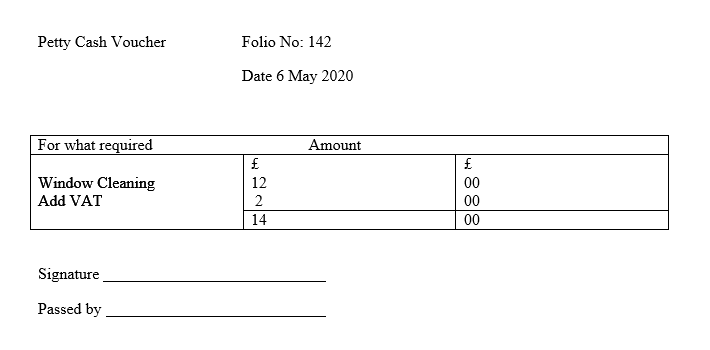

PETTY CASH

This is the imprest/advance/loan/float that a Petty Cashier receives from the General or Chief Cashier to make payment that require little amounts of money such as postage, buying stationery, paying for bus fares or taxis, office cleaning and staff tea.

When a person receives cash from a Petty Cashier, a receipt or Petty Cash Voucher should be obtained as prove of the transaction. Petty Cash Vouchers are usually pre-printed and numbered. Whenever money is paid the Petty Cashier fills a Petty Cash Voucher giving description of the item, the amount, date and signature.

PROCEDURE FOR OPERATING THE PETTY CASH SYSTEM

- An amount is fixed for the petty cash

- The Petty Cashier uses the money to purchase small items.

- He records each expenditure in the petty cash book

- At the end of a specific period he calculates the total amount used

- He subtracts the total used from the allocation given at the beginning of the period

- He is reimbursed for the expenditure to bring the figure back to the original amount.

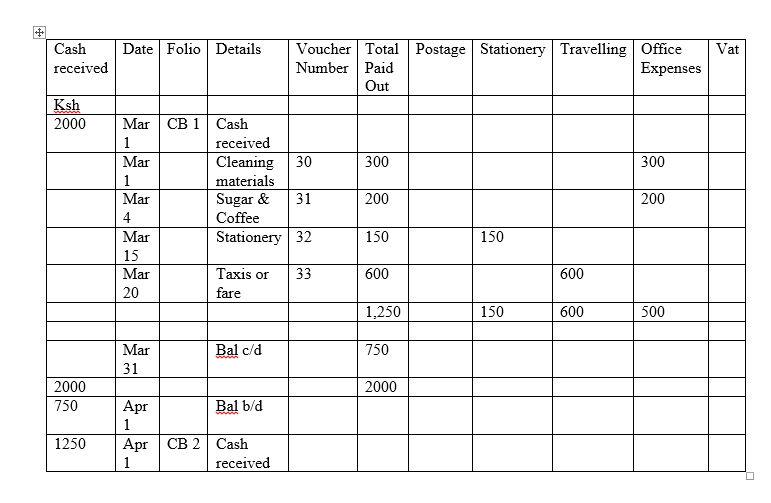

A petty cash book has columns for:

- Date

- Details of cash received

- Details of cash paid out

- Analysis columns

- Value added Tax (VAT) column

NB: The headings of the analysis columns can be varied to suit the requirements of a particular organization.

The usually fall under the following categories.

- Postage including parcels, telegrams etc

- Stationery – small items such as ink, rubber, envelopes etc

- Travelling expenses, for example, fares, taxes, etc

- Sundry/Office Expenses which includes items such as window cleaning, typewriter repairs, mild for office tea etc

Question

At the beginning of March, the Cashier released Ksh 2,000 for petty cash

On 1st cleaning materials worth Ksh 300 were bought against payment voucher number 30

On 4th sugar and coffee worth Ksh 200 were bought against payment voucher number 31

On 15th stationery worth Ksh 150 was purchased against payment voucher number 52

On 20th taxi fares Ksh 600 were paid to the regular transporter against payment voucher number 33

- Complete the analysis columns by filling in suitable headings

- Enter the details and show the balance in hand at the end of the month

- Show the amount that will be released by the cashier to restore the float

QUESTION

Outline three ways of ensuring proper control of petty cash in an office.

ANSWER

- The petty cashier should be responsible for the petty cash and be accountable for it

- A receipt or petty cash voucher should be obtained when any person receives cash from the petty cashier

- The records that include the minor/small payments should be kept in the petty cash book.

WAGES AND SALARIES

Wages are paid for services rendered in accordance with the piece of work done or hours worked.

Salaries are paid for services rendered on a monthly basis for regular employment or permanent employees on a yearly basis.

METHODS OF CALCULATING WAGES AND SALARIES AND WHEN THEY MAY BE USED

- Flat rate or basic rate – this is fixed amount of money paid to an employee usually on a monthly basis. It is used to pay salaried workers.

- Piece rate – paid for the completion of a given amount of work or unit of product or article. Commonly used for factors workers.

- Hourly rate or time rate – time is recorded on a time or clock card and the employee is paid for the number of hours worked in a week or month. It is suitable for employees whose hours of work vary e.g. part time workers

- Overtime – paid to employees who are required to work extra hours. It is calculated at an agreed rate e.g. 1¼, 1½, or double the normal rate.

- Commission – the worker is paid according to his performance at an agreed percentage. Commonly used in paying sales staff.

ADVANTAGES OF THE TIME RATE METHOD OF PAYING WAGES

- It is convenient method as time spent on the job is measured and wages calculated easily

- Employees can forecast their income and they are assured to receive this income

- It gives the employer an adequate idea of his wage burden and he can make adequate provision for its payment

- This is more suitable for such jobs where work cannot be divided into smaller units e.g. the work of an office worker

- Less wastage – under time wages, the workers need not speed up their operations to earn higher wages. There will be less wastage of materials and less wear and tear of tools and machinery

- Adaptability – this system can be adapted to all kinds of work. Even if a worker does a variety of jobs, he can be compensated on time wage basis

- Equality of wages – all workers doing similar jobs get the same rate of wages and a sense of equality prevails. There arises no cause for jealousy and malice as all the workers doing similar jobs are rated at the same level. Such sense of equality among the workers helps in the smooth working of the organization

- Better quality – where the quality of products is more important than quantity or the materials worked upon are very costly, time wages prove cheaper than piece rates in their ultimate results

- Acceptable to trade unions – labor unions always prefer time wages since this form of payment doesn’t make any discrimination in wage matters between efficient and inefficient workers. This method ensures stable income for all the employees

Disadvantages

- Inefficiency – this system does not check employee’s inefficiency as there is no link between wages and productivity. The works may deliberately slow down the pace of work

- Lack of motivation – this system doesn’t provide any incentive to greater effort or harder work. It makes no difference between an efficient and a lazy worker and both are treated at the same footing

- Increased supervision – time wage system leads to lower productivity unless strict supervision is provided. Thus, there is need of close supervision to ensure better productivity

- Fixed wage bill – the monthly wage bill doesn’t fluctuate with the changes in production by workers, it is almost fixed. Thus, labor cost per unit fluctuates from month to month. Moreover wages have to be paid whether there is greater or less production

ADVANTAGES OF THE PIECE RATE METHOD OF PAYING WAGES

- Incentive for higher production – it provides an incentive to more efficient workers to produce more in order to earn higher wages.

- Lesser supervision – cost of supervision is less as the workers do not need constant supervision to lead them to work. The very attraction of greater reward for greater effort drives them to work harder.

- It provides the employers an easy way of determining labour cost per unit of product.

- Fairness – this system ensures fairness by correlating wages and productivity. The inefficient workers are penalized as they get less wages.

- Remedial transfer – under this system if a workers is constantly producing bad results, he may be shifted to another job. Thus, shifting of workers to jobs which suit them better takes place without creating difficulty.

- Economy – the total unit cost of production comes down with large output, because the fixed overhead burden can be distributed over a greater number of units.

Disadvantages

- Low quality – too much emphasis on the quantity of production may lower the quality of products.

- Strained industrial relations – the relations between workers and employers become sour if their output is low due to some fault of management.

- Insecurity to workers – the workers have a feeling of insecurity in their minds. They could get lower wages during a period when their efficiency may be reduced due to factors beyond their control. Thus, at times, the workers may be earning wages below the subsistence level.

- Difficulty in rate fixation – fixation of piece rates poses a problem for the management lower rates may lead to resentment on the part of the workers.

- More administrative work – introduction of piece rate will involve increased administrative work as production cards will have to be maintained for each worker. Daily record of production and rate of payment will have to be elaborately kept and preparation of pay-roll will entail a lot of calculations.

- Wastage – the workers will increase the speed of work and this naturally leads to speeding up of machinery wastage of materials, fuel and power. Thus may result in greater loss to the industry, excessive speed in running machines may cause breakdowns, accidents and frequent replacement resulting in loss of the organization.

- Health hazard – in their eagerness for increased earnings workers may exert themselves to the point of exhaustion as to undermine their health and efficiency.

- Opposition by trade unions – differences in earnings cause dissatisfaction and resentment to workers. Trade unions openly work against the piece wage system. They argue that this form of wage payment encourages rivalry between workers and endangers solidarity of labour unions.

- This method doesn’t ensure a stable monthly income for workers.

- This method cannot be applied to those jobs which are not easy to divide in small pieces.

GROSS PAY

- It refers to the total amount paid to an employee each pay period i.e. weekly or monthly. It includes regular pay, overtime pay, allowances, commission, bonuses and any other amounts before any deductions are made.

- Since a salary earner is paid one-twelfth of his annual pay at the end of each calendar month, his gross pay is frequently fixed for the year and therefore each month’s gross pay becomes a repetition of the previous month. This is common for all government employees and the executive in the private sector.

- Where in a factory, wages are paid based on the hours worked and rate per hour, the system becomes more complicated especially when computing the total hours worked for all employees. Thus a definite system of time recording must be devised.

TIME RECORDING METHODS

In order to accurately determine the number of hours worked daily, weekly, monthly, time records are necessary.

Methods used to record time

- TIME BOOK

Time is recorded in a book with names of employees on the left column and with ‘IN’ and ‘OUT’ columns on the right. When a worker comes in he writes his name and marks in the IN column what time he came, when going out he indicates in the OUT column the time he went out.

Advantages

- Easy method to understand

- Simple to operate

- Easy to maintain

- Cheap, doesn’t need any complicated or expensive machines

Disadvantages

- Open to fraud, workers can cheat the time of arrival or departure

- Signatures may be difficult to read

- TIME CARD

Every individual employee is given a weekly time card (known also as a clock card). A time recorder clock is placed near the entrance to the firm. When each employee arrives or departs he puts his time card into the machines and the time of arrival or departure is printed on it. All employees’ cards are kept in a rack. The time clerk is usually in charge of the rack. The rack is divided into sections, i.e. the ‘IN’ and ‘OUT’ rack.

Advantages

- Enables wages to be calculated

- A printed record of the exact number of hours worked is shown which removes the possibility of disputes

- The time card is an identification card for payment of wages

- A visual check on absenteeism can be made every morning by scrutinizing cards on the ‘out’ rack. If all employees are at work, the who of the OUT rack should be empty at say one hour after starting time

- Ordinary times are printed in black/blue, lateness and overtime are usually printed in red and are easily picked on the card when it comes to making up wages

Disadvantages

- A worker can clock on or off for other employees

- Card can mislaid or lost

- Cost of cards and labour in controlling and checking them is incurred

EXAMPLES OF TIME RECORDING MACHINES

- Autographic recorder

- Automatic time recorder

- Dial recorder

- Watchman’s detector

AUTOGRAPHIC RECORDER

It is a machine fitted with a clock and it controls a paper tape. When the employee presses the handle the time is automatically recorded on the tape and when he releases the shutter (blank section) over the tape he signs his name against the printed time. It is automatic hence labour saving, is fraud proof, reveals lateness and overtime and provides printed times for use in calculating wages but takes time to operate, is expensive and ideal for few employees.

AUTOMATIC TIME RECORDED

It is a very compact electric digital recording clock where the employee has to drop his card (plastic) in a slot (opening) and the machine automatically prints the details. It is fast but an employee can clock for another person and may demand supervision.

DIAL RECORDER

Is a machine fitted with a clock. When the employee rotates a lever the roll of paper moves until his pay number and name appears and he depresses the lever to record the time of arrival and departure. Time recording is strictly in payroll order, suitable for factories where dirty work is performed, the machine can accommodate a bigger roll of paper on which wage calculations can be made so that it is a combined time record and payroll but workers can clock on or off for other employees either purposely or accidentally and cannot be used for identify purposes like individual time cards.

WATCHMANS DETECTOR

Portable recorders are slung around the watchman’s neck. He clocks on with special keys located at the various patrol points. The paper tape helps to check on the wakefulness of the watchman and also enables security officer to vary the patrol guards against intending burglars.s

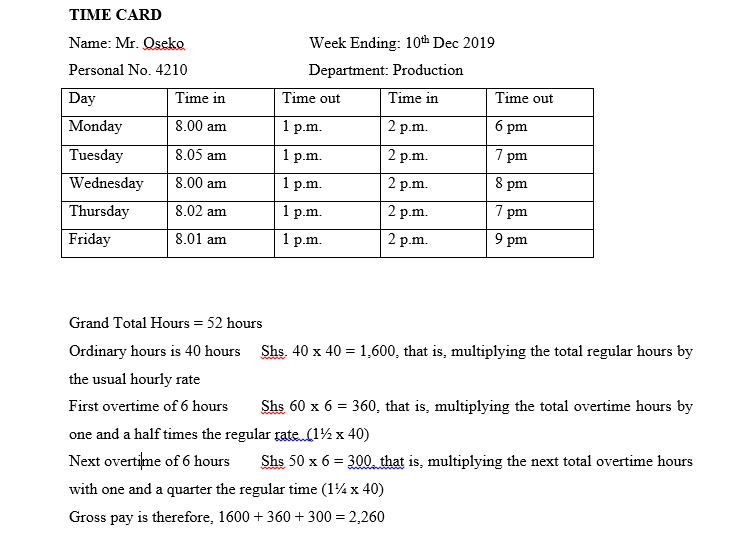

QUESTION

- Oseko works with ABC Company as a casual worker in the Production Department.

- His working day starts at 8.00 a.m. and ends at 5.00 p.m. every day Monday to Friday inclusive.

- He is given a lunch break at 1.00 p.m. to return at 2.00 p.m.

- His lateness allowance is 5 minutes.

- If he is late for more than 5 minutes that particular hour is not included as his working time.

- He is paid Ksh 40 per hour during the normal working hours.

- He is paid time and half for the first 6 hours of overtime and time and a quarter for any subsequent overtime worked.

- His personal number is 4210.

- His working hours for the week ending 10th Dec 2019 were as follows. Calculate gross pay

CALCULATING GROSS PAY

DEDUCTIONS FROM GROSS PAY

The rate agreed with an employer (whether calculated on an hourly, weekly or an annual basis) is the gross wage or salary. Before any wages are paid to employees, certain deductions are required to be made by law – otherwise known as Statutory Deductions. Other deductions are agreed by the employee (i.e. they are voluntary) and when all deductions have been totaled and taken away from the gross pay, the remainder (known as net pay) is paid to the employee.

- STATUTORY DEDUCTIONS

These are compulsory deductions authorized by an Act of Parliament

- Pay As You Earn (PAYE)

It is deducted weekly or monthly from everyone with a regular income. It is collected by the employer and paid on behalf of employees to income tax department.

The amount to be deducted from the employee’s gross pay varies with:

- Amount earned

- Marital status

- Free pay – the amount of income below which an employee is not taxed

- Personal relief – this is the amount deducted from income tax. It depends upon single or married status

- The number of non-taxable allowances claimed such as insurance premiums etc.

Advantages

- Taxes are collected on a regular basis each week or month by employer from all their employees

- Employer sends a bulk cheque to the collector of taxes once a month

- The government is assured of receiving all income tax due

- Revenue authorities do not have to collect money from individuals

- The employee does not have to take tax to the collector

- The amount of tax the employee pay is related to his actual earnings

NATIONAL SOCIAL SECURITY FUND

- It was established in 1965 through an Act of Parliament.

- It is a pension plan or retirement plan where the employees benefit in old age or his family in case he dies before retirement.

- The amount of pension is dependent on the total number of years of service by the employee and the last pay drawn by him.

- The employee receives his/her pension until death. A pension is an arrangement to provide people with an income when they are no longer earning a regular income from employment.

Benefits/advantages of N.S.S.F

- Members are paid their saving plus interest upon retirement at the age of 55 years or above

- Helps to maintain the same standard of living after retirement

- In case of a members death his/her dependents receive the pension

- Pensions are tax exempt

- Pension plans provide employers with a tool in retaining workers, incapacitated through accidents or disease. When they can no longer work NSSF pays them invalidity benefits

N.H.I.F. (National Hospital Insurance Fund)

- It is a health insurance scheme where the employee gets paid for hospitalization costs.

- It is contributed monthly by an employee.

- It registers all eligible members from both the formal and informal sector.

- Formal sector employee’s contributions are deducted and remitted to the fund by their employers.

- The amount depends on one’s salary.

Benefits of N.H.I.F

- Upon admission in hospital an NHIF member is accorded services and the hospital makes a claim to the fund for reimbursement

- All in-patient cover for the contributor, declared spouse and children

- Comprehensive maternity and caesarian (CS) package in government hospitals, majority of mission and some private hospitals.

WCPS – WIDOWS AND CHILDREN PENSION SCHEME

Under this scheme the Widow and Children receives pension when the bread winner/husband dies if he was a member of this scheme.

Advantages of W.CP.S

- Reduces number of street children

- Cut down illiteracy and poverty

- Promotes general health of wife and children

VOLUNTARY DEDUCTIONS

These are deductions made at the request of the employees

- Insurance – where the employee pays premiums bases in the type of policy taken e.g. life, education etc.

- Saving scheme contributions e.g. cooperative society shares

- Trade union dues

- Loan repayment e.g. car loan, bank loan, cooperative loans

- Contribution to social clubs e.g. lion club, Meru sports club

- Mortgage repayments

NET PAY

The net pay is the amount that remains after statutory and voluntary deductions are taken away from the gross pay.

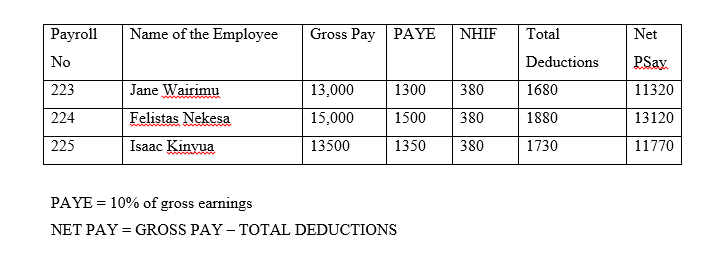

PAYROLL/WAGES BOOK

- Contains a list of all names of individual employees, their personal numbers, gross pay, all deductions both compulsory and voluntary and net pay.

- The following details relates to employees at Haraka Transporters Ltd

- Jane Wairimu, payroll number 223, basic salary sh 10,000, overtime sh 3000

- Felistas Nekesa, payroll number 224, basic salary 15000, overtime Nil

- Isaac Kinyua, payroll number 225, basic salary sh 13500, overtime sh 500

- Each employee pays NHIF at sh 380 per month and PAYE which is calculated at 10% of the gross earnings

- Prepare a payroll showing their net salaries at the end of the month

PAY ADVICE OR PAY SLIPS

- It is a small document mainly a slip of paper which contains records of an employee wage or salary including details of deductions made.

- It is issued by employer to all employees in every organization at the end of every pay period e.g. week or month.

- It may be sent before the payment day or included with his pay packet.

- A pay packet is a special envelope which bears the employees name, code number, and department.

- Wages are paid in these envelopes.

QUESTION

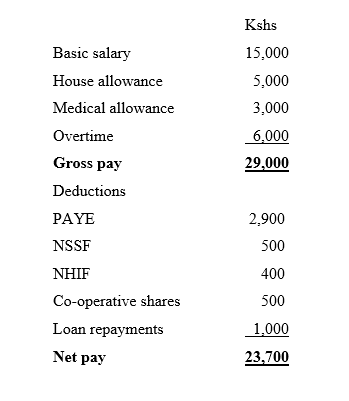

- Mwanaisha Rajab, Personal No. 7814 is employed by Kwality Services Limited as a clerk is the Company Secretary Department.

- Her basic salary is Sh. 15,000 per month.

- She is paid Sh.5,000 as house allowance and Sh. 3,000 as medical allowance monthly.

- In the course of last month she worked 20 hours overtime at the rate of Sh. 300 per hour.

- The deduction made from her salary includes PAYE at 10%, NSSF sh 500, NHIF sh 400, cooperative shares sh 500 and loan repayment sh 1,000.

- Draw up Mwanaisha’s Rajab pay slip for last month

KWALITY SERVICES LTD

Month: January Personal No 7814

Name: Mwanaisha Rajab Department: Company Secretary

Jot Title: Clerk

STEPS IN WAGES SYSTEM OR PREPARATION

- Each employee is given a pay number

- He/she is listed on a payroll (wages book)

- Gross pay is calculated from attendance or work record, depending on whether earnings are paid on a time or piece work basis

- Gross pay is entered on the payroll together with details of all deductions both voluntary and compulsory

- Net pay is calculated by taking all deductions away from gross pay

- Details of gross pay, personal tax and national insurance deductions are entered on employee tax deduction cards

- Pay statements (pay slips) are prepared together with pay envelopes

- A coin and not summary is drawn up to calculate the numbers of notes and different coin required to make up the pay packets

- The total of net pay is drawn from the bank and individual amounts of notes and coins are placed in pay envelopes

- Pay envelopes are distributed to employees

NB: There are a variety of wages and salary procedure but whatever the system used by a particular organization, the basic essentials are the same.

USES OF A WAGES SYSTEM IN AN ORGANIZATION

- To calculate and pay the employees the correct amount to which they are entitled

- To record the differences between gross and net pay, i.e. to record all deductions from pay

- To allocate these deductions to their respective funds or other purposes

- To calculate individual and total pay according to a timetable, so that it can be paid out at the recognized times

- To compile wagess in such in a way that the records can also be used for costing purposes

DUMMY WAGES

The term dummy wages is applied to the payments of money to non-existent workers entered on the payroll with bogus/false names and is a common method of embezzling from the firms cash

MEASURES TO PREVENT FRAUD IN WAGES SYSTEM OR IN A SALARIES SECTION or WAYS OF PREVENTING DUMMY WAGES

- Divide the duties between different members of the staff e.g. for the calculation, drawing cash from the bank, paying out

- Regular agreements of the names on the payroll with the staff records

- Undertake an internal audit at irregular intervals and preferably at the time of paying out

- Obtaining a signature of all wages paid or the production of a time card

- Have a definite system from dealing with unclaimed wages each week

- Periodically check on pay number issued by personnel department and on the pay numbers on the payroll

- Periodically check the payroll with national insurance cards at hand

- Pay wages as well as salaries by cheque or credit transfer

- Having good quality staff and adequate supervision

- Use a security firm e.g. Securicor to carry money to and from the bank or employees going in pairs

METHODS OF PAYMENT OF WAGES s

- Cash – where payment is made in cash, the notes and coins are enclosed in pay envelope. It is important when drawing cash from the bank to pay wages and salaries to obtain the correct amount of notes and coins. These ensure that the exact amount can be placed in each employee’s envelope. In this case preparing a coin and not summary before going to the bank helps a lot.

- By cheque – it is an order in writing addressed to the bank to pay when required a sum of money to the person named on the cheque. Payment by cheque saves the work involved in making up pay packet. It eliminates also the risk of theft through ‘wages snatch’. But it is a disadvantage to employee because a cheque is either paid into an account or cashed. Many employees do not have bank accounts and bank opening hours may be inconvenient for people in full time work

- Credit transfer – in this method the employer prepares schedules, listing the names of their employees, their banks, their account numbers and the amount to be paid and a cheque is made drawn up for the total amounts. When the bank receives the schedule lists and the cheques, it ensures that all amounts due to employees are paid into their respective accounts. It’s a requirement for each employee to have a bank account.

MACHINES USED IN WAGES CALCULATION/MECHANIZATION OF THE WAGES SYSTEM

- Time recorder machine – for recording time and attendance

- Calculation and adding machines – for computation of wages

- Cheque writing or cheque signing machine

- Note counting and coin counting machines

TIME KEEPING

Reasons for Time Keeping

- Actual hours worked are known for the purpose of calculations

- Promotes punctuality which improves overall efficiency of the office

- Act as a disciplinary check on workers

- To avoid a worker arriving late which can interrupt the work of others

- Workers arriving late are breaking the contract of employment which prescribes a certain number of hours duty

- Widespread lateness which can have a bad psychological effects on workers

WORKING TIME

- Time that an employee is actively engaged in production

- Long breaks and lunch break are excluded from working hours

- Tea breaks are usually included in working hours

Example

- Kenya Civil Servants work for 18 hours a day (40 hours a week)

- Lunch break is excluded from the working hours

- These working time (hrs) is what is usually referred to as normal working hours

- In most company’s the normal salary for an employee is based on these hours

- No time during the days 24 hours is not working time. Some organizations work is carried out in shifts.

OVERTIME

Refers to the time that an employee is engaged in productive activities of his employer above the regular working time. For example,

- Before start of work – 6.00 to 8.00 am

- After work – 5.00 to 7.00 pm

- Weekend starts to Sundays

- Holidays etc.

- Overtime is usually paid at a predetermined rate that is usually higher than the normal rate, for example, 1½ the regular rate.

ILLUSTRATION

Regular Ksh 40

Overtime rate 1½ times regular

3/2 x 40 = Ksh 60

BENEFITS OR REASONS WHY ORGANIZATIONS HAVE OVERTIME

- To deal with excessive amount of work or bottle necks, e.g. during busy periods

- Assist in finishing an urgent project before the deadline

- It covers staff absences

- Helps to clear seasonal workloads e.g. annual stock taking

- Ensures staffs shortages are catered for without the need to recruit extra staff

- Helps in the avoidance of disruption of jobs where the workload is more difficult to share e.g. transport and driving

- To increase production temporary without increasing the number of workers

- When workers are slow in completing their work

DISADVANTAGES of Overtime

- Continuous overtime fatigues the workers leading to reduced productivity and errors in work

- May make workers produce below their capacity during the regular time in order to create work for overtime

- Overtime affects the organization where extra money is paid to the employee which is costly to the organization

- Employee expectations of overtime, leading to resentments and inflexibility if you try to withdraw it

- Regular long working hours can adversely affect employees health and family life

Flextime (Flexible Working Hours )

- Recent development in management of working hours is giving the individual worker freedom to determine a work schedule that fits him best.

- The results of these development is flextime or flexible working hours whereby a worker can attend the office when he chooses as well as leaving off work at their own discretion provided they are in the office during certain hours laid down by the companies.

- Flex time is a program allows employees to decide their own the starting and ending time for their days.

- Employees usually fix the earliest and latest time allowable for work

- They also fix a time or times when all employees are expected to be at work. This period is referred to as the CORE TIME.

- The time period within which employees choose their starting and ending time constitutes a flexible band.

ILLUSTRATION OF FLEXTIME

7.00 to 8.00 am – starting flexible band

9.00 to 11.00 am – Core time

11.00 to 1.00 pm – Lunch break flexible band

1.00 to 4.00 pm – Core time

4.00 to 6.00 pm – quitting flexible band

NB: Each employee is expected to work for the total required hours per day/week/month

These arrangements assumes presence of up-to-date time recording equipment

ADVANTAGES OF FLEXTIME

- Results to less absenteeism and sickness – employees have time to visit their doctors and also attend to pressing personal matters within the flexi-time band

- Helps overcome or reduce difficulties encountered in travel during the rush hours e.g. traffic jam

- Improves staff morale – staff feels recognized when they participate in deciding on arrival and departure times

- May result with the improvement in the staff family care, e.g. mothers may decide to start work late in order to attend to pressing domestic issues before they leave. Mothers may also decide to take long lunch breaks in order to go shopping

- Leads to reduced/eliminates overtime payment – workers may decide on their arrival and departure times in blocks resulting in shifts

- Reduces need for supervision for hours of attendance – people are responsible of their own time affairs

- Increased productivity per worker – cultivates greater sense of responsibility in workers

- Reduces labour turnover, that is, the rate at which employees leave an organization

- Workers can plan their days with certainty

- Useful when introducing longer working day without extra cost to the employer

Disadvantages

- It may mean paying extra expenses for supervision in case employee choose to attend extra early or extra late

- Where jobs are related, a late arrival of one person may prevent others from working. Some sections may fail to function if other complementary section workers haven’t arrived. Time can only be effective where work is self contained

- May not convenient for customers and business associates who may be willing to talk to particular personnel

- Loss of dignity of having to clock in and out

- Workers may not be able to earn overtime pay

- In case of an urgent matter management may fail to contact all the staff members unless it falls on the core time

- Create difficulties in keeping track on the hour worked by each employee

- It may entail extra overhead expenses (electricity, water ) because the firm is opened for longer hours

FACTORS THAT DETERMINE THE WAGES AND SALARIES OF EMPLOYEES BY AN ORGANIZATION

- The firm’s capacity to pay – those firms enjoying higher profits, higher turnover and higher rate of return over investment can afford to pay higher wages than those firms which are running into losses or enjoying lesser profits.

- Demand and supply of labour at the national, regional, local and organizational levels. If demand for labour is high, the wage rate tends to be high, if the labour supply is scarce, the wage rate would be high.

- The existing market wage rate – unless and until a firm maintains the minimum wage offered by the competitors, it cannot retain the labour force because a higher wage rate elsewhere may motivate the labour to step out and join elsewhere where the wage rate is high. To retain, attract and maintain a sufficient quantity and quality of manpower, a firm should consider the existing wage in the market.

- The cost of living – the wage rate should be based on the increase or decrease in the cost of living index. When the cost of living increases workers demand increase in pay. When the cost of living index goes up substantially a revision of wage structure is called for.

- Living wage – this is the wage which should enable the earner to provide for himself and his family not only the basic essential of food, clothing and shelter but a measure of comfort including education for his children, etc.

- Job requirements – wage structure is based on relative skills required to do the job, effort needed, responsibility and authority imposed upon and the job conditions.

- Productivity of labour – this is measured in terms of output per man-hour

- Managerial attitudes – the top management desire to maintain and enhance the company’s prestige has been a major factor in the wage policy of a number of firms.

- Psychological and social factors – wage equity, fairness and justice are essential in meeting the psychological and social satisfaction to the employees at work.

ACCOUNTING SERVICES IN OFFICE ORGANIZATION

These refer to the accounting functions and responsibilities. They include:

- Keeping records of all purchases and sales and sums of money owing to and by the company, that is, account receivables (money due to the company) and accounts payable (money due from the company). That is maintaining financial records of the company

- Preparing of the final accounts or annual accounts to show either a profit or loss on the firm’s operations during the year – to be presented to the shareholders at the annual general meeting to give them information on the current financial position of the company.

- Preparation and payment of wages and salaries

- Paying tax liability of the organization and other deductions e.g. National Insurance, staff pension fund, sports or social club or trade union dues.

- Placing money value on those items which represent the capital of the company, land, building, fixtures, equipment, machinery and vehicles.

- Cost control – working out of detailed figures in regard to the cost of each article manufactured such as cost analysis enables to keep a close check on costs and any deviation from the agreed levels can be quickly seen and investigated.

- Credit control – to investigate the credit worthiness of customers

- Carry out internal audit so as to discover any errors or fraudulent attempts to tamper with accounts.

- Processing invoices

- Writing out cheques for issue to creditors

- Collecting debts by maintaining the debt ledger accounts

- Budgeting control – the accounts department allocates revenue and charges expenditure to the departments

FINANCIAL PROBLEMS OF BUSINESS

- Insufficient or no financing – without a constant flow, a business is in trouble. Businesses need money continuously.

- Poor cash management – even highly profitable businesses need to manage the money that comes in. Manage accounts receivables aggressively; don’t be afraid to collect from people who owe you.

- No budget – every business needs a budget to plan for regular expenses such as utility bills, rent and wages. Estimate their costs over a period of time such as a year and set aside cash each month to continue paying them. Don’t forget to set aside money monthly for bills that come due quarterly, semi-annually or annually so you are not caught short of cash.

- Putting off difficult decisions – putting off making hard choices almost costs money. Write down the problem. List all possible solutions. State the good and bad of each decision. Choose the best one. Assess risks carefully evaluating them against your company’s strategic plan. Taking risks contrary to your business goals, mission and purpose lead to financial trouble. Always weigh the risk versus the potential reward.

- No strategy – from the beginning to end, you business should have a plan. Begin with the end in mind. Write a formal business plan and use it as a road map, checking off mileposts as your business grows. A plan helps you increase cash flow, estimate budgets and determine when you need additional financing. Create an income and expense pro forma and monitor it monthly.

Cash control measures

- Check sums of money carefully when receiving and paying them

- Lock any cash held in the office in the office in a cash box and keep in a safe

- Never leave the office unattended with the cash box unlocked

- Ensure that every payment of cash is supported by a voucher or receipt

- Pay money into the bank as soon as possible after receipt to avoid the security risk of holding money on the premises

- If large sums of money have to be transported to and from the bank a security agency staff will normally be employed. If the office staff have to undertake this task, the people should be using a specially designed cash carrying case and if regular journeys are made, vary the route taken.

- Spot checks should be made regularly on any transactions involving the transfer of money

- Do not leave wallets or handbags in your office

STAFF RECORDS

It is the duty of the Personnel Department to open a file under the name of the new employee and also provide him/her with a personal number.

It is in this file that all correspondence between him or her and his employer will be filed and kept.

Examples of correspondence in an employee file include:

- Letters or form of application

- Copies of his/her certificates, that is, academic or professional

- Letters from referees

- Record of the interview

- Medical reports

- Letter of appointment

- Letters from his/her immediate manager

- Performance records

- Leave records, for example, annual, sick leave, maternity etc

- Training records

- Health and Safety records

- Wage and Salary records

- Any other correspondence

These testimonials are kept in the employee’s personal file.

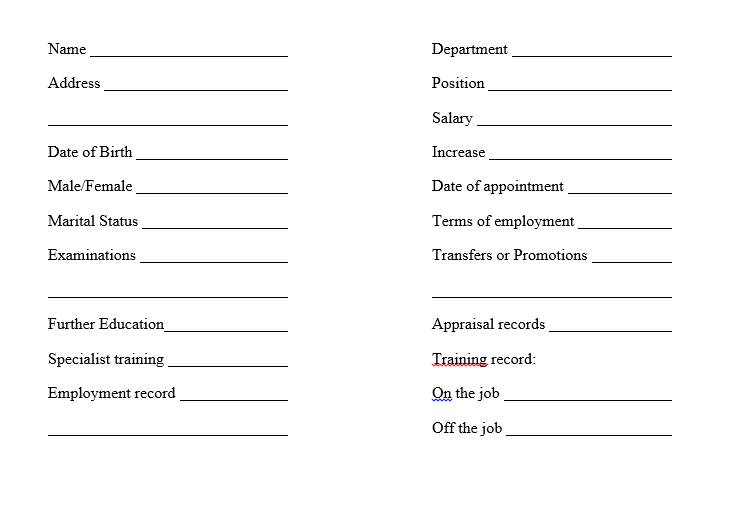

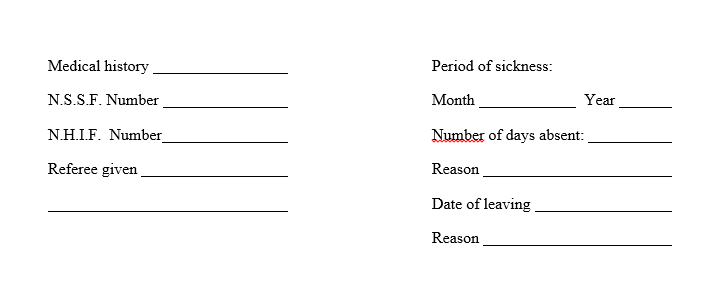

At the same time the Personnel Department completes a PERSONNEL RECORD CARD, containing summarized details relating to you as an employee.

PERSONNEL RECORD CARD

This card contains important information in his file and may be filed separately so as to make the employee record available at the point of use or to enable speedy location when needed.

EXAMPLE OF A PERSONNEL RECORD CARD

The Personnel Record Card shows:

REASONS FOR MAINTAINING PERSONNEL RECORDS

- Reference may be wanted for personal data, for example, age, date of birth, address, marital status.

- Age helps to know when a person is retiring.

- Marital Status enables to give family or single relieve

- Acts as a basis for promotion by looking at the experience an employee has on the job staff records and details of qualifications

- Acts as a basis for disciplinary action, for example, a record of lateness means need for employee to be disciplined

- Help in deciding the kind of training an employee should undergo, for example, if he is supervisor give supervisory training

- Helps to know whether an employee’s salary need to be increased by referring to the salary or wage

- In case of holidays or sickness give pay if the company offers the leave with pay

- Pension – Calculation of pension by referring to the period employee has worked and salary paid

- Income tax purposes – amount of tax to pay after giving their required relieve

- Giving of references to employer in other organizations

- Giving or refusing transfers

- Acts as a basis for merit rating (Staff appraisal)

- Working out the number of employees, deciding on recruitment of staff and turn-over

- To comply with the provisions of various industrial labour laws.

GUIDELINES THAT SHOULD BE FOLLOWED WHEN MAINTAINING PERSONNEL RECORDS or The principles of record keeping

- The purpose for which the record is kept must be justifiable. If the records are maintained without any justifiable purpose, it will amount to a waste of time, money and space.

- Records must be capable of verification. A record which is not capable of verification is of little value.

- Records must be classified – records may be classified (a) according to time or chronologically (b) according to subjects, so as to be useful for analysis.

- The requisite information must be available when needed. The main objective of keeping the records is to provide the information when needed with speed and accuracy. It is of no use to keep records if they cannot be made available when asked for.

- Records must be provided and maintained at a reasonable cost – The cost of maintaining and providing records should be justifiable in the usefulness for taking decisions. That means the maintenance of records should be effective and economical.

- Records must be precise. Records should be maintained in a concise form so that valuable space is not wasted.

- The system of record keeping must be elastic so that it may be explained or contracted according to the circumstances.

CONTRACT OF EMPLOYMENT or TERMS OF EMPLOYMENT

It is the duty of all employers to give employees a written statement of the main terms of employment not later than thirteen weeks after employment has begun. This is to avoid a lot of problems caused due to misunderstanding – not knowing how much you are to be paid, how much leave you are entitled to, the hours of work and so on. When you start working you should be given a Contract of Employment.

This contains such useful information as:

- Your name and the name of the firm

- The date you started work

- The date the contract was issued

- The amount of pay and how it is paid – weekly or monthly and your status or designation

- Details relating to holiday entitlement and holiday pay like overtime or piecework rates.

- Hours of work and days of work

- What happens to your pay if you are sick, that is, if there are provisions for sick pay

- Details of pensions and pension schemes

- The amount of notice to be given by either party to terminate the contract

- Whom to contact if you have any problem

- Any other information – for example, Many firms include a list of their own rules on the employment contract, for example, “The company does not allow use of telephone for private calls except in emergency cases.

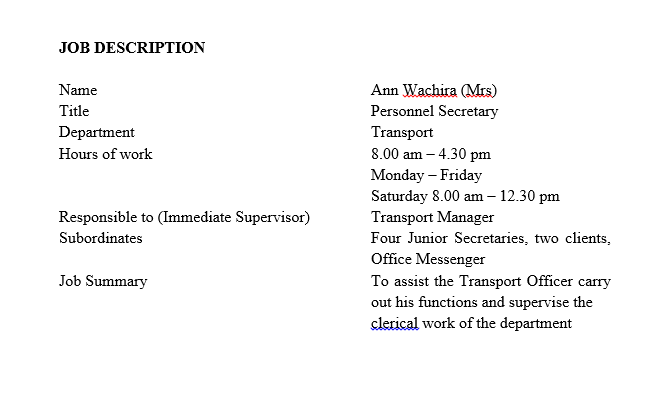

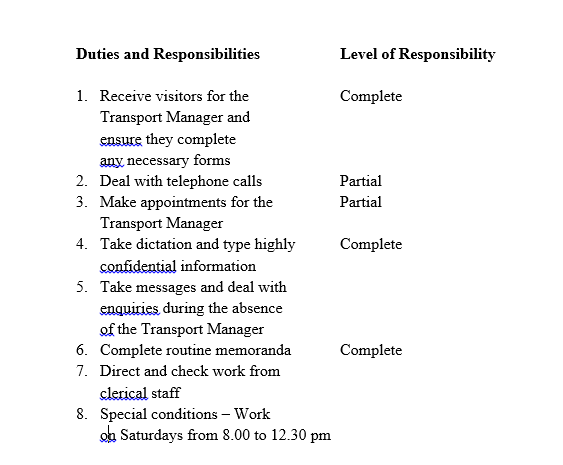

JOB DESCRIPTION

It is an organized, factual statement of the duties and responsibilities of a specific job.

TYPE OF INFORMATION IN A JOB DESCRIPTION

- Title of the job

- The aim or function of the job

- Immediate supervisor/superior, that is, the person the job holder is directly responsible to

- His/her subordinate, that is, the person(s) answerable to him/her or whose work he/she must supervise

- Duties or activities to undertake in order to fulfill the function

- Any special conditions, specific information or limited which apply to the job and which the employee should be aware of

REVISION QUESTIONS

- Give two reasons for using analysis columns in a petty cash account

- The following are statutory deductions made from employee’s salaries. Write the abbreviations in full and state the benefit of each deduction

- NHIF

- NSSF

- PAYE

- WCPS

- Name three columns that must be included in a petty cash form other than the date and amount columns

- Name two documents that are used to operate an effective imprest system

- Highlight three benefits that accrue to an employee who is engaged on permanent and pensionable terms

- Explain the following methods of calculating wages and state one advantage of each

- Flat rate

- Piece rate

- Bonus rate

- Commission

- As a secretary you have noted that the money set aside for petty cash is often misused. State three ways in which you would deal with this problem

- List three ways of calculating wages

- Rafiki textiles Limited operates its petty cash book using the imprest system with an initial cash float of Ksh. 5,000. The following payments were made in the month of June 2018.

2018 Ksh

June 1 Paid travelling expenses 550

4 Bought cartridge 720

6 Bought postage stamps 120

Paid fare for the messenger 500

21 Bought printing papers 900

23 Bought foolscaps 800

Prepare a petty cash book for the month ending 30 June 2018 and balance it. Use the following analysis columns for the expenses: Postage, Transport and Stationery (10 marks)

- Explain six items that should be included in a job description (9 marks)

- Explain four types of allowances paid to employees (8 marks)

- Give four reasons why employers must maintain accurate staff records (8 marks)

- Highlight three confidential records that may be found in the Human Resources Department

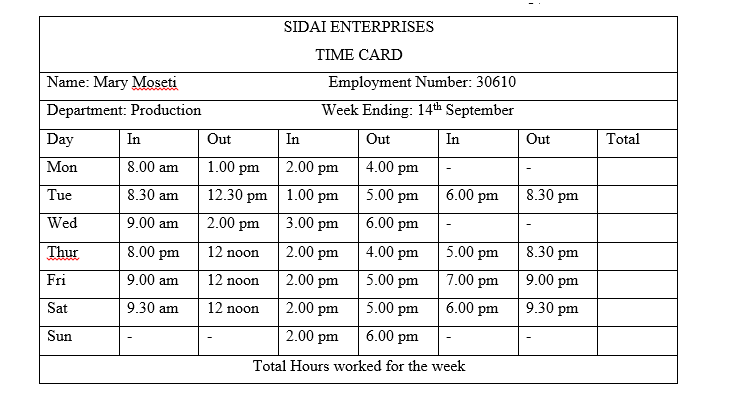

- Mary Moseti is employed by Sidai Enterprises as a Packaging Assistant. She is required to work for a minimum of 40 hours a week at a rate of Kshs. 300 per hour. She is paid double for any extra hour worked during the week. The following time card shows the time she reported for work and checked out during the week ended 14thseptember

Calculate:

- The total number of hours Mary worked for the week

- Mary’s gross wage for the week (9 marks)

15. Lucy earns a basic salary of Ksh. 10,000. She is paid commission on sales at the following rates:

Sales Value Commission

First Ksh 500,000 4%

Next Ksh 500,000 7%

Sales in excess of Ksh 1,000,000 11%

During the month of May, Lucy sold goods worth Ksh 1,600,000. Calculate Lucy’s earnings for the month of May. (9 marks)

16. You are a secretary in the Personnel Department. Your boss has asked you to draft a contract of employment for a new employee. Enumerate the points that would be included in such a contract. (9 marks)