LESSON 1

INTRODUCTION TO FINANCIAL SYSTEMS

Objectives

By the end of the lesson, learners should be able to:

Define financial system

Explain the role of financial systems

Explain the components of a financial system

The Financial System

A financial system no matter how rudimentary is a complex system. It is complex in its operation such that neither the system itself nor its operation can be measured accurately. Because of this complexity a simple definition cannot adequately capture

what a financial system is. A financial system comprises financial institutions, financial markets, financial instruments, rules, conventions, and norms that facilitate the flow of funds and other financial services within and outside the national economy.

The financial system can be described as a whole system of all institutions, individuals, markets and regulatory authorities that exist and interact in a given economy. The institutions, government and individuals form the participants in various markets; money markets (including foreign exchange) and capital markets (including security) markets. The participant buy (borrow) and sell (lend) money to different parties at a price (interest or dividend) within the market, which is determined by the forces of demand and supply.

In a broader aspect a financial system can also be defined as a system that allows the transfer of money between savers (and investors) and borrowers operating on a global, regional or firm specific level. According to Gurusam, it is a set of complex and closely interconnected financial institutions, markets, instruments, services, practices, and transactions.

Financial systems are crucial to the allocation of resources in a modern economy. They channel household savings to the corporate sector and allocate investment funds among firms; they allow inter-temporal smoothing of consumption by households and

expenditures by firms; and they enable households and firms to share risks. Since these functions take place in a market oriented environment, there is a need for an independent party to enforce rules and contracts and this is the regulator. The main regulatory authorities of the financial institutions that constitute the financial system of a given economy are the Central Bank and Capital Market Authority.

THE ROLE OF FINANCIAL SYSTEM IN THE ECONOMY

The financial sector provides six major functions that are crucial for the survival and efficient operation of any given economy. These functions are outlined below:

1. Providing payment services.

It is inconvenient, inefficient, and risky to carry around enough cash to pay for purchased goods and services. Financial institutions provide an efficient alternative. The most obvious examples are personal and commercial checking and check-clearing and credit and debit card services; each are growing in importance, in the modern sectors at least, of even low-income countries.

2. Matching savers and investors.

Although many people save, such as for retirement, and many have investment projects, such as building a factory or expanding the inventory carried by a family micro enterprise, it would be only by the wildest of coincidences that each investor saved exactly as much as needed to finance a given project. Therefore, it is important that savers and investors somehow meet and agree on terms for loans or other forms of finance. This can occur without financial institutions; even in highly developed markets, many new entrepreneurs obtain a significant fraction of their initial funds from family and friends. However, the presence of banks, and later venture capitalists or stock markets, can greatly facilitate matching in an efficient manner. Small savers simply deposit their savings and let the bank decide where to invest them.

3. Generating and distributing information .

One of the most important functions of the financial system is to generate and distribute information. Stock and bond prices in the daily newspapers of developing countries are a familiar example; these prices represent the average judgment of thousands, if not

millions, of investors, based on the information they have available about these and all other investments. Banks also collect information about the firms that borrow from them; the resulting information is one of the most important components of the capital

of a bank although it is often unrecognized as such. In these regards, it has been said that financial markets represent the brain of the economic system.

4. Allocating credit efficiently .

Channeling investment funds to uses yielding the highest rate of return allows increases in specialization and the division of labor, which have been recognized since the time of Adam Smith as a key to the wealth of nations.

5. Pricing, pooling, and trading risks .

Insurance markets provide protection against risk, but so does the diversification possible in stock markets or in banks’ loan syndications.

6. Increasing asset liquidity .

Some investments are very long-lived; in some cases – a hydroelectric plant, for example – such investments may last a century or more. Sooner or later, investors in such plants are likely to want to sell them. In some cases, it can be quite difficult to find a buyer at

the time one wishes to sell – at retirement, for instance. Financial development increases liquidity by making it easier to sell, for example, on the stock market or to a syndicate of banks or insurance companies.

7. Financial systems and economic growth:

Both technological and financial innovations have driven modern economic growth. Both were necessary conditions for the Industrial Revolution as steam and water power required large investments facilitated by innovations in banking, finance, and insurance.

Both are necessary for developing countries as they continue their struggle for economic development. But the effective functioning of the financial system requires, in turn, the precondition of macroeconomic stability.

The Five Parts of the Financial System

1.Money : A Good which is used as a means of payment for exchanging goods. This has not always been the case, we once used gold and silver coins as a means of paper.

2. Financial Instruments : A written legal obligations of one party to transfer something of value to another party at some future date under certain conditions. These obligations usually transfer resources from savers to investors. Examples: Stocks, bonds,

insurance policies.

3. Financial Markets : Markets where financial instruments are traded. Examples: New York Stock Exchange, Chicago Board of Trade and Nairobi Stock exchange.

4. Financial Institutions : These entities prov ide services and allow agents access to financial instruments and markets. Examples: Banks, securities firms and insurance companies.

5. Regulators : Government entity which monitors the state of the economy and conducts monetary policy. Example: central Bank of Kenya.

LESSON 2

Instruments of capital markets

An Overview of Financial Markets

A Financial Market is an institution or arrangement that facilitates the exchange of financial assets. They are mechanisms in our society for converting public savings into investments such as buildings, machinery, infrastructure and inventories of goods and raw materials. This enables the economy to grow, new jobs to be created and living standards to rise. Financial markets therefore perform the essential economic function of channeling funds from economic units which have surplus funds (net savers) to economic units with a net deficit of funds (investors).

Classification of Financial Markets

There are several basic methods of classifying financial markets as follows:

1. A classification of the markets based on the type of instrument or service as follows:

Debt Markets

Equity Markets

Financial services Markets

2. A broad classification that distinguishes between

Primary &

Secondary Markets

3. A classification of markets based on the term to maturity and liquidity of the instrument. This method categorizes financial markets into

Money Markets &

Capital Markets

4. A classification of markets according to when the financial instruments being traded will be delivered. This classification categorizes markets into:

Spot markets

Futures or forward markets

Option markets

5. A classification of markets into open and negotiated markets.

Auction market

Bourse

Over-the-counter market

6.Financial markets can also be classified in terms of the extent of financial intermediation involved in the sale of the financial instruments as follows:

Direct finance markets

Semi-direct finance markets

Indirect finance markets

1. Debt Markets

This is the most familiar type of market. Here, the lenders provide funds to borrowers for some specific period of time. In return for the funds, the borrower agrees to pay the lender the principal loan plus some specified amount of interest. Debt markets are used by individuals to finance purchases such as houses, cars, home appliances, Corporate borrowers to finance working capital and new equipment and the central and local governments to finance various public expenditures. Debt instruments include bonds, mortgages and the various types of bank loans. These are contractual agreements by the borrower to pay the holder of the instrument fixed amounts of money at regular intervals until the maturity date, when the final payment is made. The regular payments contain elements of both principal and interest payments.

2.Equity Markets

This is the market for raising funds by issuing equities such as common stock. Equities are claims to share in the net income and the assets of a business. Equities usually make periodic payments in form of dividends to their holders. Holders are residual claimants in that the corporate must pay all its debt holders before it pays its equity holders. Equities usually have no maturity dates.

3. Service Markets

These are markets where individuals and corporate can purchase services that enhance the workings of the debt and equity markets. Banks for example, provide depositors many serv ices in addition to paying them interest on their deposits. These include money transmission services, safe deposit facilities, payment services e.t.c. Thus, in addition to participating in the debt market, by issuing loans banks also provide financial services that provide ‘convenience’ to consumers in various ways.

Stock brokers also participate in financial markets by competing for the right to help individuals and corporate bodies buy and sell financial assets such as stocks and bonds. As intermediaries, brokers receive a fee for performing the service of matching buyers and sellers. Dealers on the other hand, buy and sell securities on their portfolio, not just matching buyers and sellers. Another important function of the financial services market is providing consumers, businesses, and governments with financial risk management services, that is protection against life, health, property and income risks through sale of various insurance policies.

4. Primary Markets

The primary market is used for trading of new securities that have never before been issued. Its primary function is raising capital to support new investments or corporate expansions. The best example of a primary market is the market for corporate Initial Purchase offers (IPOs) which are used to sell company shares to the public for the first time. Other primary markets include market for Treasury bills and Treasury bonds.

5. Secondary Markets

These are markets that deal in securities which were issued previously. The chief function of a secondary market is to provide liquidity to investors – that is, provide an avenue for converting financial instruments into ready cash. Examples of secondary markets are markets for stocks and shares and that of long-term bonds.

6. Money Markets

Money markets are financial markets that are used for the trading of short-term debt instruments, generally those with original maturity of less than one year. The money market is the place where individuals and institutions with temporary surpluses of

funds meet the needs of borrowers who have temporary fund shortages. Thus, the money markets enable economic units to manage their liquidity positions. For example, a security or loan with a maturity period of less than one year is considered a money market instrument. One of the principle functions of the money market is to finance the working capital needs of corporations and to provide governments with short-term funds in lieu of tax collections. The money market also supplies funds for speculative buying of securities and commodities.

7. Capital Markets

The capital market is designed to finance long-term investments by businesses, governments and households. Capital market instruments are mainly longer term debt securities (generally those with original maturities of more than one year) and equities. Examples include bonds and shares traded on the stock exchange.

8. Spot Markets

A spot market is one in which securities or financial services are traded for immediate delivery (usually within one or two business days. Advanced stock exchange markets for equities and spot foreign exchange markets operate in this manner.

9.0 Futures or Forward markets

A futures or forward market trades contracts calling for future delivery of financial instruments. The purpose of such contracts is to reduce risk by agreeing on a price today rather than waiting to buy spot in future when the price of the asset being purchased might have risen.

10. Option Markets

Option markets make it possible to trade in options, to buy a selected range of stocks and bonds. Options are agreements (contracts) that give an investor the right (but not the obligation) to either buy from or sell designated securities to the writer of the option at a guaranteed price at any time during the life of the contract. Options, just like futures are a risk management mechanism. They give investors the chance of limiting losses while preserving the opportunity to make substantial profits.

11. Open versus Negotiated Markets

Open markets refer to the situation where financial instruments e.g corporate bonds are sold in the open market to the highest bidder and bought and sold any number of times before they mature and are paid off. On the other hand, the negotiated market refer to a situation whereby the instruments are sold to one or a few buyers under private contract. Bank Loans are a type of assets that can be said to be traded under negotiated market conditions.

12. Direct, Semi Direct and Indirect Finance

Direct Finance

Direct finance refers to the situation in which borrowers borrow money directly from lenders in return for financial assets. This means that there are no financial intermediaries involved in the transaction. The financial assets issued in these situations are usually primary securities like stocks, bonds, notes, e.t.c which are issued directly to the lender. Examples include company shares sold through private placing and commercial paper issued by large corporate bodies . Direct finance instruments are also referred to as instruments of financial disintermediation due to the fact that no intermediaries are involved in the transactions. Dir ect finance is the

simplest method of carrying out financial transactions. It however has a number of serious limitations as follows

- Both the borrower and lender must be desirous of exchanging the same amount of funds at the same time

- The borrower must be willing to accept the borrower’s IOU which may be risky or slow to mature

- There must be a coincidence of wants between surplus and deficit – budget units in term of amount and form of a loan; without this fundamental coincidence, direct finance breaks down.

- Both the lender and the borrower must frequently incur substantial information costs simply to find each other.

Semi-direct Finance

This is the kin to the situation that prevailed in the early history of most financial systems. Here, some individuals and business firms become securities brokers and dealers whose principal function is to bring surplus and deficit budget-units together, thereby reducing information costs. There is a difference between a broker and a dealer in securities. A broker is merely an individual or financial institution who provides information concerning possible purchases and sales of securities. Either a buyer or a seller can contact a broker whose job is simply to bring buyers and sellers together. A dealer on the other hand although also an intermediary between buyers and sellers, actually acquires the seller’s securities in the hope of marketing them at a later time at a favorable price. Dealers take a ‘position of risk’ when they buy the securities for their own portfolio or when they ‘underwrite’ a security issue by undertaking to buy any securities that might not be taken up by buyers in a primary sale.

Dealers and brokers assist in reducing costs associated with information search. They also facilitate the development of a secondary market for the securities. Despite these advantages semi-direct finance has limitations. The ultimate lender still winds up holding the borrowers’ securities and therefore, the lender must be willing to accept the risk and maturity characteristics of the borrower’s IOU. There also must be a fundamental coincidence of wants and needs between surplus and deficit budget units for semi-direct financial transactions to take place.

Indirect Finance

This is a financing situation that is carried out in with the help of financial intermediaries, a situation that attempts to reduce the limitations of direct and indirect finance. Financial intermediaries in financial markets include commercial banks, insurance companies, credit unions, finance companies, pension funds, microfinance institutions, e.t.c. Financial intermediaries serve both ultimate borrowers and lenders but in a much more complete way than brokers and dealers do. Financial intermediaries issue securities of their own- secondary securities – to ultimate lenders and at the same time accept IOUs from borrowers – primary securities.

Secondary securities include familiar facilities like checking and savings accounts, life insurance policies, and shares in a mutual fund. Common characteristics of these instruments include

- They generally carry low risk of default

- They can be acquired in small denominations, affordable by savers of limited means

- For most part, secondary securities are liquid and can therefore be converted quickly into cash with little risk of significant loss.

Financial intermediaries accept primary securities from those who need credit and, in doing so, take on financial assets that many savers, especially those with limited funds and limited knowledge of the market would find unacceptable. One of the benefits of the development of efficient financial intermediation (indirect finance) has been to smooth out consumption spending by households and investment spending by businesses over time, despite variations in income. Intermediation makes savings and borrowing easier and safer. Financial intermediation also permits a given amount of saving in the economy to finance a greater amount of investment than

would have occurred without intermediation.

LESSON 3

FINANCIAL INSTRUMENTS

Objectives: learners are expected to have a good understanding of the following:

Financial instruments and their role in the economy

Properties of financial assets

Money market and capital market instruments

Eurocurrency instruments and government agency securities

A financial instrument is defined as, a claim against the income or wealth of a business firm, house hold or unit of government, normally represented by a certificate, receipt or other legal document, and which is usually created by the lending of money. Financial Assets are by therefore nature intangible assets e.g

- Treasury Bills

- Bonds

- Shares

Role of financial assets

1. Transfer funds from surplus units to deficit units to invest in intangible assets.

2. Transfer funds in such a way as to redistribute the unavoidable risk associated with the cash flow generated by tangible assets among those seeking and those providing the funds.

Properties of financial assets

These properties influence the attractiveness to investors:

MONEYNESS : Some financial assets are used as a medium of exchange- these assets are called money. Other assets are near money/quasi-money for example Treasury bills. Therefore moneyness is a desirable property for investors.

DIVISIBILITY & DENOMINATION : Divisibility relates to the minimum size at which a financial asset can be liquidated and exchanged for money. The smaller the size the more the financial asset is divisible.

REVERSIBILITY : Also known as round-trip cost refers to the cost of investing in a financial asset and then getting out of it and back into cash again e.g Bank deposit. A low round-trip cost is clearly a desirable property of a financial asset, and as a result thickness is a valuable property. Thickness of the market is essentially the prevailing rate at which buying and selling orders reach the

market maker. A thin market is one which has few trades on a regular and continuing basis.

TERM TO MATURITY : The term to maturity is the length of interval until the date when the instrument is scheduled to make its final payment or the owner is entitled to demand liquidation. However, it should be recognized that even a financial asset with a stated maturity, may terminate before its stated maturity. This may occur for several reasons including bankruptcy or because of provisions

entitling the debtor to repay in advance or the investor may have the privilege of asking for early repayment.

LIQUIDITY: Liquidity is determined by contractual arrangements. Deposits at a bank are perfectly liquid because the bank has a contractual obligation to convert them at par on demand. However, financial contracts representing a claim on private pension fund may be regarded as totally illiquid because these can be cashed only on retirement. Liquidity may depend not only on the financial

asset but also on the quantity one wishes to sell or buy. A small quantity may be quite liquid while one may run into illiquidity problems with large lots.

CONVERTIBILITY : Some financial assets are convertible into other financial assets. In some cases, the conversion takes place within one class of financial assets, as when a bond is converted into another bond. In some cases the conversion spans classes e.g a Corporate convertible bond may be changed into equity. Normally the timing , costs and conditions are clearly spelled out in the

legal descriptions of the convertible security at the time it is issued.

The following are some of the most common instruments in use today:

Money Market Instruments

They are short-term dated securities. Because of their short terms to maturity, they undergo the least price fluctuations and are therefore the least risky instruments. The following are examples of money market instruments;

1.Treasury Bills:

- These are shot-term debt instruments issued by the government

- They are issued in 3,-6,- and 12-month maturities to finance government activities

- They pay a set amount at maturity and have no interest payments

- Interest is covered by the fact that they are initially sold at a discount, that is, an amount lower than the amount they are redeemed at on maturity

- They are the most liquid of all the money market securities because they are the most actively traded

- Interest rates on T-bills are usually the anchor for all other money market interest rates

- They re also the safest among the money market instruments because the chances of default are minimal (the government can always raise taxes or issue currency to pay off its debts)

- T-bills are popular due to their zero default risk, ready marketability, and high liquidity.

Types of Treasury Bills

There are several types of bills that are issued by governments:

Regular- series bills: –

- These are issued routinely every week or month in competitive auctions

- They have original maturities of three months, six months and one year.

- New three and six month bills are auctioned weekly,; one year bills are normally sold once each month

Irregular- series bills

- These are issued only when the Treasury has a special cash need

- They can be strip bills or cash management bills

- Strip bills- these comprise of a package offering of bills requiring to bid for an entire series of different bill maturities.

- Investors who bid successively must accept bills at their bid price each week for several weeks running

Cash Management bills

Consist simply of reopened issues of bills that were sold in prior weeks

The reopening of a bill issue normally occurs when there is an unusual or unexpected Treasury need for cash.

How Treasury Bills are sold

- T-bills are sold using the auction method.

- A new regular bill is announced weekly by the Treasury on Tuesday each week, with bids from investors being due the following Monday by 1pm.

- Interested investors fill out a form tendering an offer to the Treasury for a specific bill issue at a specific price.

- The bid forms are usually submitted through commercial banks or it can be taken to Central bank

- The Treasury entertains both competitive and non-competitive tenders for bills

- Competitive tenders are typically submitted by large investors such as banks and security dealers who several million shillings worth at one time.

- Non-competitive tenders usually come from small investors who agree to accept the average price set in the weekly or monthly bill auction

- Non competitive bidders must pay the full par –value price of the bill at the time the tender is made and on the issue date receives the refund representing the difference between the amount paid in by the investor and the actual auction price.

- Generally, the Treasury fills all non-competitive tenders for bills.

- For the competitive bills, the highest bidder receives bills and those who bid lower also receive theirs until all available securities have been allocated.

- The lowest price at which at least some bills are awarded is called the stop-out price.

2.Negotiable Bank Certificates of Deposit:

A certificate of deposit (CD) is

- a debt instrument sold by a bank to depositors

- it pays annual interest of a given amount and at maturity pays back the original purchase price

- The interest rate on a large CD is set by negotiation between the issuing institution and its customer and it generally reflects the prevailing market conditions.

- Negotiable CDs may be registered on the books of the issuing depository institution or issued in bearer form to the purchasing

investor. - Bearer CDs are easier to trade on secondary markets

- Interest rates in the CD market are computed as a yield to maturity but are quoted on a 360 day basis, except in the secondary trading market where the bank discount rate is used as a measure of CD yields.

3.Commercial paper:

- A commercial paper is a short-term debt instrument issued by large banks and well known corporations.

- it promises to pay back higher specified amount at a designated time in the immediate future – say, 30days

- Issuers of commercial paper sell the instrument directly to other institutions as a way of rising funds for their immediate needs instead of borrowing from banks

- Commercial paper is a form of direct finance and therefore an instrument of financial disintermediation

- Issuance of commercial paper is a cheaper way of raising funds for a firm than borrowing from a bank

- A firm must be large and creditworthy enough for lenders to accept its paper

- Funds raised from paper issue are mainly used for current transactions e.g. to purchase inventories, pay taxes, meet pay-rolls, e.t.c rather than capital transactions( long-term investments)

- There is however a growing trend of corporations’ issuance of paper to raise bridging finance for long-term projects such as buildings, manufacturing assembly lines, e.t.c.

- Commercial paper is mainly traded in the primary market

- Opportunities for resale in the secondary market are limited, although some dealers redeem the notes they sell in advance of maturity and others trade paper issued by large finance companies and bank holding companies

- Because of the limited resale possibilities, inv estors are usually careful to purchase those paper issues whose maturity matches their planned holding periods.

Types of commercial paper:

There are two types:

Direct paper – issued directly to the investor, sold by large finance companies and bank holding companies that deal directly with the investor rather than using a securities dealer as an intermediary. Directly placed paper must be sold in large volume to cover the substantial cost of distr ibution ad marketing.

Dealer paper – also known as industrial paper dealer is usually issued by security dealers on behalf of their corporate customers.

1) It is mainly issued by non-financial companies as well as smaller bank holding companies and finance companies who borrow less frequently than firms issuing direct paper.

2) The issuing company may sell the paper directly to the dealer, who buys less discount and commissions and then attempts to resell it at the highest possible price in the market.

3) Alternatively, the issuing company may carry all the risk, with the dealer only agreeing to sell the issue at the best price available less commission, referred to as a best effort basis.

4) Another method that may be used is the open-rate method in which the borrowing company receives some money in advance but the balance depends on how well the issue sells in the open market.

Maturity of Commercial Paper:

- Maturities of commercial paper ranges from three days (‘weekend paper’) to nine months

- Most commercial paper notes carry an original maturity of 60 days or less, with an average maturity ranging from 20 to 45 days

- Yields of commercial paper are calculated by the bank discount method

- Just like with treasury bills, most commercial paper is issued at par, where by the investor yield is arises from the price appreciation of the security between its purchase date and maturity date.

Advantages of Issuing Commercial paper

- It is a cheaper method of raising funds for a company because the interest rate is generally lower than bank loans

- Interest rates are usually more flexible than for bank loans

- It is a quicker method of raising funds either through a dealer or direct finance. Dealers usually keep in close contact with the market and generally know where funds may be found quickly

- Generally large amounts of funds may be borrowed more conveniently than through say, bank loans mainly because there are legal restrictions concerning the amount of money that a ban can lend to a single company.

- The ability to issue commercial paper gives a company considerable leverage when negotiating with banks.

Possible disadvantages of issuing commercial paper

- Risk of a company that frequently issues commercial paper alienating itself from banks whose loans may be required in case of an emergency

- Commercial paper cannot be paid off at the issuer’s discretion. It generally remains outstanding until maturity unlike bank loans which may permit early retirement without penalty.

5. Banker’s Acceptances

These are money market instruments that are created in the course of carrying out international trade and have been in use for hundreds of years.

A banker’s acceptance is a time draft dr awn on a bank by an exporter or importer to pay for merchandise or to buy foreign currencies. It is usually guaranteed at a fee by the bank that stamps it “accepted” on its face and endorses the instrument.

By “accepting” instruments, the issuing banks unconditionally guarantee to pay the face value of the acceptances at maturity, thereby shielding exporters and investors in international markets from default risk.

The firm that is issuing the instrument is required to deposit the required funds into its account to cover the draft, otherwise the accepting bank is obligated to honour the instrument whether it is covered or not.

A banker’s acceptance is as good as the bank guaranteeing its payment

Acceptances carry maturities ranging from 30 to 270 days (with 90 days being the most common) and are considered prime – quality money market instruments.

They are actively traded among financial institutions, industrial corporations and securities dealers as a high- quality investment and source of ready cash.

Importance of Acceptances

- Acceptances are used in international trade because most exporters are uncertain of the credit standing of importers to whom they ship goods.

- Exporters may also be uncertain about business conditions or political developments in foreign countries.

- Nations experiencing instability in form of civil wars and terrorist activities have serious problems attracting financing for imports of goods and services because of the country risk involved if lines of credit were extended within their territories.

- Exporters therefore rely on acceptance financing by a foreign or domestic bank.

- A bank acceptance is thus an instrument designed to shift the risk of international trade to a third party willing to take on that risk at cost.

- Banks are willing to take on such risk because they are specialists in assessing credit risk and spread that risk over many different loans.

The Operation of a Banker’s Acceptance

- Trade acceptances usually begin when an importer goes to a bank to secure a line of credit to pay for shipment of goods from abroad.

- Once the line is approved, the bank issues a letter of credit (LC) in favour of the foreign exporter. The LC authorises the exporter to draw a time draft for a specified amount against the issuing bank, on condition that appropriate shipping documents giving the issuing bank temporary title to the exported goods.

- The fact that the LC authorises the drawing of a time draft and not a sight draft means that the exporter must wait until maturity to be paid. The time draft may also be payable in the home currency of the issuing bank, a currency that might not be needed by the exporter.

- Typically then, the exporter discounts the time draft in advance of maturity through his/her principle bank

- The exporter then receives timely payment in local currency to avoid exchange rate fluctuations.

- The bank that has now acquired the draft from the exporter forwards it plus the shipping documents) to the bank issuing the original letter of credit.

- The issuing bank checks to see that the draft and any accompanying documents are correctly drawn and then stamps “accepted” on its face. This action results in the creation of an acceptance and

the acknowledgement by the issuing bank of absolute liability on the document which must be paid on maturity

Frequently, the issuing bank discounts the new acceptance for the foreign bank that sent it and credits its correspondent account with the proceeds. The acceptance may then be held by the issuing bank as an asset or sold to a dealer.

Meanwhile shipping documents for any goods that accompanied the acceptance are handed over to the importer against a trust receipt, permitting the importer to pick up and market the goods.

However, under the terms of the letter of credit, the importer must deposit the proceeds of from the sale of the goods at the issuing bank in sufficient time to pay for the acceptance.

Note :A discount fee is charged off the face value of an acceptance whenever it is discounted in advance of maturity. The accepting bank earns a commission which may be paid either by the exporter or importer, in addition to the fees associated with the original line of credit.

6.Repurchase Agreements

- A repurchase agreement (Repo/RP) is a short-term loan where by the borrower sells marketable securities such as Treasury bonds to the lender but undertakes to buy them back at a later date at a fixed price plus interest or at a price which is

slightly higher than the one they were sold to the lender. - Thus, Repos are in effect temporary extensions of credit collateralized by marketable securities.

- Some Repos are for a specified period of time (term) while others carry no express maturity dates but may be terminated by either party on short notice. These are known as continuing contracts

- The main borrowers in the repos markets are dealers and banks

- Lenders in the market include large banks, corporations, state and local governments, insurance companies, and foreign financial institutions, who find the market a convenient, relatively low- risk way to invest temporary cash surpluses that may be retrieved quickly when needed.

- Normally the securities that form collateral for a repo are supposed to be placed in a custodial account in a bank. When the loan is repaid, the borrower’s repo liability is cancelled and the securities returned to them.

- Traditional overnight lending makes up the bulk repos but there is a growing trend of repos carrying longer maturities of between one and three months. These are known as ter m agreements.

- Some repos have built in flexibility to benefit both borrower and lender. An example would be a repo which permits the seller of securities (borrower) to repurchase from the lender securities that are similar to but not necessarily the same as the securities originally sold. These are called flex repos

- The interest rate on repos is the return that a dealer must pay a lender for the temporary use of money and is closely related to other money market interest rates.

- Usually, the securities pledged behind a repo are valued at their current market price plus accrued interest (on coupon – bearing securities) less a small “haircut ” (discount) to reduce the lender’s exposure to market risk. The longer the term and the riskier and less liquid the pledged securities, the larger the “haircut” in order to protect the lender in case security prices fall,

- Periodically, the repos are “marked to market”, and if the price of the pledged securities has dropped, the borrower may have to pledge additional collateral.

Sources of Dealer Income

- Security dealers usually act as market makers for T-bills and other financial instruments. They take substantial risks to make a market for these instruments and for this reason they try to deal with only the high quality instrument available in the financial market place.

- However, even the finest instruments can experience rapid declines if interest rates rise. Despite this, established dealership houses are obliged to stand ready at all times to buy and sell on customer demand, regardless the condition of the market.

- Dealers therefore, take a position of risk when they ct as principals in the buying and selling of securities, unlike brokers who merely bring buyers and sellers together.

- Dealers buy specified types of securities at n announced bid price and sell them at an announced asked price. This is what is known as making a market in a particular financial instrument.

- Dealers hope to make a profit from market making activities in part from the positive spread between bid and asked prices.

- The spread varies wit market activity and the outlook for interest rates but is usually narrow on bills and wider on more volatile notes and bonds.

- Spreads also range higher on long-term securities not actively traded due to greater risk and cost.

- Dealers’ holdings of securities ar e usually financed by borrowing, which makes their portfolio positions extremely sensitive to fluctuations I interest rates. For this reason dealers keep shifting from long positions to short positions, depending on the outlook for interest rates.

- Along position refers o the situation where dealers have purchased securities outright, taken title to them, holding them in their portfolios as an investment or until the customer comes along. Long positions typically increase in periods of falling interest rates .

- A short position refers to the situation where dealers have sold securities they do not own presently, to make a future delivery to a customer. In so doing, they hope they hope that prices of those securities will fall (and interest rates rise) before they must acquire the securities and make the delivery.

- If interest rates fall (and security prices rise), the dealer will experience capital gains on a long position but losses on a short position.

- If interest rates rise (resulting in a drop in security prices), the dealer’s long position will experience capital losses and the short position will post a gain.

- In periods when interest rates are expected to rise, dealers typically reduce their long positions and go short. On the other hand, expectations of falling rates lead dealers to increase their long positions and avoid short sales.

- By correctly anticipating rate mov ements, the dealer is able to earn substantial position profits.

- Dealers also receiv e carry income, which is the difference between interest earned on securities they hold and their cost of borrowing funds.

- Generally, dealers earn higher rates of return on the securities they hold than the interest they for loans, but this is not always the case.

- To help reduce exposure to risk, security dealers also diversify their revenue generating services, e.g. by trading in foreign currencies, commodities such as oil, security options, futures contracts and SWAP contracts.

- Some offer cash management services in which they hold funds of customers and invest them in securities, earning cash management fees from those same customers.

- Some act as financial intermediaries, simultaneously borrowing and lending money through a technique known as matched book, in which funds are borrowed through low-cost short-term RPs and then are loaned out through longer-term, higher yielding RPs.

- The yield spread between the matched RPs gives the dealer a net profit, unless the yield curve suddenly changes and the dealer is forced to borrow short-term money at significantly higher interest rates.

- Dealers are increasingly making heavy use of interest rate hedging tools to further protect their portfolios from losses due to changes in interest rates.

- They are active participants in the financial futures markets and are also making increasing use of forward commitments in which a dealer sells securities but does not deliver those securities to the customer until five days have elapsed

- A dealer does not often hold the securities to be delivered under the forward commitment but waits to acquire them near the promised delivery date.

- This strategy minimizes the risk of loss due to interest rate changes because the dealer is exposed to risk for only a brief period before delivery is made.

Inter-bank lending

- These are overnight loans between banks of their deposits at the Central bank.

- The inter-banks market is a an easy and risk less way for banks to invest excess funds held in their account at Central bank and still earn some interest income

- It is essential to the daily management of bank reserves because credit can be obtained in a matter of minutes to cover emergency situations, especially daily clearing obligations.

- The inter-banks market is very sensitive to the credit needs of the banks, so the interest rates on these loans, called theInter-bank lending rate is a closely watched barometer of the tightness of the credit market conditions in the banking system and the stance of the monetary policy.

- When it is high, it indicates that the banks are strapped for funds, where as when it is low, banks’ credit needs are low.

- The central bank can influence this rate through Open Market Operations (OMO) that is, participating directly in the money market activities as one way of influencing the level of money supply in the economy.

Eurocurrency instruments

The Eurocurrency market is an international money market that trade in deposits denominated in the world’s most convertible currencies via instruments that are similar to local CDs

- The Eurocurrency market has arisen due to the need worldwide for funds denominated in dollars, marks, pounds, francs, yen, and other relatively stable currencies.

- Euro currency markets are free of regulation of the countries whose currency is being traded in the Eurocurrency market.

- The largest among these markets is the Eurodollar, which deals with deposits of U.S. dollars in banks located outside the United States.

- Most Eurodollar deposits are short-term deposits (ranging from overnight to call money loaned for a few days out to one year) and are therefore true money market instruments

- A small percentage however, are long-term deposits, in some instances extending to five years.

- Most Euro dollar deposits carry one month maturities to coincide with payments for shipment of goods, with the others being 2,3,6 and 12 months

- There is no central location for trading in the Eurocurrency markets

- Funds flow in the market from bank to bank in response to demands for shortterm liquidity from corporations, governments and Euro banks themselves

- Traders may conduct negotiations by satellite, cable, computer networks, telephone or telex, with written confirmation coming later

- Funds are normally transferred o the second business day after an agreement is

reached though correspondent banks - Eurocurrency deposits are volatile and highly sensitive to fluctuations in interest rates and currency prices.

- They carry higher reported interest rates than many other sources of bank reserves such as domestic certificates of deposit, due to perceptions of higher risk.

Eurodollar loan rates have two components:

1. The cost of acquiring Eurodollar deposits (usually measured by the London Interbank Offer rate (LIBOR) on three or six months deposits) and

2. A profit margin (“spread”) based on the riskiness of the loan and the intensity of competition. Profit margins are low on Eurodollar loans, mainly because the market is highly competitive, lending costs are low, and the risk is normally low as well. In deciding whether to tap the Eurodollar market for funds, banks and other borrowers compare deposit interest rates with alternative borrowing costs

available in their domestic financial systems.

CAPITAL MARKET INSTRUMENTS

1. These are debt and equity instruments which have maturities greater than one year.

2. They have far wider price fluctuations than money market instruments ad are considered to be fairly risky investments.

The most common capital market instruments in use include:

1. Corporate Stocks

2. Mortgages

3. Corporate bonds

4. Marketable long-term Gov ernment securities

5. State and Local government bonds

6. Bank Commercial loans

7. Consumer Loans

1. STOCKS

These are equity claims on the net income and assets of a corporation. They confer on the holder, a number of rights as well as risks.

There are two types of Corporate stocks:

1. common stock &

2. Preferred (or preference) shares

Common Stock

- Most important form of corporate stock

- It represents residual claim against the assets of the issuing firm

- Entitles the owner to share in the net earnings of the firm when it is profitable and to share in the net market value (after all debts are paid) of the company assets if it is liquidated.

- Stock holders risk exposure is limited to the extent of investment in the company

- If a company with outstanding shares of common stock is liquidated, the debts of the firm are paid first from the assets available, then preferred stock holders are paid their share and whatever remains is distributed among the common stock holders on a pro-rata basis

- The volume of stock that a corporation may issue is known as the Authorised share capital and additional shares can only be issued by amending the Articles and Memor andum of Association with the approval of current stock holders in a general meeting

- The level of a company’s authorized sh are capital is usually a reflection of their need for equity capital and also their desire to broaden he ownership base.

- The par value of common stock is usually an arbitrarily assigned value printed of each stock certificate and its usually low relative to the stock’s current market value.

- The rights of common stock shareholders include:

- Right to elect the company’s board of directors, which in turn chooses the officers responsible for the day to day running of the company

- Pre-emptive right (unless specifically denied by the articles and memorandum of association) to purchase any new stock issued by the firm in order to maintain a pro-rata share of ownership.

- Right of access to the minutes of stock holders’ meetings and to lists of existing shareholders.

Note: some companies issue classified shares, e.g class A and B whereby class B shares have no voting rights.

2. Preferred Stock

- These carry a stated annual divided stated as a percentage of the par value e.g. a 8% preference share is entitled to 8% divided on each share held provided the company declares a divided

- They occupy the middle ground between debt and equity including the advantages and disadvantages of both instruments used in raising long-term finance.

- In case of liquidation, they are paid after other creditors but before equity holders

- They have no voting rights

- They can be cumulative- meaning the arrearage of dividends must be paid in full before common stock holders receive anything or participate- meaning they allow the holder to share in the residual earns accruing to common stock holders. Most

are however non-participative - Some preferred stocks are convertible into shares of common stock a the investor’s option

Recent developments in the area of preferred stocks include development of:

- Variable rate preferred stock: These carry a floating divided rate that makes the stock a substitute or short-term debt. Many allow their divided rate to be reset several times during the year, which ma be accomplished by a marketing agent or via a special auction.

- Dutch auction preferred shares: whereby stock buyers submit bids and the highest priced bid becomes the price paid by all winning bidders. Frequently the divided rate has a ceiling rate based on a key market reference rate such as the yield on commercial paper.

- Preference sh ares with an exchange option , giving the issuing company the choice of exchanging the preferred stock for debt securities

- “MIPS” or Monthly income preferred shares which are counted as equity but carry tax deductible interest payments like debt

Preferred shares represent an intermediate investment between bonds and common stock.

They provide more income than bonds but a greater risk

They fluctuate more widely than bond prices for the same change in interest rates

Compared common stock, preferred shares generally provide less income but are inturn less risky.

2. MORTGAGES

- These are loans to house holds or firms to purchase housing, land or other real structures where the structure or land it self serves as collateral for the loans.

- Interest cost of home mortgages is tax deductible

- Mortgages can be residential mortgages (loans secured by single family homes and other dwelling units) and non-residential mortgages which are secured by business and firm properties.

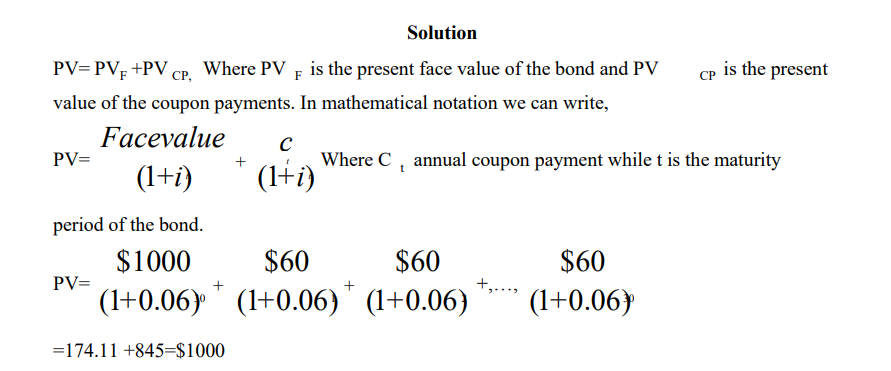

3. CORPORATE BONDS

- These are long-term bonds issued by corporations with very strong credit ratings.

- They are mainly instruments used to raise long-term finance for businesses

- They are mainly in form of corporate notes or corporate bonds .

- A note is a corporate debt whose maturity is five years or less

- A bond, on the other hand, carries an original maturity of more than five years.

- A typical corporate bond pays interest at specific intervals, commonly half yearly, with the par or face value of the bond becoming payable wh en the bond matures

- Each bond is accompanied by an indenture, a contract listing the rights and obligations of both the borrower and investor.

- Indentures usually contain restrictive covenants designed to protect holders against actions by a borrowing firm or its shareholders that might weaken the value of the bonds. Examples of restrictions include covenants that prohibit

increases in a borrowing corporation’s divided rate (which would reduce the growth of its net worth), limit additional borrowing, restrict merger arrangements or limit the sale of the borrower’s assets. - Bonds can either be term bonds – meaning bonds in a particular issue mature on a single date orserial bonds which carry a range of maturity dates. Most bonds issued by the state and local governments are serial bonds

- Most corporate bonds carry call privileges, allowing early redemption if market conditions prove favourable.

- Some bonds are however increasingly being issued without call privileges due to the trend toward shorter maturities, the added interest cost involved, and the availability of hedging instruments

- Many corporate bonds are backed by sinking funds designed to ensure that the issuing company will be able to pay off the bonds when they come due. Periodic payments are done into the fund on a schedule usually related to the depreciation of any assets supported by the bonds.

Common types of Corporate Bonds

- Debentures: not supported by any specific asset of the issuing corporation

- Subordinated Debentures: also known as a junior security_ holders are paid only after all secured and unsecured senior cr editors are paid in case of liquidation,

- Mortgage Bonds: these are debt securities representing a claim against specific assets owned by a corporation. They could be closed end or open end mortgage bonds. Closed end bonds o not permit the issuance of any additional debt against the assets pledged under the mortgage. Open end bonds on the other hand allow additional debt to be issued against the pledged assets, which may dilute the position of current bond holder. For this reason, open-end bonds typically carry h igher yields than closed-end bonds

- Collateral Trust bonds: these are debt instruments secured by stocks and bonds issued by governments and other corporations. Such a bond is really an interest in a pool of securities held by the bond issuer. The pledged securities are held in trust for the benefit of bond holders, although the borrowing company usually receives any interest and divided payments generated by the pledged securities, and retain voting rights on any stock pledged.

- Income bonds: these are often used in corporate reorganizations and in other situations when a company is in financial distress. Interest on these bonds is paid only when income is actually earned. Holders however have a prior claim on earnings over both stockholders and holders of subordinated debentures

- Equipment Trust Certificates: they resemble a lease in form. They are mostly used to acquire industrial equipment or rolling sock (such as railroad cars or airplanes).

- Industrial Development bonds (IDBs): mostly issued by a local government borrowing authority to provide buildings, land or equipment to a business firm. Because the governments can borrow cheaper than private businesses, the lower debt costs may be passed to the firm as inducement to move to a new location, bringing jobs to the local economy. The business firm normally guarantees both interest and principal payments on IDBs by renting the buildings, land, or equipment at a rental fee high enough to cover debt service costs.

- Pollution Control Bonds: these are used to aid private companies in financing the purchase of pollution control equipment. Local governments purchase pollution control equipment with the proceeds of a bond issue and lease that equipment to business firms.

4. GOVERNMENT SECURITIES

These are long-term debt instruments issued by the treasury to finance the deficits of the government

Because they are the most widely traded bonds, they are the most liquid instruments in the capital market They are held by the Central bank, banks, households and foreigners.

GOVERNMENT AGENCY SECURITIES

- These are long-term bonds issued by various government agencies such as parastatals to finance items such as mortgages, farm loans, power generating equipment, e.t.c

- Most of them function like government bonds and they are guaranteed by the government and are held by the same parties as government

5. LOCAL GOVERNMENT BONDS

- Also known as municipal bonds

- Long-term debt instruments issued by local governments to finance expenditures on schools, roads, and other large programs.

- Interest payments on these bonds are exempt from income tax

- Commercial banks are the biggest buyers due to their large incomes. Wealthy individuals, and insurance companies also buy or invest in them

Consumer and Bank Commercial Loans

- These are loans to consumers and businesses made principally by banks and also by finance companies

- There are no secondary markets for the loans, which makes them the least liquid of the capital markets instruments

- Secondary markets are however developing in some countries.

LESSON 4

DETERMINANDS OF INTREST RATES

Objective: In lesson four, learners are expected to have a clear knowledge on various types of interest rate, various ways of computing interest rate and the fisher effect.

Interest rate is the pr ice that a borrower of funds must pay to the lender to secure use of funds for a specified period. An interest rate is a predetermined or negotiated payment made or received for the temporary use of money. A financial institution will charge interest when it lends money to a consumer and a consumer will receive interest when he or she deposits money with a financial institution. It is useful to think of interest as the rental charge on money.

Financial institutions charge interest on all borrowing facilities. The borrowing facilities a consumer may utilize include:

• Personal loans

• Business loans

• Overdrafts

• Car loans

• Mortgages

• Credit cards

Interest is also paid to the consumer when he/she deposits money with an institution. A financial institution determines the interest rates it charges on its loans by evaluating its cost of funding (the interest it has to pay to borrow money from various sources), its

operating expenses and a profit margin. Financial institutions fund their loans from a variety of sources, including consumer and corporate deposits and interbank borrowings. Since interest rates can vary significantly between financial institutions, consumers should compare the interest rates offered by lenders.

Types of interest rates

1.Compound interest rates

Compound interest is interest that is charged on a daily basis. This type of interest rate keeps going and going. This is the type of interest rate that most consumers are on. The problem with this interest is that it is extremely hard when trying to find out how to pay

off debt because most of the consumer’s minimum payments go towards the interest rates each month and not the principal balance. Most creditors offer this type of interest for obvious reasons. If at all possible steer clear of this type of interest rate.

2.Simple interest rates

Simple interest is only calculated towards the principal amount that is unpaid. This type of interest is basically the opposite of the compound interest rate, it is not charged on a daily basis and the debt can be paid in a most effective manner.

3.Fixed interest rates

If you have a fixed interest rate it is an interest rate that is basically locked in for the duration of the agreement. Fixed interest rates can be beneficial, but make sure that the agreement is read thoroughly. Some of these agreements may state that after a few months the rates will increase.

4.Introductory interest rates

This is an interest rate that is given in the beginning of the offer for the time stated on the agreement and goes up later.

5.Partially fixed interest rate

This is an interest rate that allows the consumer to pay partial interest on one part of the loan and variable interest on the other. This type of rate is given a guideline from the creditor.

6.Variable interest rate

A variable interest rate varies depending on the changes in cash rate of other changes made by the provider. These interest rates basically flip flop at any given time due to the providers guidelines.

7. Fixed vs. Floating Rates

Banks generally charge either fixed or variable interest rates on their loans. A fixed rate loan has an interest rate that does not vary during the term of the loan. The interest rate on a variable rate loan can vary depending on the movement of a ref erence rate (such as

the prime rate).

Calculating the Cost of Borrowing

The advertised rate of interest on loans does not usually give a good indication of the true cost of a loan, since fees and different ways of calculating the interest charges can result in different costs to the borrower. Various ways of computing the cost of

borrowing exist.

• Annual Percentage Rate (APR)

This rate measures the yearly cost of credit and includes both interest cost and any transactions fee or charges enforced by the lender. Financial institutions should tell potential borrowers what the annual percentage rate (APR) is on a loan. The APR is calculated the same way by each institution (although the advertised rates may be calculated in different ways). Therefore, the APR can be used in comparing interest rates between institutions. If a loan has a high APR, your cost of borrowing will be high.

APR=(2INT)NP/P(1+NP)

Where:

INT is amount of interest rate paid annually

NP is the number of payment periods in one year

P is principle amount

This method is used largely by banks, Sacco’s and other lending institutions

• Simple method

This method accesses cost of a loan for only the period of time that the borrower uses the money. The total interest rate charged decreases with the increase in the frequency of borrowers payment.

I=P.R.T

Where: P=principal amount of loan borrowed, R is annual rate of interest and t is loans duration

• Compound method

Refers to the situation where the lender or depositor earns interest income on principle amount involved and any accumulated interest.

• Home mortgage interest rate method

Borrowers monthly payment in the life of the loan go almost entirely to pay the interest on the loan and only a fraction of each monthly payment later go reducing the principle borrowed.

Composition of interest rates

In economics, interest is considered the price of credit, therefore, it is also subject to distortions due to inflation. The price of a loan or credit card statement is reflected by nominal interest rate. The nominal interest rate is the interest rate you hear about at your bank. If you have a savings account for instance, the nominal interest rate tells you how fast the number of shillings in your account will raise over time. This nominal interest is composed of the real interest rate plus inflation, among other factors. The real interest rate corrects the nominal interest rate for the effect of inflation in order to tell you how fast the purchasing power of your savings account will rise over time. A simple formula for the nominal interest is:

Where iis the nominal interest, ris the real interest and is inflation. This relationship between nominal interest rate, real interest rate and inflation is known as the fisher hypothesis, fisher parity or fisher effect. Fisher effect is a proposition by Irving Fisher that the real interest rate is independent of monetary measures, especially the nominal interest rate. The Fisher equation is represented as follows for compounded interest rate:

In the case of simple rates, the Fisher equation takes a different form as shown below:

If is assumed to be constant, must rise when rises. Thus, the Fisher Effect states that there will be a one for one adjustment of the nominal interest rate to the expected inflation rate. From the equation it can be deduced that:

Real interest rate = Nominal Interest Rate – Expected Inflation Rate

Nominal Interest Rate = Real interest Rate + Expected Inflation Rate

The fisher effect has the implication that if inflation permanently rises from one constant level to a higher constant level that currency’s interest rate would eventually catch up with the higher inflation, rising by same points as inflation year from their initial level. These changes leave the real return on that currency or financial assets unchanged. In the Macroeconomic policy plane, the Fisher effect is evidence that in the long-run, purely monetary developments will have no effect on that country’s relative prices.

LESSON5

FINANCIAL INTERMEDIATION

Objectives: In this lesson, the learners should have a clear understanding of financial intermediation, the role of financial intermediation, problems of information asymmetry, information cost and the possible solutions The efficiency of an economy is much determined by not only how developed the financial system is but also by the effectives of its financial intermediation. A health economy requires a well run intermediation process.

A financial intermediary is a firm whose assets and liabilities are mainly financial instruments. The goal of financial intermediation is to pool resources from savers and lend them to people and firms who need to borrow. These institutions also play a pivotal economic function of gathering and relaying information about the financial conditions of firms and individuals which helps in allocation of resources to their most valued use. The failure of intermediation process implies the fall of financial sector and this can cripple the whole economy for instance the failure of the banking sector in the 1930s helped to bring about the Great Depression. Similar arguments exist for the Asian crisis of the late 1990s.

The Role of Financial Intermediaries

Financial intermediaries perform five basic functions which are crucial in the economy

These functions are listed below:

1. Pooling of resources from small savers

2. Providing safekeeping and services and access to the payments system

3. Supplying liquidity

4. Providing methods and avenues of diversification to reduce risk

5. Collecting and processing information to reduce information costs

A keen observation reveals that the first four functions focus on reducing transactions costs while the fifth function deals with redu cing information costs. An in-depth analysis of the three functions is given below:

• Pooling Savings

The most obvious function of a financial intermediary is to pool resources of a large number of small savers. By pooling these resources the banks can then make large loans to other people or firms. It is very unlikely that one person could finance a $200,000 mortgage or a multi-million dollar investment. However, a bank will pool together the asset of several individuals to accomplish this goal. To be effective, financial intermediaries need to attract a large number of savers. This is generally accomplished by banks who make savers feel secure in the fact that their assets are safe.

• Safekeeping, Payments System Access, and Accounting

Banks used to construct large, heavy safes which looked imposing. This safekeeping of valuables and assets is just one of several services provided by intermediaries. Banks provide services that give savers quick access to their assets through things like ATMs,

credit and debt card, checks, and monthly statements. Bank are extreme efficient at financial transactions greatly reducing their costs. Many banks also provide bookkeeping and accounting services. They help customers maintain their finances and plan for the future.

• Providing Liquidity

Financial intermediaries also provide liquidity to their customers. Liquidity is simply the ease at which assets can be turned into a means of payments and thus consumption. Banks allow their depositors to quickly and easily turn their deposits into money quickly

and easily whenever needed. Borrowers also benefit from easier liquidity. They can make loans which require repayment in a extended fashion. Intermediaries specialize their balance sheet so that they can make sizeable quick withdraws for customers.

• Diversifying Risk

Banks mitigate several types of risk. First, they take deposits from many people and make thousands of loans with these deposits. Thus, each depositor faces only a small amount of the risk associated with loans that would go default. No one depositor losses

all their assets when a bank loan goes unpaid. Banks also provide a low-cost way for depositors to diversify their investments. Mutual fund companies offer small investors a way to purchase a diversified portfolio of several different stocks.

• Collecting and Processing Information

One of the biggest problems that savers face is whom to lend their assets too. The fact is that the borrowers could lie about their true state and the lender has little ability to verify the truth. Finding out the truth can be a costly venture. The problem of information asymmetry sets in i.e the borrowers have information that the lenders do not. By collecting and processing information, financial intermediaries reduce the problems associated with asymmetric information. Loan applicants are carefully screened. They monitor loans for timely payments hence reducing this information problems. These information problems have huge implications on the financial systems.

INFORMATION ASYMMETRIES AND INFORMATION COSTS

Information is a central element to efficient markets. When the costs of obtaining information are too high, some potentially beneficial transactions do not take place and markets tend to stall. Information costs sometimes make financial markets the worst functioning markets. In most all transactions, the issuer of a financial instruments, borrowers, know some information which the buyer, saver, does not know. This is a situation know as asymmetric information. There are two information problems which form obstacles to smooth running financial markets. The first problem is called adverse s election . This problem arises before the transaction ever occurs. Simple fact is that lenders need to know how to differentiate between good risks and bad risks.

Unfortunately for them, that is information only the borrower has. The second type of information problem is called moral hazard . This problem occurs after the transaction has taken place. Lenders need to find a way to tell whether borrowers will use the proceeds of a loan as they claim they will. We should look at some examples, their details and implications of these problems and their implications.

Adverse Selection

One of the best documented situations in study of asymmetric information is the Lemon’s Problem. This problem was revealed by 2001 Nobel Prize winner in Economics George Akerlof in his analysis of markets with asymmetric information. His contribution came from a 1970 paper titled “The Market for Lemons” in which he explained why the market for used cars, some of which are “lemons”, does not function well. Suppose two cars are for sale, both of the same make and model. One is in good shape and was owned by a previous owner who maintained a good maintance record and drove very little. The second car was owned by someone who sparingly changed the oil and loved to drive in the fast lane. The owners of the cars know whether their own car is in good repair, but the buyer does not. Let’s say the potential buyer is will to pay $15,000 for a well-maintained car and $7,500 for a lemon. The first car owner knows the car is in good shape and won’t sell it for less than( $12,500. The other owner knows that the car is in poor shape and would be willing to sell for as little as $6,000. Without knowing anything else about the car, the risk-neutral buyer would only be willing to pay the expected, average, price for these cars wh ich would be $11,250. That is less than the first owner is willing to sell for, thus the only car we can buy is the lemon. In this type of world no one with an above average car would ever put their car on the market. Thus,

the market is full of lemons. Due to this asymmetric information, Several entities exist that help solve this problem. Consumer reports can be established about the sellers of used cars.

Many people now offer warranties on used cars and buyers can use mechanics to help verify the true state of the car. As a result we should find the prices for good and bad used vehicles closer to their true value. When it comes to financial markets, this adverse selection problem exists just as it exists with used cars. Potential borrowers know more about the projects they wish to finance than potential lenders. In the same way that adverse selection can drive out the good cars this situation can drive good stocks and bonds out of the financial market.

For instance, two firms, one with good prospects and one with bad prospects, as a potential stock buyer, since you cannot tell which firm is which, you would only be willing to pay the average stock price as a risk neutral investor. The stock of the good company would be undervalued. Since managers of this company know that their stock would be undervalued, they would never bother issuing it in the first place. That leaves only the firm with bad prospects in the market. This would be known by investors and the market would have a hard time getting started.

The same thing can happen in the bond market. Risk requires compensation and if you cannot tell the high risk bonds from the low risk bonds, the lender will demand the average premium on all bonds. This drives companies with good credit out of the market unwilling to pay the inflated interest rate. Since lender are not interested in buying debt from bad companies, the market would not function.

Solving the Adverse Selection Problem

The adverse selection problem creates situations where good companies will pass on potentially valuable investments. Since these investments are lost, the best companies are not necessarily the ones that grow as rapidly as they should. At the same time,

poorer companies may take on investments which they should not be doing. So, it is important to identify the good companies from the bad companies. There are two basic methods for solving problems of adverse selection:

Create more information for the investors

Disclosure of Information the most straightforward solution to adverse selection Since it creates more information. This can be done by government regulation or through other market forces. Most publicly traded companies are required to release a lot of information through requirements set up by the Securities and exchange regulatory authorities. Public companies are also required to release information which can influence the wealth of the company and any information that is given to professional stock analysts. The newly created accounting regulations are geared at closing these loop holes through which firms may be able to hide the true financial position of a firm.

Guarantees

Another way of solving this problem is providing guarantees in the form of contracts that can be written such that the owners of the firms face the same risks as the investors. The contract is written in such a way that lenders are compensated even if the borrower

defaults on the loan. If the lender is guaranteed a payment, some bad credit risks no longer look so bad. There are two ways to ensure that a borrower is likely to repay a lender: collateral and net worth . Collateral is something of value pledged by a borrower to the lender in the event of default on a loan. This collateral is said to secure the loan. In many situations, the collateral for the loan is simply the good that is being purchased by the borrower. For example: a house is collateral for a mortgage and the car is collateral for an auto loan. In this adverse selection is not much of a problem. In either case the lender gets paid and the borrower only gets a payoff if they meet their financial obligations. Loans without collateral (unsecured loans) generally have higher interest rates. The lender is taking on more risk and must be compensated.

Net worth is an owner’s stake in a firm. Under many cases, new worth serves like collateral. If a firm defaults on a loan, the lender can make a claim on the net worth of the firm. Of course if the firm has no or negative net worth, the lender would receive nothing, but in general the lender would still get some form of a payoff. In this case the lender still faces risk from changes in the value of the firm.

Moral Hazard: Problem and Solutions This problem can be clearly understood through a keen look in to insurance markets. An