254,000 | 0.30 | 00–29 |

| $318,000 | 0.50 | 30–79 |

| $382,000 | 0.20 | 80–99 |

| Costs | ||

| $248,000 | 0.20 | 00–19 |

| $260,000 | 0.60 | 20–79 |

| $272,000 | 0.20 | 80–99 |

A computer could generate 20-digit random numbers such as 98125602386617556398. These would then be matched to the random numbers assigned to each probability and values assigned to ‘Sales Revenues’ and ‘Costs’ based on this. The random numbers generated give 5 possible outcomes in our example:

| Random | Sales revenue in | Random | Costs in | Profit |

| number | $000 | Number | $000 | |

| 98 | 382 | 12 | 248 | 134 |

| 56 | 318 | 02 | 248 | 70 |

| 38 | 318 | 66 | 260 | 58 |

| 17 | 254 | 55 | 260 | (6) |

| 63 | 318 | 98 | 272 | 46 |

After the computer simulation has been run many many times, a frequency distribution of the profits (in the final column of the above table) can be drawn, to give a sense of what the likely outcome will be.

After so few runs (only 5 in the above example), it is difficult to see a pattern yet, but if similar results were to be obtained over many many simulations, only 20% of the combinations (1 in 5) would give a loss.

Simulation cannot give a definitive answer on whether to undertake the project or not, but an analysis of the results will enable the decision maker to assess the risk associated with the project, for example the risk of making a loss in the above example.

Required:

Which project should the business invest in?

Solution

Project A has a lower average profit but is also less risky (less variability of possible profits).

Project B has a higher average profit but is also more risky (more variability of possible profits).

There is no correct answer. All simulation will do is give the business the above results. It will not tell the business which is the better project.

If the business is willing to take on risk, they may prefer project B since it has the higher average return.

However, if the business would prefer to minimise its exposure to risk, it would take on project A. This has a lower risk but also a lower average return.

Value at Risk (VaR)

The meaning of VaR

Value at risk (VaR) is a measure of how the market value of an asset or of a portfolio of assets is likely to decrease over a certain time, the holding period (usually one to ten days), under ‘normal’ market conditions.

VaR is measured by using normal distribution theory.

It is typically used by security houses or investment banks to measure the market risk of their asset portfolios.

VaR = amount at risk to be lost from an investment under usual conditions over a given holding period, at a particular ‘confidence level’.

Confidence levels are usually set at 95% or 99%,

e.g. for a 95% confidence level, the VaR will give the amount that has a 5% chance of being lost.

Illustration 2

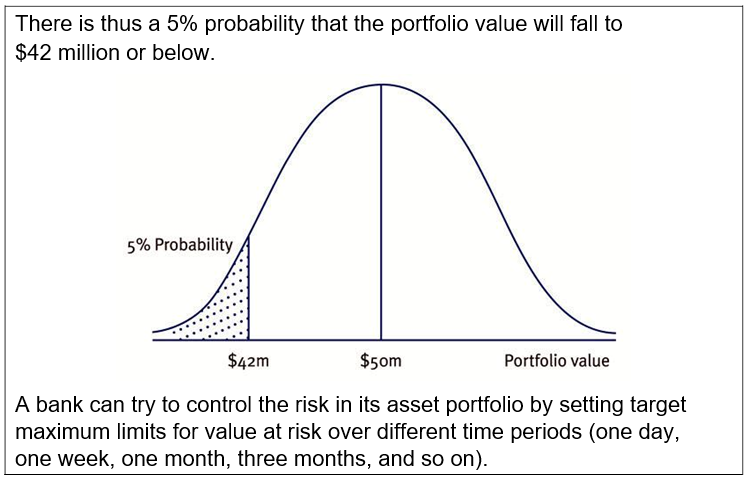

A bank has estimated that the expected value of its portfolio in two weeks’ time will be $50 million, with a standard deviation of $4.85 million.

Required:

Using a 95% confidence level, identify the value at risk.

Solution

A 95% confidence level will identify the reduced value of the portfolio that has a 5% chance of occurring.

From the normal distribution tables, 1.65 is the normal distribution value for a one-tailed 5% probability level. Since the value is below the mean, – 1.65 will be needed.

z = (x – μ)/σ

(x – 50)/4.85 = –1.65

x = (–1.65 × 4.85) + 50 = 42

Link between Monte Carlo Simulation and VaR

In the above Illustration, the expected portfolio value in two weeks’ time was presented as a normal distribution with a mean of $50m.

This distribution may well have been created by running a Monte Carlo simulation on the likely outcome over the next two weeks.

Alternatively, the future expected value may have been forecasted by using historical data.

Test your understanding 2

A bank has estimated that the expected value of its portfolio in 10 days’ time will be $30 million, with a standard deviation of $3.29 million.

Required:

Using a 99% confidence level, identify the value at risk.

7 Introduction to hedging methods

The use of derivative products

Hedging methods relating to currency risk and interest rate risk are covered in separate later chapters. Many of the hedging methods use ‘derivatives’ (e.g. futures contracts) to reduce the firm’s exposure to risk.

This section introduces some basic terms relating to derivatives.

The operation of the derivatives market

- A derivative is an asset whose performance (and hence value) is derived from the behaviour of the value of an underlying asset (the ‘underlying’).

- The most common underlying assets are commodities (e.g. tea, pork bellies), shares, bonds, share indices, currencies and interest rates.

- Derivatives are contracts that give the right and sometimes the obligation, to buy or sell a quantity of the underlying or benefit in some other way from a rise or fall in the value of the underlying.

- Derivatives include the following:

– Forwards

– Forward rate agreements (‘FRAs’)

– Futures

– Options

– Swaps.

- Forwards, FRAs and futures effectively fix a future price. Options give you the right without the obligation to fix a future price.

- The legal right is an asset with its own value that can be bought or sold.

- Derivatives are not fixed in volume of supply like normal equity or bond markets. Their existence and creation depends on the existence of counter-parties, market participants willing to take alternative views on the outcome of the same event.

- Some derivatives (especially futures and options) are traded on exchanges where contracts are standardised and completion guaranteed by the exchange. Such contracts will have values and prices quoted. Exchange-traded instruments are of a standard size thus ensuring that they are marketable.

- Other transactions are over the counter (‘OTC’), where a financial intermediary puts together a product tailored precisely to the needs of the client. It is here where valuation issues and credit risk may arise.

These features of derivative products were introduced in Financial Management (FM).

Futures contracts

Introduction

- A futures contract is an exchange traded forward agreement to buy or sell an underlying asset at some future date for an agreed price.

- There are two ways of closing a position:

– Deliver the underlying on the maturity date – RARE.

– If futures contracts have been bought, then equivalent contracts can be sold before maturity, resulting in the company having a net profit or loss (and no obligation to deliver).

- Hedging is achieved by combining a futures transaction with a market transaction at the prevailing spot rate.

Illustration 3 – TAL

TAL Inc is a sugar grower looking to sell 3,000 tonnes of white sugar in August and wants to fix the price via futures.

Suppose that the quoted futures price today on LIFFE for white sugar for August delivery is $221.20 per tonne and that each contract is for 50 tonnes.

TAL would agree to sell 60 futures contracts at a price of $221.20.

Suppose the market price in August (on the final day of the contract) has risen to $230. The futures price would also equal $230.

TAL thus has two transactions:

- TAL would sell their sugar in the open market (i.e. not via the futures contract) for $230/tonne.

- Separately TAL would buy 60 futures contracts for August delivery for $230 per tonne, making a loss on the futures of $8.8 per tonne.

This gives an overall (fixed) net receipt of $221.2 per tonne. Note: Futures do not always give a perfect hedge because of

- Basis risk.

- The size of contracts not matching the commercial transaction.

Tick sizes

- A ‘tick’ is the standardised minimum price movement of a futures or options contract.

- Ticks are useful for calculating the profit or loss on a contract.

Illustration 4 – TAL continued

For the sugar futures contract in the above example, a tick is $0.01 per tonne. Given that a contract is for 50 tonnes, each tick is worth $0.50 per contract.

The overall movement of $8.80 per tonne would be expressed as 880 ticks.

The total loss on the contracts would thus be:

60 contracts × 880 ticks × $0.50 per tick = $26,400

As detailed below, this amount would not be collected in one amount when the position is closed but instead daily ‘marking to market’ occurs.

The margin system

Margins

A potential problem of dealing in futures is that having made a profit, the other party ‘to the contract’ has therefore made a loss and defaults on paying you your profit. This is termed ‘counter party credit risk’.

- However the buyer and seller of a contract do not transact with each other directly but via members of the market.

- Therefore the market’s Clearing House is the formal counter party to every transaction.

- This effectively reduces counter party default risk for those dealing in futures.

- As the Clearing House is acting as guarantor for all deals it needs to protect itself against this enormous potential credit risk. It does so by operating a margining system, i.e. an initial margin and the daily variation margin.

The initial margin

- When a futures position is opened the Clearing House requires that an initial margin be placed on deposit in a margin account to act as a security against possible default.

- The objective of the initial margin is to cover any possible losses made from the first day’s trading.

- The size of the initial margin depends on the future market, the level of volatility of the interest rates and the risk of default.

- For example, the initial margin on a £500,000 ‘3 month sterling contract’ traded on LIFFE is £750, i.e. £750/£500,000 = .0015%.

- Some investors use futures for speculation rather than hedging. The margin system allows for highly leveraged ‘bets’.

Maintenance margin, margin call and the variation margin

- When the hedge is set up, the Clearing House specifies an amount (‘the maintenance margin’) which represents the minimum amount that the client must keep in the margin account.

- At the end of each day the Clearing House calculates the daily profit or loss on the futures position. This is known as ‘marking to market’. The daily profit or loss is added or subtracted to the margin account balance.

- If this causes the amount in the margin account to fall below the specified maintenance margin, a ‘margin call’ is made to the investor, requiring the investor to deposit extra funds (the ‘variation margin’) to top-up the margin account.

- An inability to pay the variation margin causes default and the contract is closed, thus protecting the Clearing House from the possibility that the investor might accumulate further losses without providing cash to cover them.

Numerical example

Peter Ng is a wealthy speculator who believes that oil prices will fall over the next three months. Oil futures are quoted with the following details:

- Futures price for 3 month delivery = $68.20 per barrel.

- Contract size = 1,000 barrels.

- Tick size = 1 cent per barrel.

- Initial margin = 10% of contract.

Peter decides to set his level of speculation at 10 contracts.

Required:

- Calculate Peter’s initial margin.

- Assuming that the initial margin calculated in part (a) is the same as the maintenance margin on Peter’s account, calculate the required variation margin cash flow the next day if the futures price moves to $68.35.

Solution

- Initial margin = 10% × 10 contracts × 1,000 barrels × $68.20 = $68,200.

- Price has increased so Peter will make a loss of $0.15 per barrel or 15 ticks. This equates to a total loss (which will need to be paid in to top-up the margin account).

Loss = 10 contracts × 15 ticks × $10 per tick = $1,500.

Political risks

Possible ramifications would include:

- revocation of the licence

- significant increase in the licence fee

- company subject to regulations designed to prevent the company taking profits earned from the country:

– imposition of punitive taxes

– restrictive exchange controls

- seizure of control of the plant

- expropriation of the extracted minerals

- total disruption to operations from further coup attempts.

Economic risks

In terms of exchange risk, the primary risk will be caused by changes in value between UK sterling and the US dollar. Although some payments (such as employee wages) will presumably be made in putos and M plc will therefore be subject to some risk associated with fluctuations between the puto and the dollar, it is unlikely to have any significant impact on the long term viability of the project.

Regulatory risk

As M plc are based in the UK, which can be expected to have a fairly stringent set of regulations covering mineral extraction, it is not anticipated that the Mahastan project will present any significant specific regulatory risk.

However, new regulations imposed on all foreign companies operating in Mahastan may come into force once the new government finds its feet. This could affect the ability of the company to operate effectively.

Fiscal risk

The uncertainty over the double tax position is an obvious risk for M plc. In addition, the country’s tax legislation may not be well established and may be changed as the prime minister looks to encourage investment.

Risk mitigation

The recent political instability in Mahastan and the newness of the government, make this investment a very high-risk project.

Political risk

M plc already have a licence for the extraction of the minerals. They could attempt to negotiate further terms surrounding matters as diverse as levels of price increases, transfer of capital, transfer of remittances, transfer of products, access to local capital markets, transfer pricing, taxation and social and economic obligations.

However no matter what is negotiated the risk that the agreement will be not be honoured by this government (or subsequent ones should it fail) remains high.

The political risks can be best mitigated by gaining the goodwill of the community and ensuring that the wealth generated by the mineral extraction is not perceived to be entirely the preserve of M plc. Solutions may include:

- employing local workers where possible

- paying fair wages

- considering joint ventures with local companies over some parts of the construction or extraction processes

- investing some part of the profits in local opportunities.

It may be worth considering political risk insurance. However where the risk is so high the premiums may be prohibitive.

Economic risk

Since M plc has an international presence, the economic risk of the project will already be mitigated by their diversification. However, if many of the areas in which it operates also trade in dollars then the benefits are reduced. Consideration should also be given to financing using dollar-based loans.

Regulatory risk

The risk that onerous regulations may be imposed on M plc cannot be easily avoided. The methods of mitigating political risk mentioned above, would also apply here, although they are unlikely to help with regulations aimed at all organisations.

M plc must ensure that they consistently monitor the changing regulatory environment and consider the impact on their firm. As the government is keen to encourage inward investment, it would be worth attempting to identify key ministers and open up lines of communication with them. Being viewed as an important stakeholder may mean that M plc is consulted on major regulatory changes before they are implemented.

Fiscal risk

Given the considerable uncertainty, fiscal risk may be best managed by assuming worst case tax treatment (based on current information) and only accepting the project if the NPV is still positive. Again constant monitoring of the situation and reforecasting as necessary will also be required.

One thought on “An introduction to risk management”