1 Introduction

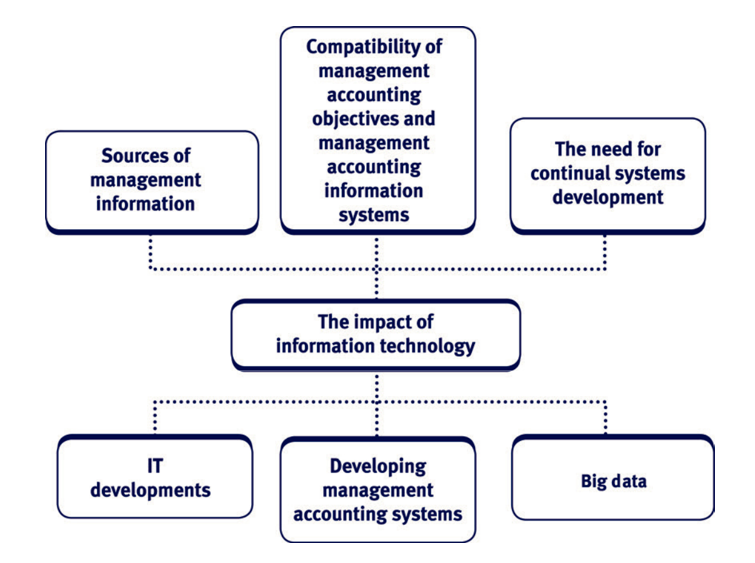

Managers need access to good information in order to be able to effectively plan, direct and control the activities that they are responsible for. The first part of this focuses on the sources of management information and on the development and importance of an effective management accounting information system.

The then goes on to look at some IT developments and discusses how advancements in technology have allowed managers instant access to data and have enabled remote input of data.

2 Sources of management information

2.1 Introduction

Managers need information for planning and decision making and in order to manage and control their organisations effectively. As a result, managers will need a range of internal and external information.

2.2 Internal sources

Internal sources of information may be taken from a variety of areas such as the sales ledger (e.g. volume of sales), payroll system (e.g. number of employees) or the fixed asset system (e.g. depreciation method and rate).

Examples of internal sources of information

| Examples of internal data: | |||||

| Source | Information | ||||

| Sales ledger system | | Number and value of invoices | |||

| | Volume of sales | ||||

| | Value of sales, analysed by customer | ||||

| | Value of sales, analysed by product | ||||

| Purchase ledger | | Number and value of invoices | |||

| system | |||||

| | Value of purchases, analysed by supplier | ||||

| Payroll system | | Number of employees | |||

| | Hours worked | ||||

| | Output achieved | ||||

| | Wages earned | ||||

| | Tax deducted | ||||

| Fixed asset system | | Date of purchase | |||

| | Initial cost | ||||

| | Location | ||||

| | Depreciation method and rate | ||||

| | Service history | ||||

| | Production capacity | ||||

| Production | | Machine breakdown times | |||

| | Number of rejected units | ||||

| Sales and marketing | | Types of customer | |||

| | Market research results | ||||

2.3 External sources

In addition to internal information sources, there is much information to be obtained from external sources such as suppliers (e.g. product prices), customers (e.g. price sensitivity) and the government (e.g. inflation rate).

Examples of external sources of information

| External source | Information | ||

| Suppliers | | Product prices | |

| | Product specifications | ||

| Newspapers, | | Share price | |

| journals | | Information on competitors | |

| | Technological developments | ||

| | National and market surveys | ||

| Government | | Industry statistics | |

| | Taxation policy | ||

| | Inflation rates | ||

| | Demographic statistics | ||

| | Forecasts for economic growth | ||

| Customers | | Product requirements | |

| | Price sensitivity | ||

| Employees | | Wage demands | |

| | Working conditions | ||

| Banks | | Information on potential customers | |

| | Information on national markets | ||

| Business enquiry | | Information on competitors | |

| agents | | Information on customers | |

| Internet | | Almost everything via databases (public and | |

| private), discussion groups and mailing lists | |||

Test your understanding 1

Required:

What are the limitations of using externally generated information?

2.4 Use of internal and external information in performance management

The internal and external information may be used in planning and controlling activities. For example:

- Newspapers, the Internet and business enquiry agents (such as Dun and Bradstreet) may be used to obtain external competitor information for benchmarking purposes.

- Internal sales volumes may be obtained for variance analysis purposes.

Test your understanding 2

Required:

Briefly explain the use of customer data for control purposes.

2.5 The costs of internal and external information

The benefit of management information must exceed the cost (benefit > cost) of obtaining the information.

Benefits and costs of information

The design of management information systems should involve a cost/benefit analysis. A very refined system offers many benefits, but at a cost. The advent of modern IT systems has reduced that cost significantly. However, skilled staff have to be involved in the operation of information systems, and they can be very expensive to hire.

Let us illustrate this with a simple example. Production costs in a factory can be reported with varying levels of frequency ranging from daily

(365 times per year) to annually (once per year). Costs or benefits of reporting tend to move as follows in response to increasing frequency of reporting.

- Information has to be gathered, collated and reported in proportion to frequency and costs will move in line with this. Experience suggests that some element of diseconomy of scale may set in at high levels of frequency.

- Initially, benefits increase sharply, but this increase starts to tail off. A point may come where ‘information overload’ sets in and benefits actually start to decline and even become negative. If managers are overwhelmed with information, then this actually starts to get in the way of the job.

An information system is just like any part of a business operation. It incurs costs and it offers benefits. In designing an information system, the accountant has to find some means of comparing the two for different options and determining which option is optimal. In this sense, system design follows the same practices for investment appraisal and decision making which are explored later in this text.

In the above case it can be seen that net benefits (benefits less costs) are maximised at around 120 reports per year – suggesting an optimal information cycle of about 3 days. The system should be designed to gather, collate and report information at three-day intervals. This is an over-simplified example but it serves to illustrate a general logic which can be applied to all aspects of information system design.

The costs of information can be classified as follows:

| Costs of internal information | Costs of external information |

| Direct data capture costs, e.g. the cost | Direct costs, e.g. newspaper |

| of barcode scanners in a supermarket. | subscriptions. |

| Processing costs, e.g. salaries paid to | Indirect costs, e.g. wasted time finding |

| payroll processing staff. | useful information. |

| Indirect costs, e.g. information | Management costs, e.g. the cost of |

| collected which is not needed or is | processing information. |

| duplicated. | |

| Infrastructure costs, e.g. of systems | |

| enabling Internet searches. |

- Compatibility of management accounting objectives and management accounting information systems

Management accounting systems must be capable of producing performance and control information that is consistent with the objectives of the management accountant. Management accounting information may be used to:

- assess the performance of the business as a whole or of individual divisions or products

- value inventories

- make future plans – the provision of management accounting information may assist in making future business plans

- control the business – for example, through variance reporting

- make decisions – for example, through the provision of summary information (which can be used to make strategic decisions) or through the provision of more detailed information (which can be used to make tactical and operational decisions).

The information is only useful to the management accountant if it is:

- aligned to the objectives of the management accountant

- relevant – to the needs of the user

- accurate and complete – to inspire confidence in the user

- timely – in the right place at the right time

- appropriately communicated – using a suitable format and communication medium

- cost < benefit.

Illustration 1

Many organisations are aiming to improve efficiency and minimise wastage through the adoption of a lean philosophy (see 13 for further discussion). This organisational objective will directly impact the objectives of the management accountant (since alignment of objectives is necessary). As a result, the management accountant will require an information system that has been simplified, is efficient and keeps wastage down to a minimum. This may, for example, result in the provision of information to the management accountant which is simple to read and is instantly accessible.

4 Developing management accounting systems

4.1 What is a management information system?

A management information system (MIS) converts internal and external data into useful information which is then communicated to managers at all levels and across all functions to enable them to make timely and effective decisions for planning, directing and controlling activities.

4.2 What makes an effective MIS?

An effective MIS will:

- define the areas of control within the organisation and the individuals who are responsible for those areas

- ensure that the relevant information is communicated and flows to the managers in charge of those areas.

4.3 Types of MIS

There are a number of key types of MIS:

| Type of MIS | Explanation | ||

| Executive information | An EIS gives senior executives access to internal and | ||

| system (EIS) | external information. Information is presented in a user- | ||

| friendly, summarised form with the option to ‘drill down’ | |||

| to a greater level of detail. | |||

| Decision support | A decision support system aids managers in making | ||

| system (DSS) | decisions. The system predicts the consequences of a | ||

| number of possible scenarios and the manager then | |||

| uses their judgement to make the final decision. | |||

| Expert system | Expert systems hold specialist knowledge, e.g. on law | ||

| and taxation, and allow non-experts to interrogate them | |||

| for information, advice and recommended decisions. | |||

| Can be used at all levels of management. | |||

Test your understanding 3

CB publishing is considering the impact of a new system based on an integrated, single database which would support an executive information system (EIS) and a decision support system (DSS). A network update would allow real time input of data.

Required:

Evaluate the potential impact of the introduction of the new system on performance management.

Test your understanding 4

Required:

Discuss the factors that need to be considered when determining the capacity and development potential of a management information system.

5 The need for continual systems development

Information and management accounting systems need to be developed continually otherwise they will become out of date either because of advances in technology or because of environmental changes.

Change will be required to maintain or improve the performance of the system in an increasingly competitive and global market.

Test your understanding 5

Blueberry is a quoted hotel resort chain based in Europe. It is considering the use of an activity-based management approach and has identified five activity areas (cost pools) and cost drivers.

The company has recently invested in a ‘state of the art’ IT system which has the capability to collate all of the data necessary for budgeting in each of the activity areas.

Required:

Explain the problems that Blueberry might experience in the successful implementation of an activity-based costing system using its recently acquired ‘state of the art’ IT system.

Test your understanding 6

Lead times are becoming increasingly important within the clothing industry. An interesting example of a company going against the conventional wisdom is Zara International, part of the Inditex group (Spain).

- Zara produces half of its garments in-house, whereas most retailers outsource all production. Although manufacturing in Spain and Portugal has a cost premium of 10 to 15%, local production means the company can react to market changes faster than the competition.

- Instead of predicting months before a season starts what women will want to wear, Zara observes what is selling and what is not and continuously adjusts what it produces on that basis. This is known as a ‘design-on-demand’ operating model.

- Rather than focusing on economies of scale, Zara manufactures and distributes products in small batches.

- Instead of using outside partners, Zara manages all design, warehousing, distribution, and logistics functions itself.

- The result is that Zara can design, produce, and deliver a new garment to its 600-plus stores worldwide in a mere 15 days.

By comparison a typical shirt manufacturer may take 30 days just to source fabric and then a further ten days to make the shirt. For some firms overall lead time could be between three and eight months from conception to shelf.

Required:

Comment on the importance of IT systems to Zara’s competitive strategy.

6 IT developments

There has been a wealth of IT developments. These include:

Data warehouses

A data warehouse is a:

- Database: data is combined from multiple and varied sources (internal and external) into one comprehensive, secure and easily manipulated data store. A unified corporate database allows all users to access the same information, to see an overall picture of performance and helps inform business decisions.

- Data extraction tool: data can be extracted from the database to meet the individual user’s needs.

- A decision support system: data mining is used to analyse the data and unearth unknown patterns or correlations in data.

Illustration 2 – Influence of IT on Sainsbury plc

Sainsbury plc, the UK supermarket giant, has a data warehouse with information about purchases made by the company’s eight million customers.

Transactional details are tied to specific customers through the company’s Nectar loyalty programme, producing valuable information about buying habits.

Initial analysis of the information quickly showed Sainsbury’s how ineffective its traditional mass-mailing approaches were – where large numbers of coupons were widely distributed in an attempt to get customers through its doors. Rather than buying more, many customers would cherry-pick the specials and go to its competitors for other items. This meant many advertising campaigns were running at a loss.

Since those initial findings, a concerted focus on timely data analysis and relevant marketing has helped Sainsbury to design far more effective direct marketing campaigns based on customers’ actual purchasing habits.

In one campaign designed to increase the value of customers’ shopping baskets, Sainsbury’s analysed purchases and identified the product category from which each customer purchased most frequently. A coupon for that category would then be sent, along with five other coupons for areas in which it was hoping to boost sales – to encourage customers to buy other types of products. The response rate was 26%, a tremendous amount in retail.

The data warehouse will bring the benefit of removing possible duplication of files and reducing storage requirements. However, the centralisation of data may make a loss more catastrophic although backup procedures will reduce the risk. The cost of such an upgrade should also be less than the benefit.

Data mining

This is the analysis of data contained within a data warehouse to unearth relationships between them.

Illustration 3 – Data mining relationships

Data mining results may include:

- Associations – when one event can be correlated to another, g. beer purchasers buy peanuts a certain percentage of the time.

- Sequences – one event leading to another event, e.g. a rug purchase followed by a purchase of matching curtains.

- Classifications – profiles of customers who make purchases can be set up.

These relationships can be used to help an organisation focus on the things that the customer enjoys and desires. Marketing can be targeted to a group of customers and the organisation will focus on the more profitable product offerings.

Networks

Most organisations connect their computers together in local area networks (LANs), enabling them to share data (e.g. via email) and to share devices such as printers. Wide area networks (WANs) are used to connect LANs together, so that computer users in one location can communicate with computer users in another location. Improvements in broadband speed and security have eased communication across sites and from home.

A network should facilitate the transfer of information between different parts of the business.

Intranet

This is a private network contained within an organisation. It allows company information and computing resources to be shared among employees.

Extranet

This is a private, secure extension of an Intranet. It allows the organisation to share information with suppliers, customers and other business partners.

Internet

This is a global system of interconnected networks carrying a vast array of information and resources.

By connecting the network to the internet (or intranet/extranet), communication with key stakeholders will be improved and it may be possible to share data with organisations which could assist in a benchmarking exercise.

However, the opening of the organisation’s network to the internet will provide additional opportunities for the spread of viruses and possibly open the network to hackers.

Illustration 4 – The internet and management information

An Internet site that allows customers to place orders on-line can provide the following useful management accounting information:

| Data | Use |

| Customer details | For delivery purposes; also to build up a record of |

| customer interests and purchases. | |

| Product details | For delivery purposes; also to build up patterns |

| accessed and | such as products that are often bought together. |

| products bought | |

| Value of products | Sales accounting and customer profiling. |

| bought | |

| Product details | Other items that the customer might be interested |

| accessed but | in. Why were they not bought? Has a rival got |

| product not | better prices? |

| bought | |

| Date of purchase | Seasonal variations; tie in with special offers and |

| advertising campaigns. | |

| Time of purchase | Some web-sites might be particularly busy at |

| certain times of the day. Why that pattern? Avoid | |

| busy times when carrying out web-site | |

| maintenance. | |

| Delivery method | Most Internet sellers give a choice of delivery costs |

| chosen | and times. Analysis of this information could help |

| the company to increase its profits. | |

The use of intranets to enhance performance

HI is a large importer of cleaning products; HI has its head office situated in the centre of the capital city. This head office supports its area branches; a branch consists of an area office and a warehouse. The branches are spread geographically throughout the country; a total of seven area branches are supported.

Currently each HI area office and warehouse supports and supplies its own dealers with the required products. When stocks become low they place a Required Stock Form (RSF) with head office. On receipt of the RSF, head office despatch the goods from their central warehouse to the appropriate area office. When the central warehouse becomes low on any particular item(s) HI will raise purchase orders and send them to one of their many international suppliers.

Typically, each area office has its own stock recording system, running on locally networked personal computer systems (PCs). RSFs are e-mailed to head office.

Required:

How would the introduction of an Intranet enhance performance within HI?

Solution:

An Intranet could provide an excellent opportunity for HI to link all the areas in a number of ways: i.e. allowing access to a central database would be a substantial improvement on the current system, where updates are faxed or e-mailed to head office. This may possibly lead to the development of an integrated database system.

An automatic stock replenishment system could be introduced for the branches, replacing RSFs. If some branches were short of specific items and other branches had ample stocks, then movement between branches may be possible. Currently head office may order goods from suppliers when the organisation has sufficient stocks internally.

Dissemination of best practice throughout the organisation can be encouraged and savings in terms of printing and distributing paper based manuals, catalogues and handbooks. All the current internal documentation can easily be maintained and distributed.

The Intranet would enable the establishment of versatile and standard methods of communication throughout the company.

The Intranet could encourage group or shared development, currently several area offices have their own IT systems working independently on very similar projects.

An Intranet could also enable automatic transfer of information and data i.e. the quarterly figures could be circulated. Monthly returns of business volumes could be calculated on an as required basis.

Information can be provided to all in a user-friendly format.

Enterprise resource planning system (ERPS)

An ERPS is an example of a unified database of corporate information. Rather than data existing in isolation in different parts of the business, it integrates the data from many aspects of operations (for example, manufacturing, inventory, distribution, invoicing and accounting) and support functions (such as human resource management and marketing) into one single system.

Benefits to the organisation include:

- identification and planning of the use of resources across the organisation to ensure customers’ needs are fulfilled

- the free flow of information between all functions and improved communication between departments

- aids the management decision making process due to decision support features

- can be extended to incorporate supply chain management (SCM) and customer relationship management (CRM) software, thus helping to manage connections outside the organisation.

Software companies like SAP and Oracle have specialised in the provision of ERPS across many different industries.

Test your understanding 7

Required:

Explain how the introduction of an ERPS could impact on the role of management accountants.

Radio frequency identification (RFID)

Organisations can use small radio receivers to tag items and hence to keep track of their assets. It can be used for a variety of purposes, for example:

- to track inventory to retail stores

- to tag livestock on farms

- to track the location of doctors in a hospital.

Illustration 5 – RFID

Many clothing retailers began the phased rollout of item-level radio frequency identification (RFID) tags in 2007 following extensive testing of the technology. Stock accuracy has improved and stores and customers have commented on the more consistent availability of sizes in the pilot departments.

The tags allow staff to carry out stocktaking 20 times faster than bar code scanners by passing an RFID reader over goods. At the end of each day, stock on the shop floor will be scanned and the data collected will be compared with information in a central database containing each store’s stock profile, to determine what products need to be replaced. This has led to improved sales through greater product availability.

The introduction of RFID can bring about a number of benefits:

- Information on the location and quantity of items can be provided in real time meaning that less time is spent looking for items.

- This information should be more accurate since it will be less reliant on physical checks.

- Performance reporting should improve due to the provision of real time information.

- Control should be easier. This is firstly due to the provision of real time information and, secondly, since the location and quantity of items will be known, the risk of theft and obsolescence will be reduced.

The benefits must outweigh the costs. Costs will include the cost of hardware, software, ongoing running and maintenance costs and training costs.

Test your understanding 8

Required:

Discuss the impact of recent IT developments on management accounting and on business performance.

7 Big Data

7.1 What is Big Data?

There are several definitions of Big Data. The most common refer to:

Extremely large collections of data that may be analysed to reveal patterns, trends and associations.

Data collections so large that conventional methods of storing and processing that data will not work.

Big Data is a big buzzword at the moment and some say that it will be even bigger than the Internet. The ability to harness these vast amounts of data will transform our ability to understand the world and will lead to huge advances, for example, in understanding customer behaviour, foiling terrorist attacks, preventing diseases and pinpointing marketing efforts.

Illustration 6 – The use of Big Data by supermarkets

A supermarket is able to take data from a your past buying patterns, its internal inventory information, your mobile phone location data, social media as well as weather information to send you a voucher for barbeque food; but only if you own a barbeque, the weather is nice, you are within 3 miles of one of their stores and the barbeque food is in stock.

7.2 The 3Vs

Big Data is characterised by the 3Vs:

- Volume: organisations now hold huge volumes of data. For example:

– A supermarket will have a data store of all purchases made, when and where they were made, how they were paid for and the use of coupons via loyalty cards swiped at the checkout.

– An online retailer will have a data store of every product looked at and bought and every page visited.

– Mobile phone providers will have a data store of texts, voice mails, calls made, browsing habits and location.

– Social media companies, such as Facebook, will have a data store of all the postings an individual makes (and where they were made), photos posted and contacts.

- Variety: Big Data can include much more than simply financial information and can include other organisational data which is operational in nature as well as other internal and external information. This data can be both structured and unstructured in nature:

– Structured data – for example, a bank will hold a record of all receipts and payments (date, amount and source) for a customer.

– Unstructured data – can make up 80% of business data but is more difficult to store and analyse.

- Velocity: The data must be turned into useful information quickly enough to be of use in decision making and performance management (in real time if possible). The sheer volume and variety of data makes this task difficult and sophisticated methods are required to process the huge volumes of non-uniform data quickly.

A fourth ‘v’, veracity is sometimes included, i.e. is the data accurate enough to be relied upon?

7.3 Processing Big Data

The ability to manage Big Data successfully will drive innovation (and potentially competitive advantage) to reduce the time taken to answer key business questions and hence make decisions.

The processing of Big Data is known as Big Data analytics. For example, Google Analytics tracks many features of website traffic.

Hadoop software allows the processing of large data sets by utilising multiple servers simultaneously.

7.4 Big Data and performance management

Big Data is relevant to performance management in a number of ways, such as:

- It can help the organisation to understand its customers’ needs and preferences which can then be used to improve marketing and sales.

- It can improve forecasting, for example of future customer spending or of machine replacement cycles, so that more appropriate decisions can be made.

- It can help the organisation to automate business processes resulting in improved efficiency.

- It can help to provide more detailed, relevant and up to date performance measurement.

7.5 Examples of how Big Data is used

- Consumer facing organisations monitor social media activity to gain insight into customer behaviour and preferences. This source can also be used to identify and engage brand advocates and detractors, and assess responsiveness to advertising campaigns and promotions.

- Sports teams can use data of past fixtures to track tactics, player formations, injuries and results to inform future team strategies.

- Manufacturing companies can monitor data from their equipment to determine usage and wear. This allows them to predict the optimal replacement cycle.

- Financial Services organisations can use data on customer activity to carefully segment their customer base and therefore accurately target individuals with relevant offers.

- Politicians are using social media analytics to establish where they have to campaign the hardest to win the next election.

- Humanitarian agencies, such as the United Nations, use phone data to understand population movements during relief operations and outbreaks of disease, meaning they can allocate resources more efficiently and identify areas at risk of new disease outbreaks.

More examples of Big Data in the real world

UPS’s delivery vehicles are equipped with sensors which monitor data on speed, direction, braking performance and other mechanical aspects of the vehicle. This information is then used to optimise maintenance schedules and improve efficiency of delivery routes saving time, money and reducing wastage.

Data from the vehicles is combined with customer data, GPS information and data concerning the normal behaviour of delivery drivers. Using this data to optimise vehicle performance and routes has resulted in several significant improvements:

- Over 15 million minutes of idling time were eliminated in one year. This saved 103,000 gallons of fuel.

- During the same year 1.7 million miles of driving was eliminated, saving 183,000 gallons of fuel.

It is widely reported that Walmart (Asda) tracks data on over 60% of adults in the US. Data gathered includes online and in store purchasing pattern, Twitter interactions and trends, weather reports and major events. This data, according to the company, ensures a highly personalised customer experience. Walmart detractors criticise the company’s data collection as a breach of human rights and believe the company uses the data to make judgements and conclusions on personal information such as sexual orientation, political view and even intelligence levels.

Tesco has sophisticated sensors installed on all refrigeration units to monitor the temperature at regular intervals and to send the information over the internet to a central data warehouse. The data collected is used to identify units that are operating at temperatures that are too low (resulting in energy wastage) or too high (resulting in potential stock obsolescence and a safety risk). Engineers can monitor the data remotely and can then visit the store to rectify any problem that is identified. Previously, store managers may have overlooked a problem or only identified a problem once it had escalated into something more serious.

Netflix has over 100 million users worldwide. The company uses information gathered from analysis of viewing habits to inform decisions on which shows to invest in. Analysing past viewing figures and understanding viewer populations and the shows they are likely to watch allows the analysts to predict likely viewing figures before a show has even aired. This can help to determine if the show is a viable investment.

Test your understanding 9

MC is a mobile phone network provider, offering mobile phones and services on a range of different tariffs to customers across Europe. The company enjoyed financial success until three years ago but increasing competitive pressure has led to a recent decline in sales. There has also been an increase in the level of complaints regarding the customer service provided, and the company’s churn rate (number of customers leaving the company within a given time frame) is at an all-time high.

Required:

Discuss how Big Data could help drive the strategic direction of MC company.

7.6 Risks associated with Big Data

- The availability of skills to use Big Data systems, which is compounded by the fact that many of the systems are rapidly developing and support is not always easily and readily available. There is also an increasing need to combine data analysis skills with a deep understanding of the industry being analysed and this need is not always recognised.

- The security of data is a major concern in the majority of organisations and if the organisation lacks the resources to manage data then there is likely to be a greater risk of leaks and losses. There can be a risk to the data protection of organisations as they collect a greater range of data from increasingly personal sources (for example, Facebook).

- It is important to recognise that just because something CAN be measured, this does not necessarily mean it should be. There is a risk that valuable time is spent measuring relationships that have no organisational value.

- Incorrect data (poor veracity) may result in incorrect conclusions being

- There may be technical difficulties associated with integrating existing data warehousing and, for example, Hadoop systems.

- The cost of establishing the hardware and analytical software needed.

Student accountant article: visit the ACCA website, www.accaglobal.com, to review the articles on ‘Big Data and performance management’ and ‘Big Data’.

8 Exam focus

| Exam sitting | Area examined | Question | Number |

| number | of marks | ||

| Mar/June 2016 | RFID | 2(a) | 14 |

| Mar/June 2016 | Data warehouse, loyalty cards | 1(v) | 8 |

| Sept/Dec 2015 | ERPS | 1(iv) | 10 |

| June 2015 | ERPS | 2(a) | 10 |

| December 2013 | RFID | 3(a) | 12 |

| December 2011 | Control and development of IS | 3 | 20 |

| June 2011 | EIS | 1(c) | 5 |

| December 2010 | Impact of KPIs on system design | 1(d) | 9 |

Test your understanding 1

- External information may not be accurate.

- External information may be out of date.

- The company publishing the data may not be reputable.

- External information may not meet the exact needs of the business.

- It may be difficult to gather external information, e.g. from customers or competitors.

Test your understanding 2

Historical customer data will give information about:

- product purchases and preferences

- price sensitivity

- where customers shop

- who customers are (customer profiling).

For a business that prioritises customer satisfaction this will give important control information. Actual customer data can be compared with plans and control action can be taken as necessary, e.g. prices may be changed or the product mix may be changed.

Test your understanding 3

| Advantages | Disadvantages | |||

| | Benefit of real time data input | | Cost of real time data input. | |

| and access. | | Cost of linking the EIS to | ||

| | Improved decision making, | new, external data sources. | ||

| e.g. the EIS should allow | | Cost of implementation and | ||

| drill- down access of data to | ||||

| training. | ||||

| operational level but | ||||

| presentation of data should | | Risk that the system does | ||

| be based on the KPIs of the | not work properly or that | |||

| company. | training is inadequate. | |||

| | The EIS will link to external | | Increased security threat | |

| data sources thus reducing | since the data is only held in | |||

| the risk of ignoring issues | one place. | |||

| from the wider environment. | | Potential information | ||

| | The database will | overload, especially for | ||

| reduce/eliminate the problem | senior management. | |||

| of data redundancy since | ||||

| data is only held in one | ||||

| place. | ||||

| | Improved data integrity. Data | |||

| is only held in one place and | ||||

| therefore time and effort will | ||||

| be taken to ensure it is of | ||||

| high quality. | ||||

Test your understanding 4

A management information system can be developed to varying levels of refinement. Specifically:

- Reporting frequency– information can be collected and reported with varying levels of frequency, e.g. for example, the management accounting system of a manufacturer can report actual production costs on a daily, weekly, monthly or even annual basis.

- Reporting quantity and level of detail – information can be collected and reported at varying levels of detail e.g. in absorbing overheads into product costs one can use a single factory overhead absorption rate (OAR) or one can operate a complex ABC system. The information requirements of the latter are far more elaborate than those of the former.

- Reporting accuracy and back-up – subtle qualitative factors can be incorporated into information systems at varying levels,

e.g. information can be rigorously checked for accuracy or a more relaxed approach can be adopted.

Broadly, the more refined the MIS is, then the more expensive it is to establish and operate. The organisation has to decide if the increased benefits outweigh the increased costs.

Test your understanding 5

- A large amount of data will need to be collected initially on each activity. Therefore, the cost of buying, implementing and maintaining a system of activity-based costing will be high.

- Incorrect identification of cost pools and cost drivers would result in inaccurate information being produced by the ABC system and hence incorrect decisions by managers.

Test your understanding 6

IT systems are critical to Zara’s short lead times.

Zara needs comprehensive information in the following areas:

- which garments are selling, at what price points and in what quantities – key information will relate to both Zara stores and those of competitors

- detailed product specifications for these garments to enable design of new products

- compatibility between reporting and design software systems

- supply chain management

- order and delivery systems.

Test your understanding 7

The introduction of ERPS has the potential to have a significant impact on the work of management accountants.

- The use of ERPS causes a substantial reduction in the gathering and processing of routine information by management accountants.

- Instead of relying on management accountants to provide them with information, managers are able to access the system to obtain the information they require directly via a suitable electronic access medium.

- ERPS perform routine tasks that not so long ago were seen as an essential part of the daily routines of management accountants, for example perpetual inventory valuation. Therefore, if management accountants are not to be diminished then it is of necessity that management accountants should seek to expand their roles within their organisations.

- Management accountants may be involved in interpreting the information generated from the ERPS and to provide business support for all levels of management within an organisation.

Test your understanding 8

- IT developments, such as networks and databases, provide the opportunity for instant access to management accounting information.

- It is possible to directly access and manipulate information from both internal and external sources.

- Information is relatively cheap to collect, store and manipulate.

- Many of the modern forms of management accounting have been developed in conjunction with IT systems, e.g. it may be difficult to run a meaningful ABC system without IT support.

- Data mining techniques can be used to uncover previously unknown patterns and correlations and hence improve performance.

Test your understanding 9

Big Data management involves using sophisticated systems to gather, store and analyse large volumes of data in a variety of structured and unstructured formats. Companies are collecting increasing volumes of data through everyday transactions and marketing activity. If managed effectively this can lead to many business benefits although there are risks involved.

A company like MC will already collect a relatively large amount of data regarding its customers, their transactions and call history. It is likely that a significant proportion of their customers are also fairly digitally engaged and therefore data can be gathered regarding preferences and complaints from social media networks. This will be particularly useful to MC as they have seen an increase in complaints and have a high churn rate so engaging with customers will be highly beneficial.

Recent competitive pressure has led to a decline in sales and so MC need to consider the strategic direction which is most appropriate for them to improve performance.

Analysing the large amounts of data available to them will inform decisions on areas such as:

- The type of handsets currently most in demand and therefore the prices required when bundling with tariffs; Main areas of complaint and therefore the areas of weakness which need to be resolved

- Which types of communication are most popular (e.g. data, call minutes, text messages) to ensure the tariffs have the right combinations

- Usage statistics for ‘pay as you go’ customers, to drive the most appropriate offers and marketing activity

- Most popular competitor offerings with reasons.