- Purpose and structure of co-op banking

- Purposes of co-op banking

- Structure of co-op banking in Kenya

- Organisation charts of various co-op financial organisation

- Roles of various financial organisations in the co-op sector.

- Credit programmes and policies

- Definition of the term credit

- Sources of loaniable funds

- distinction between production and consumption loan credit programmes

- conditions for participation in credit programmes

- criteria for classification of loans

- credit policy for union banking section and Saccos

- Loan package of loan funds

- what is a loan package

- preparation of loan package and loan priority list

- importance of loan package and priority list

- Acquisition of loan funds

- procedure for loan application in co-op bank of Kenya

- Union banking section

- member qualification

- upper loan limit

- Short term

- Medium term (phase I)

- Medium term (phase II)

- Contents of loan application form

- Loan granting procedure

- loan withdrawal and recording procedure

- withdrawal procedure

- loan recording

- loan reconciliation

- loan repayment

- explanation of loan terms

- causes of loan default

- minimisation of loan default

- consequences of loan default

- co-operative saving scheme

- Meaning of co-op saving scheme

- Historical background of co-op saving scheme

- Purpose of co-op saving scheme

- conditions for participations in co-op savings scheme

- Union banking system

- Factors necessary for establishing a UBS

- Visibility studies for UBS

- Centralised and decentralized members savings

- Advantages and disadvantages of centralised and decentralized banking system

- Union banking services

- Savings account services

- Conditions for opening and operating savings a/c

- Members savings account and members personal account

- opening of a member savings a/c, personal a/c

- posting of transactions of members savings a/c and members personal/c

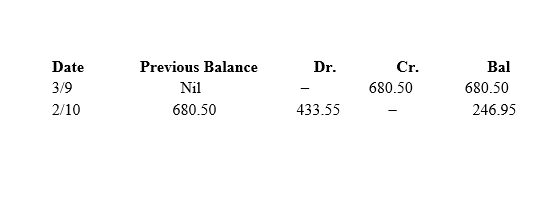

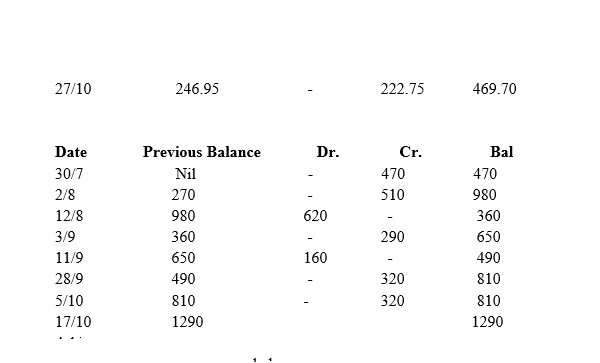

- Reconciliation

- Definition of the term reconciliation

- importance of reconciliation

- opening and posting into various a/cs

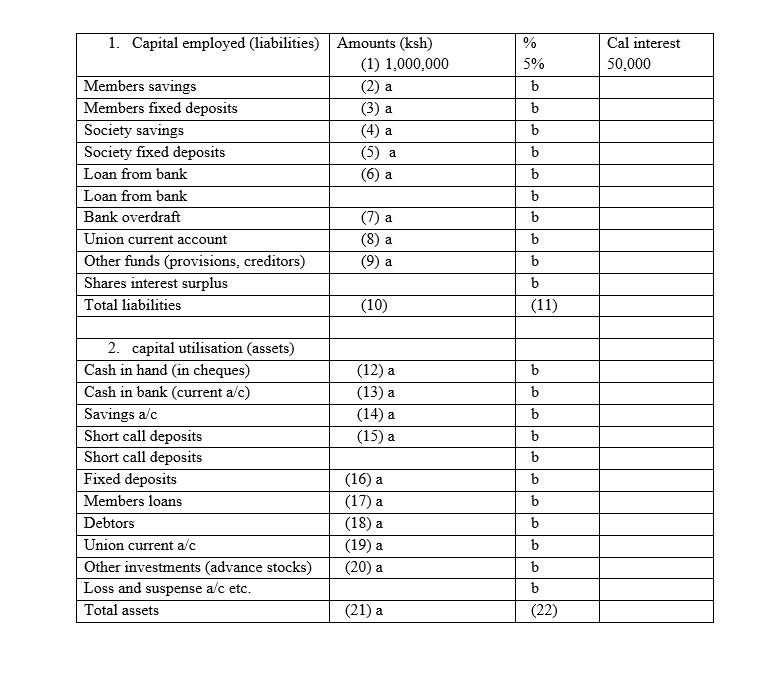

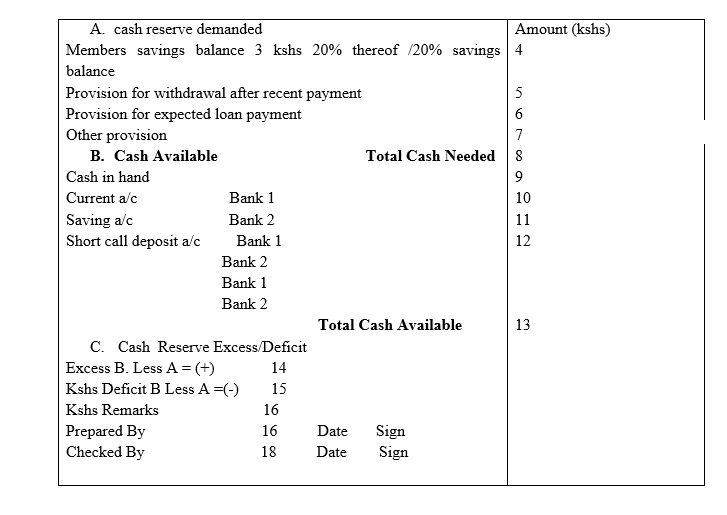

- liquidity and investment

- Meaning of the term liquidity

- preparation of cash inflow and cash outflow

- calculation of liquidity margin

- action taken on the basis of above calculations

- priority consideration in investment

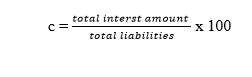

- Profitability margin

- explanation of profitability margin

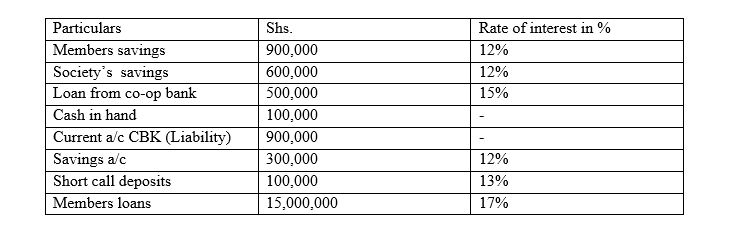

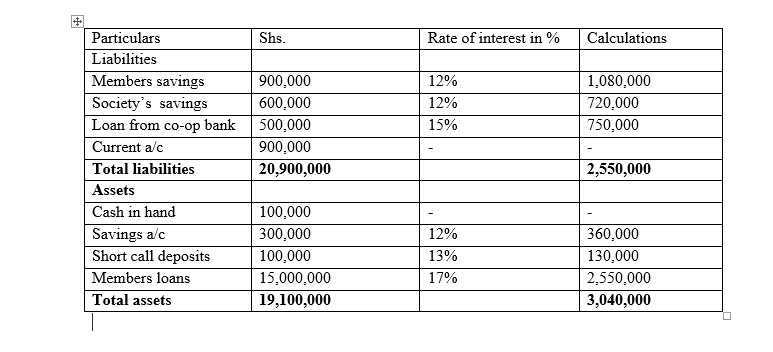

- sources of capital in the UBS

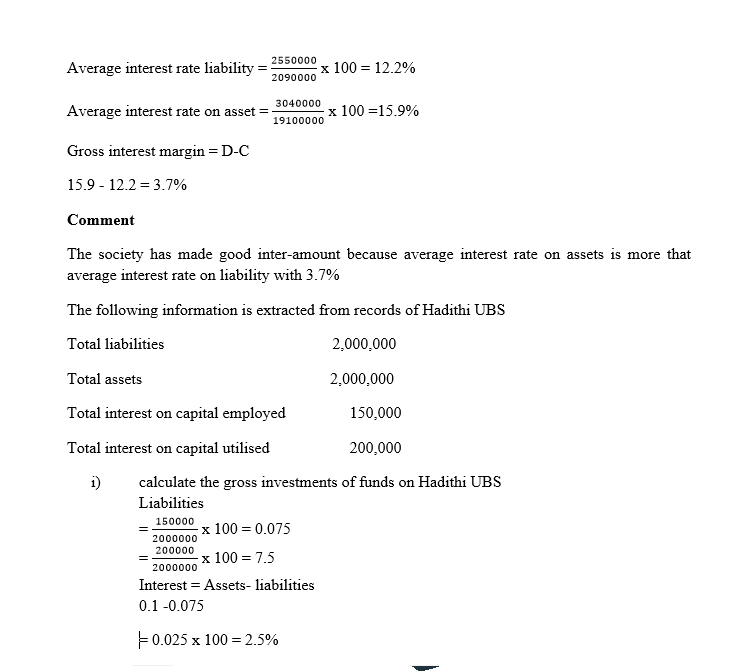

- calculation on rate of returns on capital utilised

- composition of capital utilised

- calculation of cost of capital employed

- calculation of the grass interest margin

- actions arising from the gross interest margin

- Security Arrangements

- Physical security measures in the UBS

- Control measure in the UBS

- Insurance requirement in the UBS

- Structure and Daily Operations Of Saccos

- Functions/roles of various people in the Saccos

TOPIC 1

Purpose and structures of co-op banking

Co-operative banking system

The co-op banking system consists of:-

- co-op bank of Kenya

- union banks

- co-op rural and urban Saccos

- marketing society

It is an organised system whereby the members of the co-op movement are provided with banking services in line with co-op ideas/policies /principles

The co-op bank operates under the co-op society’s act and the banking act

The co-op banks works through the head office in Nairobi and a number of its branches countrywide

It functions as the central bank in the system where a rural Sacco has excess funds it invest in the co-op bank.

However where the rural Saccos experiences liquidity problems it can borrow from the co-op bank of Kenya

The bank also gives some other types of services e.g. management of systems investment analysis and advice to urban or rural Saccos.

The structure shows the central bank as a banker to all commercial banks including the co-op bank of Kenya.

The co-op bank system operates from the central bank of Kenya through the co-op of Kenya down to the union banking section, rural Saccos, credit sections, non-affiliated Saccos and finally the individual members of the co-op movement.

The co-op bank system operates aims at the meeting its needs through:-

- providing efficient payment for produce market through the societies

- providing savings custody facilities to their members

- Providing credit facilities to co-operative organizations and to individual members

- accumulating savings for development activities

- assisting in education in the use of banking services and financial management

- it exposes the farmers to banking services

Co-operative bank of Kenya

It was registered as a co-op society on 19th June 1965

On 10th Jan 1968 it registered under the new banking act

It was until 1969 when it started offering banking services

Reasons for these were:-

- it needed to be registered under the banking act to operate as a bank

- minimum capital requirement for the banking act had not been met

- it had operational problems i.e. whether the bank would started operating with branches in every province or it could start with one branch in the head office and open branches later

The problem of share capital was solved through exemption and the bank would operate from one branch in Nairobi. It: – started operating in 1969.

Membership of the co-op bank

The members of the bank (shareholder) are:-

- registered co-operative societies

- co-operative unions

- countrywide co-operative organisations

To become a member the following requirements have to be fulfilled

- Accept the by-laws of the bank

- Undertake to purchase not less than the minimum number of shares as it is decided by the bank from time to time.

Objectives of co-op bank

The co-op bank of Kenya was established to achieve the following objectives within the co-operative banking systems

- Mobilizing the financial resources of the co-op organization and to avail this capital circulation by distributing credit to co-op members according to the need without relying too much in borrowed funds.

- organise appropriate saving services to the co-operative organisation

- to channel outside financial resources from donor agencies into the co-op sectors

- assist the co-op sector in the international trade

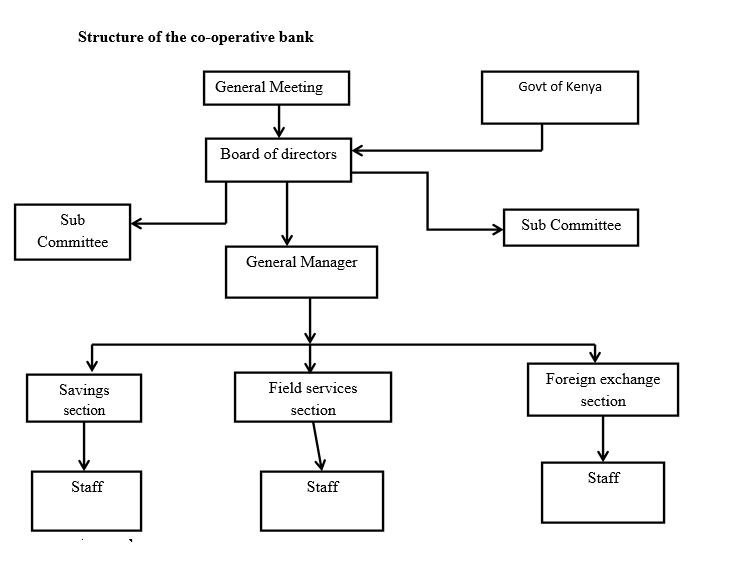

General meeting

The AGM is composed of delegates from provincial electoral zone

Each member within a provincial electoral zone will elect 2 persons

There are 8 provincial electoral zones namely: – Nairobi, Central, Riftvalley, Western, Nyanza, Coast, Eastern, and North Eastern

Board of directors

At the AGM the BOD is elected. Each provincial electoral zone will elect their representative as follows:-

Central province 2 board members

Nairobi province 2 board members

Eastern province 1 board member

Western province 1 board member

Nyanza province 1 board member

Riftvalley province 1 board member

North Eastern 1 board member

Coast Province 1 board member

Total 10 Board Members

Representation of the Kenya board members comprise of:-

Commissioner of co-operatives

Permanent secretary in ministry of co-operative

Permanent secretary treasury

A representative of the central bank of Kenya

Sub Committee

The by-laws of the bank provide for election of the sub-committee to various specific areas

The decision of the sub-committee is subject to verification by BOD

LIBDQUIST REPORT

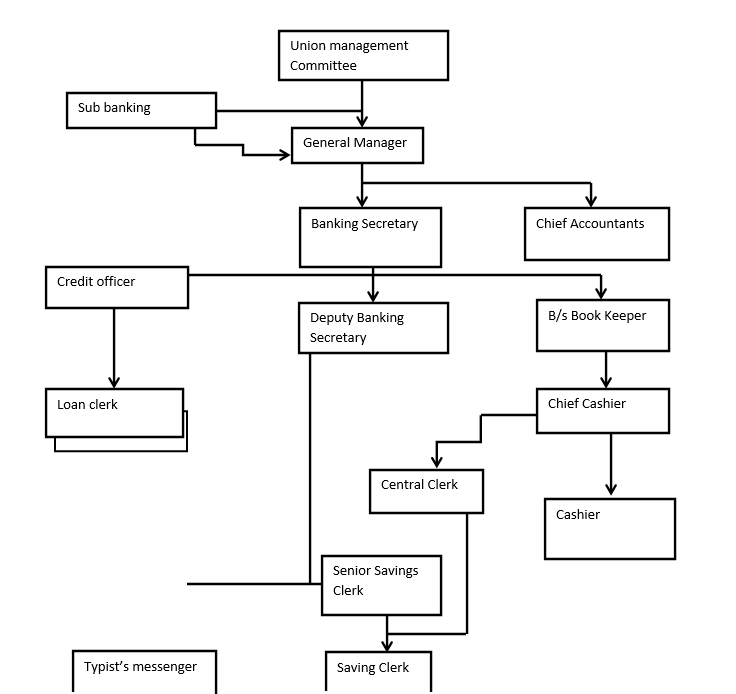

Union Banking section

Although the co-op bank was setup to serve the co-op union and societies, the individual member continued to have problems due to lack if appropriate savings facilities within the co-ops.

At the same time the members pay outstanding increased and need for banking services through which the prompted for the establishment of UBS

in order to find out how the members could be helped, a survey was conducted by the ministry of co-op development and the nomadic mission to Kenya to look into ways and means of starting a saving scheme and credit facilities

This survey came up with the Lindquist report which had the following recommendations

- the co-op should find ways and means of building up their own fund for venture and extension of credit facilities to small scale farmers

- the shareholders were to raise enough capital to make the bank self-supporting without relying too much on borrowing funds

Out of the report that the co-op bank was established in 1970, co-op banking section was started in kiambu district by the kiambu coffee grower’s co-op union. Under the guidance of Nandi advisor, the success of the union banking section made the government to encourage other unions to start their co-op savings scheme.

In 1972, Murang’a started theirs. Thereafter, union banking sector were started in Kirinyaga , Nyeri, Kissi , Meru, Central, Machakos, Nyahururu, Sugarbelt, Kiambu diary and pyrethrum, then Embu, Bungoma, Kinangop, Al Leareto, Mwea and Mashamba Union.

The major aims of the UBS are:-

- to organise appropriate savings facilities to farmers

- to mobilise persons savings /resources for local development

- to promote appropriate credit facilities

Organisation Chart

Any organisation chart is an arrangement of framework of b/s activities within which people work

It shows the responsibilities, duties of command and communication within the business enterprise for efficient accomplishment of the organisation objectives.

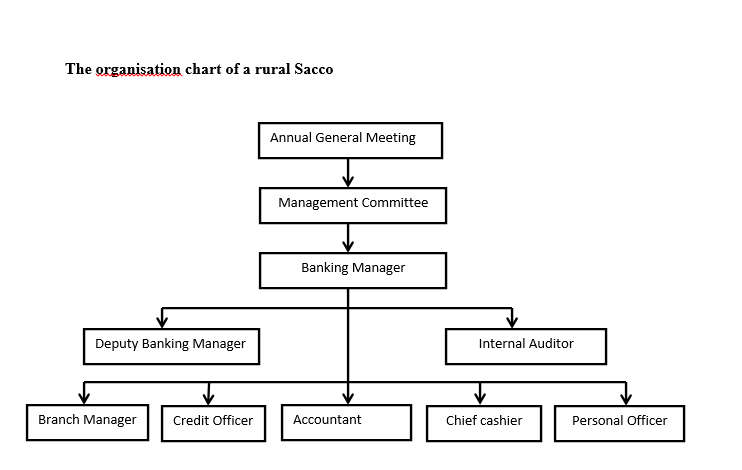

Organisation chart of a rural Sacco

The AGM is the highest authority within a Sacco organisation

It consists of members and employees of the Sacco and any minority official in accordance with the by-laws.

UBS Organisation chart

The main duties of AGM are:-

- approve audit a/c

- approve the budget which includes all capital expenditure

- elect the members of the management committee

- any other matter as contained in the act or by laws

Management committee

The management committee consists of members elected by the AGM

A committee must meet once in a month

Powers and duties of management committee

- Loan – The committee determines the allocations of loan of members

- Supervise and ensure the rules and regulations are complied with

- Together with the district co-op officer and the district agricultural officer, work out a detailed use of loan priorities (ie which project to be considered to be given loan first)

- Follow the issuing and usage of loans by members

- Grant or reject individual member application

- Follow the repayment of loans, members debts and charge of interest through monthly report

- Decide on legal action against defaulters

Savings- They ensure that they are compliant with the rules and regulation laid down by the co-op society act in regard to the savings activities

- follow up the development of services to members and suggest changes on the terms of savings

- any other issue dealt with is empowered by the annual delegate meeting

Other powers and duties of management committee

- pay special attention to the prepared report and make follow up of these reports by having surprise checks and special scrutiny.

- to follow closely through the report, trial balances, budget of the economy of the society

- to introduce motion for consideration by the AGM through the following matters

- Through proposed budgets and related matters

- Suspension of members from participating in savings and credit scheme in case of violation of regulation of this scheme

- Terms and conditions for loan and savings including rate of interest

- to recommend limits for maximum borrowing powers of the society in the application to the commissioner

- to delegate responsibilities e.g. to the sub -committee

- holding meeting atleast once per month

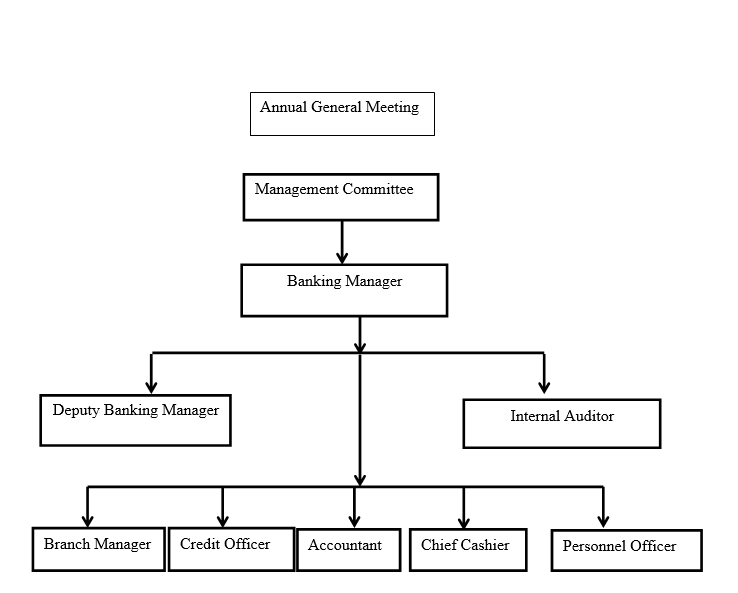

The banking manager

This is an employee of the Sacco who reports to the management committee and shall be an ex-officio member (he is not elected but becomes a member because he holds the office) of all committee and sub- committee of the sacco except a committee appointed to enquire into any matter in which he is personally concerned.

He has no right to vote because he is not elected by the members

He is responsible for the day-to-day running of the affairs of the Sacco

We have 7 people who report directly to him

- accountant

- credit officer

- chief cashier

- personnel officer

- internal auditor

- deputy banking manager

- branch manager

Deputy banking manager

- He acts as the banking manager if the banking manager is not in

- He is incharge of the headquarters branch

- He is incharge of the savings section within the headquarters

- he is incharge of mobile services and reports directly to banking manager

Internal auditor

He is incharge of audit within the Sacco and reports to the banking manager

Branch manager

He is responsible for the total branch operations i.e. saving services, mobile services, loans on branch office etc.

He reports directly to the banking manager

Credit officer

Responsible for receiving and processing loan application

Responsible for maintaining the loan accounts or any other matter pertaining to loans

Supervises the loan clerks

Accountant

He is incharge of all accounting matters in the sacco

He is incharge of supervising book keepers, accounts clerks etc

Chief cashier

Responsible for safe keeping of all cash

Responsible for all cash handling

Supervises all cashiers

Personnel officer

Responsible for all personnel records and handling of all personnel matters

Responsible for all daily administration as directed by the general manager

Supervises personnel and administrative clerks and all the subordinate staffs.

NB the main difference between the organisation chart of a sacco and that of a UBS is that the sacco is completely independent with its own AGM, management committee and banking manager while the UBS has an advisory banking sub-committee and the section is headed by a banking secretary who reports to the general manager.

Urban Saccos

In the co-op banking section, the urban Saccos play a vital role of mobilizing personal savings from the employed individual members of the national workforce for local development.

About 90% of urban Sacco members have benefited from loans dispersed by Saccos where personal savings from individual members is not sufficient. The Saccos are financed by the co-op bank of Kenya according to their needs

The loans have substancially assisted in the development of the county in all the fields of business including:-

- purchase of land, house, furniture , household goods etc.

- shares and variety of other investments

- building of shops and houses

- meeting urgent expenses e.g. legal and hospital bills

- sponsoring the employees for education and training

The credit programmes in the co-op sector

Credit may be defined as the process of obtaining the control of money, goods or services in the presence in exchange for promise to repay in future i.e. the borrower obtain the resources to use for current production or consumption purpose b/s doing the savings that would be otherwise required to pay for this services if credit were not available

There are two types of credits

- Production credit

It’s the credit that has been connected to save economical activities so that the borrower will have a higher net income after he has repaid the loan e.g. credit to purchase fertilisers, building rental houses buying a public vehicle

- Consumption credit

It is the credit that is channeled to purposes which do not improve the net income of the farmer or help the farmer to repay the loan e.g. credit for a marriage dowry, a living house, school fees.

NB Rural credit programmes aims at improving the agricultural aspect which intern would lead to higher standards of living and improvement in the national output and social economic development.

Aims of credit programmes

It aims at developing, promoting and supervising the following:-

- well controlled credit schemes

- provision of produce buying funds

- co-op org to manage their credit skills

- members savings and deposits facilities

- short-term loans and medium term loans

- training of farmers , official, committees, members and staff

- follow up on the utilisation of credit loan repayment

- Special rural credit programmes for small scale holders the potential for increase production.

Credit programmes in co-op sectors

- P.C.S- co-op production credit scheme

- A.D.P- integrated agricultural devt programme

- I.S.S-farm input supply scheme

- P.S.C.P- small holder production services and credit project

- C.I.P- small holder coffee improvement project

- P.D.P-national poultry devt project

- S.C.S- new seasonal credit scheme

C.P.C.S (Co-Op Production Credit Scheme)

It was started by the Kenya govt in 1970 to channel credit facilities to small scale farmers

This scheme is meant to improve or to increase agricultural production

Aims

- helps develop understanding of modern farming methods

- increase yield and better quality crops

- help increase farmers income from increased yield

- increase savings capacity as a result of increased income

- Generally help develop the area where it is operating.

Sources of funds for the scheme are:-

- own funds –i.e. members savings in the UBS

- borrowed funds –i.e. from the co-op bank of Kenya

Individual member’s qualification

The conditions which are to be fulfilled to quality for a loan under this programme are:-

- A member should market their produce through the society during the last 3 years.

- the member should be less than 18years

- should be an active member of the society

- should have repaid all the outstanding debts or secured them

- Legal owner of the land cultivated. If not the legal owner should appear as me of the guarantees is aimed at securing the loan.

- should be considered honest, hardworking and trustworthy

- To qualify for the medium term loans a member should not have a long term loan from another unless that org give consent in writing.

The society’s qualifications

To qualify for participation for credit scheme a society will have to meet certain minimum requirement

- be financially sound

- have a management committee

- have been in operation for atleast 3years

- have update records for atleast 3years e.g. books of a/cs

- good stuff and secretary/ manager capable of running e.g. affairs of the society properly

- have the society committee, secretary/manager and other staff properly trained in credit activities

- pass certain resolutions in the society management, committee and general meeting

- obtain funds for lending within the society o from outside source e.g. union and co-op bank

- Give members of the society necessary information about the aims and conditions of the loans and the application procedures.

Union qualifications

Before a union can participate in cps, it must fulfill the following conditions:-

- Appoint a banking /credit committee composing of 3-5 members. This subcommittee will handle the loan processing activities

- Establish a banking /credit section on a model organisation chart so as to determine the number of staff that will be required.

- appoint a qualified banking or credit secretary to manage the operation of a credit section

- formalize all outstanding debts i.e. the debtors must be followed up and made to repay their debts

- pass certain resolutions in the union management , committee and general meeting

- Carry out adequate education of members. committee and staff on C.P.C.S rules and its benefits

- apply to the commissioner of co-op for appraisal to be allowed to participate in the C.P.C.S programmes

Types of loans that are given to this programmes C.P.C.S

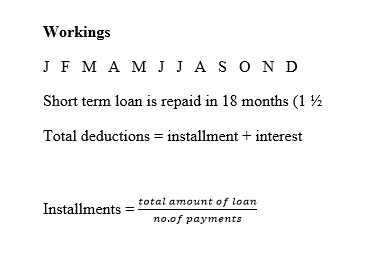

- short term loans- takes 1 ½ years (18months)

- medium term loans phase I- 3 years (36months)

- medium term loans phase II- 5 years (60months)

Mr. Kioko crop proceeds for the last 3 years were as follows:-

1984 10,000

1985 9,000

1986 11,000

Total 30,000

Calculate what Mr. Kioko will get under short term loan, medium term loan phase and medium term loan phase II

- Short Term Loan

x 30,000 =6,600/=

or

x = 6,600/=

2. Medium Term Loan-Phase I

x 30000 = 15,000

3. Medium Term Loan –Phase II

x 3000 = 24,000

NB short term = of average annual cash value of the crop

Or

22% of 3years crop value

Medium term phase I = 50% of 3 years crop value

Medium term phase II = 80% of 3 years crop value

- Short Term Loans

It has a maximum repayment period of 18months (11/2) years

A member can only be granted 2/3 of the annual cash value of the crop market through the society for the last 3years or 22% of 3 years crop value marketed through the society

No loan less than shs. 500 should be given to any member

2. Medium Term Loan Phase I

The repayment period for this loan is 36 months and the amount of loan that a member can get is 50% of his last 3years crop value marketed through the society

Any amount excess of kshs. 10,000 will require additional security

- Medium Term Loan Phase II

Its repayment period is 60months (5 years) and the limit hat a member can be given is 80% of the crop value marketed by him through the society for the last 3 years.

Intergrated agricultural devt programme (I.A.D.P)

This is the project finance by the World Bank and e- fund i.e. international fund for agricultural devt

The loan scheme support the following activities

- store construction

- recruitment of staff

- subsidiary operating expenses

- recruitment of additional ministry staff

- foods for farmers training

NB they target those subsistence farmers in marginal arrears

AIMs of I.A.D.P

- increasing production of food crops

- creating opportunities for upgrading livestock’s

- intensified soil and water conservation activities as a support measure

F.I.S.S (farm input supply scheme)

The F.I.S.S was introduced by Davida to make farm inputs ready available to small scale co-op farmers in less developed areas of Kenya

The assistance is given through:-

- provision of credit for produce stores constructions

- seasonally credits for farm inputs to the members

- provision of storage facilities for far, inputs

- management service and training of personnel

The target group consists of individual farmers with unexploited farming potential and these credit facilities enable them to explore these potentially productive areas.

S.P.S.C.P (small holder production services and credit project)

This was introduced by USAID in order to improve and dev the capacity within the co-op system.

Aims

- Organising comprehensive production

- Marketing of produce for small holders who have potential of increasing production.

These are the potential of increasing production but have not benefited from credit services

The projects is aimed at improving the following

- Co-op mvt

- food production credit

- input delivery system

- marketing services

- agricultural technical assistance

- programme management

S.C.I.P (small holder’s coffee improvement project)

This project is aimed at improving the quality and quantity of small holder coffee farms through rehabilitation of coffee farms, coffee factories and improved extension services.

The type of credit offered under the scheme include:-

- clearing and weeding coffee shambas

- purchase of farm inputs

- pruning and fencing

- factory rehabilitation/ construction

The target groups are small holder’s coffee who have not sufficiently benefited from other credit programmes such as SPSCP.

These farmers may have had production in the past but has neglected their coffee

This project is funded by World Bank.

N.P.D.P (national poultry devt project)

This was introduced by the govt of Kenya and Netherlands to assist the small poultry keeping farmers by the devt of commercial poultry farming

The project was introduced to assist in providing alternative source of cheap protein by providing more eggs and broilers.

The assistance include:-

- purchase of inputs

- improving indigenous poultry production

- production techniques /methods

- marketing org and economic research

This projects started with pilot project co-operation in the project area with project is to start with atleast 24 eggs production farmers and 10 broilers production units.

N.S.C.S (new seasonal credit schemes)

This is programme was introduced by the govt to support existing credit scheme for increased production

It was introduced to replace the guaranteed minimum return loans scheme which was being run by AFC (Agricultural finance co-operation) and the govt for maize and wheat farmers. Currently, credit for farm with less than 5 hectares of land is financed through the co-op mvt while those with 5 or more hectares are financed by AFC.

AFC- an or that specializes in agriculture and rural devt segments of the economic through consultancy and technical support.

Agricultural co-operative credit policy (ACCP)

the main objective of ACCP is to improve economic and social welfare of the co-op members and the credit policy is expected to achieve the following major goals

Goals

- to establish a fair loaning system

- to assist co-op members in identifying viable projects

- to establish efficient credit administration procedure

- to ensure proper utilisation of and recovery of loan funds.

The members loan conditions

Loan application by members of the Sacco shall be done by the credit committee and presented to the management committee for consideration and approval

The loan application shall be considered on the basis of 1st serve

To qualify a loan from a Sacco society the member must meet and fulfill the fall

Major conditions

- Active member- the member must be active in that he should deliver his produce for marketing in the co-op society case of produce marketing society e.g. coffee, dairy, cotton, tea etc.

- Good character- the applicant should be a person of high integrity, honest and trustworthy. his past loan repayment records must be clean

- viability-the applicant should make a viable market proposal in accordance with credit purpose of this policy

- Age-the applicant must be the atleast 18years old.

- Land ownership-the applicant must be the owner of the land cultivated by him if not the owner must appear as one of the guarantees and where he is not a member must give a letter of undertaking.

- Total debts- a borrower should not be eligible for capital devt loan if the borrower has a long term loan with another lending institution.

Types of loans offered under A.C.C.P

- working capital

This type of loan cover activates such as: – land preparation, procurement of farm inputs, hiring labour, transport, maintenance and repair of farm machinery.

Members who qualify for this loan will be granted a maximum of 30% of the immediate past total value of produce marketed through the society.

The minimum loan that members may be granted under this category is kshs.500

The repayment period of this type of loan is 1 ½ years (18 months)

1. Musendos crop value for 3years was given as follows

1986 -4800 1987-6200 1988-8400

Calculate what Mr. Musenda will qualify for under the working capital loan.

x 8400 = 2520

This type of loan replaces the short term loan under the co-op production credit scheme (C.P.C.S)

2. capital devt loan

This type of loan is intended for perennial crops, livestock, irrigation systems farm machinery, vehicle purchases, agro-chemical industries, construction of houses, buying of salon cars etc.

The amount for which a member can be granted is 80% of the total value of 3years produce marketed through the society

The minimum to be granted is ksh.1000

Repayment period is 60 months (5months)

It replaces the medium and long term loan under the C.P.C.s

Mr. Musendas crop value

4,800 + 6,200 + 8,400 = 19,400

x 19,400 = 15,520

3. welfare loan

This type of loan will be granted to the members to pay school fees, legal bills hospital bills etc.

The loan advance for this activity shall be based on the value of members produce delivered to the society and not yet paid for.

A member will qualify for a maximum of 20% of the production + the value of the member’s shareholding subject to the society liquidity position

The repayment period is 12 months (1year)

Loan securities

It’s a property or undertaking given in support of a loan lender to make it harmless for the lender in the event of default.

- welfare loan

Loans are secured against members produce delivered to the society member’s shares and 2 guarantors.

A guarantor is one who undertakes to pay the loan in case the applicant defaults.

working capital and capital devt loan

The loan types requires security such as guarantors, members proceed marketed through the society title deeds etc.

NB

Working capital- 30% of the immediate total value of produce marketed through the society

Capital devt loan- 80% of the total values of 3 years produce marketed through the society

Welfare loan-20% of the production + the value of the member’s shareholding

Loan package and loan priority list

It involves various types of inputs that any farmers may require when he wants to venture or go into same produce purpose or it’s an enterprise budget per cost of investments.

It is an assortment of cost of inputs that is required by unit of investment by a farmer and expected output

Loan packages are usually grouped in their priority order taking into consideration the investments that correlate directly to the agricultural production e.g.

1. packages of 1st priority

They are enterprise whose investments are directly agricultural like coffee, tea, pyrethrum, diary, maize etc.

2. Packages of 2nd priority

Are enterprises whose investments are directly connected towards the improvement of agricultural production in 1st priority e.g. tractors, ox-ploughs, water pumps and tanks etc.

3. Packages of 3rd priority

they are nay of her type of investment that will generally assist in raising the std of living of a farmer but does not in any way fall under the 1st and 2nd above e.g. money for putting up a new house, purchase of TV, car, radio, shoes etc.

NB once the loan packages for all the enterprises have been prepared they are grouped and listed according to priorities. This is called loan priority list

When preparing a loan package it is necessary to project the expected output i.e. the return should be adequate enough to cover the cost of investment and leave the farmer with some surprise.

The loan packages are usually prepared annually at district level as the cost of inputs keep on changing every year and also the climatic and physical features of the district value.

Persons responsible for loan preparation at district level

- district co-op officer

- district agricultural officer

- union manager

- credit secretary

- assistant co-op officer

Loan priority list

It’s a document giving in order of importance the projects which are to be financed through a credit programme

It’s prepared on district basis taking into consideration the climatic, economic and agricultural conditions

It may be uniform for one district but may also be valid for different divisions, locations etc.

They are also prepared annually for each district

They should be tailored to suit the devt plan for the district as closely as possible

It is prepared by DCO, DAO, UM, CS, ACO

The loan priority list should show the loan repayment period for cash loan

Examples of a loan priority list

Loan priority list

Kiambu district

Coffee extension

Dairy farming

Irrigation

Piped water

Co-op saving scheme

It’s an activity a co-op org either at union or society level with the main objective of providing saving services and eventually offers savings facilities to the very members who save with the scheme.

Aims of the co-op savings scheme

1. To provide appropriate savings facilities to the co-op members.

The minimum balances that were being demanded by the commercial bank were too high for the farmers to raise hence they resorted into keeping their monies in odd places where security was not guaranteed. The scheme now was, established to provide a safe custody for the members’ funds as well as earning interests for the account holders.

2. Help mobilise personal savings- money kept in people’s houses is ideal and does not contribute to the national economic development. There is need to make co-op members bring their personal savings to a place where money could utilised for national devt.

This was also seen as a way for the co-op movement to create its own funds instead of depending on borrowed funds.

3. To provide appropriate credit facilities-the farmers had very little to offer as security to the commercial bank for any loans they needed. The time required between co-op delivery and payment was lorry and they were finding it very difficult to continue producing in the absence of credit.

Qualification for operating a co-op saving scheme

Every co-op that wants to participate or run a co-op saving scheme must fulfill certain conditions it requires to:-

- Appoint a banking committee to supervise the operation of the co-op banking section.

- has a good financial position in order to assure to the members that their funds will be safe

- establish a co-op banking section with proper facilities for operation

- appoint a qualified banking secretary to manage the co-op banking in a professional manner

- all members debts should be formalised in order to ensure that all old debts are reserved and those not recovered are fully secured for recovery.

- both the union committee and the general meeting should pass a resolution to operate a co-op banking section

- Carry out member’s education in all affiliated societies. this is because members need to be informed on how the bank will operate and how they can get the services

- the audit of the union should be upto date so as to reveal the financial position of the union at the starting this activity

Society conditions

To qualify for participation in the savings scheme, a society will have to meet certain requirements

- the society will have been in operation for 3 years

- to have updated records of atleast 3years

- the society should be financially sound

- should have a good committee, staff and the secretary manager capable of running the society affairs

- Give members necessary information about the aims, conditions of the loan, loan application procedure and list of loan packages.

- formalize all outstanding loans owned to the society and pass certain resolutions in the society

- shall obtain adequate funds for lending either internally or from outside

Feasibility studies for implementation of the saving scheme

by establishing a savings scheme it’s important to carry out the necessary feasibility studies in the area of operations and based upon results, prepare a proper plan implementation.

Steps in implementation of a savings scheme

- evaluation

It will cover the following areas:-

- preliminary studies to establish the need for staring the savings scheme

- feasibility studies in the following aspects

- technical requirements study

- technical feasibility study

- economic feasibility study

Technical requirement study

The technical requirement study shall make clear:-

- whether the co-op org qualifies for operation under the savings scheme or not

- the crops marketed by the society and how the systems of payments are organised

- the frequency of payments presently maintained e.g. on delivery, monthly, quarterly, yearly

- whether the relevant m.t systems have been implemented and if not which steps are being taken to do so

- which type of deposits and credit facilities will be established

- The quality of such services i.e. daily, weekly, monthly etc. and the number of hours per day possibility of organising savings, withdrawal and deposits services.

- Availability of transport, labour in cases of construction work, fuel, power, stationery equipment’s, office machines and sanitary facilities for the staff etc.

- estimated initial operating and overhead costs for a smooth implementation and continuous operation of the credit and saving activities and how the whole activity can be financed.

Technical feasibility study

It will show item by item how the tech required can be met e.g.

- How to make the society qualify for participation in the saving scheme e.g. implementation of mt. system if not already carried out.

- through reconstruction of office premises or building of new offices and the cost involved

- where and how to employ qualified staff for the banking society

- where and how to obtain necessary office machines , equipment’s, stationeries and other accessories involved

- how to satisfy the members need for banking services at the lowest cost

Economic feasibility study

As a result of the above its necessary that an economic appraisal in the farm of study of the present situation in the Sacco is accrued our in order to establish satisfactory savings facilities to the members.

Hence the following ought to be worked out before an implementation plan is prepared:-

- the savings capacity-savings capacity ought to be known as this will certainly determine the members need services and also number of staffs and opening hours at each service place

- size of the society- the membership turnover/ number of members to be served as far as its concerned should be known in order to show size of Saccos together with experience gained from already established saving scheme giving the bas for staff requirements, the size of the office premises , equipment’s, accessories and stationery need.

- How frequently should the service be given

It could be daily, weekly, fortnight or monthly in each one of the centres. what are the distances from the sacco office to be members and how are the road conditions should be service be rendered through a mobile bank or permanent offices

Should be members personal a/c be centred or decentralized

Should they be maintained manually or should they be mechanized?

What security arrangements are to made for money in custody or in transition e.g. should they be reinforcement in report of storeroom and insurance cover required.

which categories e.g. of people who are in need of training , education and which stage e.g. knowledge about the scheme should be reached by each category and where can such education be obtained (locally, co-op college of Kenya or other education centres).

Results of the study

Based upon the answers to be above question together with the gained e.g. filed of scene it is possible to determine.

- organisational set up of the sacco activity and prepare an implementations

- initial cost of establishing a sacco in the area

- the ruining and overhead cost for longer period of time e.g. 3-5 years plan

- whether the banking activity will be a viable one or not

Savings implementation plan

General information

To enable a smooth implementation of the savings scheme in a Sacco it’s necessary that certain conditions laid down in the 5th year devt plan. Of the Sacco should be fulfilled of the economic viability must be proved through the members transaction system must be updated and the records maintained before the actual savings scheme is implemented.

The local conditions as far as the devt of various systems must also be considers as in the case with the 5th year devt plan before it gives a rough idea as to when saving scheme should be implemented in a certain area.

Before implementing a Sacco which offers the above services to members it will be important to workout proper plan of operation

The following implementation plan for the savings scheme in Sacco will serve as a guided

- planning and preparation

- implementation of the sacco

- consolidation of the centre

ACQUISITION OF LOAN FUNDS

Loan application and handling procedures

Loan application procedure by a society

Whenever a society wants to give out loans to its members and it has no enough funds, it can borrow from co-op bank.

To get funds from the co-op bank of Kenya the society will fill 5 application farms, one copy is sent to the manager of co-op bank and the other fair (4) copies are sent to the district co-op officers.

At the district co-op office, they are scrutinized and forwarded sent to the district loan committee for that particular district.

The loan committee is composed of:-

- District agricultural officer

- Branch manager

- Representative of the district co-op union

As soon as the district loan committee has approved the loan district co-op office will distribute the farms as follows:-

- One copy to the co-op bank of Kenya

- One copy to the commissioner of co-op debt

- The other copy to the office files.

- One copy to the district office files

Details to be filled in the application forms

- name of the society and its address

- amount in figures and the loan purpose

- Repayment –indicate frequency of repayment which will be made taking into consideration when payments to members are normally made during the year and the size of recovery of member’s loans which will be expected.

- Proposed withdraw schedules- indicates the amount to be withdrawn and approximate date for withdrawals. this will be in conjunction with members expected withdrawals, such information can be detained from the members individual applications

- date of registration and the total shares in the co-op bank of Kenya

- assets and liabilities –these figures are used for assessing the validity of the society

- Total investments-specify have the total investments is to be financed

- Details of security –the details of security offered shall be indicated.

Documents to be closed in support of the application

- Extract from the minutes showing the resolution passed by the committee certified by the chairman and the manager.

- Extracts from the minutes showing the unions/societies max borrowing power as decided by the last general meeting certified by the chairman and the manager.

- a statement signed by the chairman and the manager revealing the total amounts of loans overdraft already granted to the society including loans overdraft granted but Act yet utilised.

- one copy of audited final a/cu and the balance sheet

- the trial balance and the budget

- Specified report showing the profitability of the planned investments.

- A list of the societies to allocated funds together with a report on credit activities for prevails loans signed by the manager and credit secretary.

The application shall be dated and signed by the society officials who are the signatories on the reversed side of the application form.

The DCO shall after scrutinizing give his comments

The DCO gives the recommendation/discommendation of the districts loan committee

Funds from the union banking section

Another source of funds for lending to members, comes from the union section

Such funds are usually the members own savings

When applying for funds from the union, the society will normally make its application direct to the union

The union will then allocate loans from the societies on the basis of either the individual society turnover or its member’s savings balance.

Usually the UBS policy that when granted loans thereby leaving a balance of 20% for the members to come and withdraw for other needs

This method encourages societies to save regularly and also prompt loan repayment.

When the society turnover method then the CPCS upper loan limit for calculation are applied i.e. Short term, medium term, phase I and phase II

Before a society can use its own funds for leading purposes, it must be authorized by the district officer

The essential information you be filled in the application farm includes

- The total amount to lend out

- In which period and for which credit.

Filling of the application form by a members

Loan application by members from their society

Members who want to apply for loan will get a loan application form from the society

A society clerk may assist the member to fill in the loan application form

The following stationery and equipment must be available:-

- Loan packages

- Members proceeds

- Computation table for upper loan limit

- Loan application form

Filling in the loan application

- Fill in the name of the society, address, age and members number of the applicant

The number of application is important to note in order to ensure the members are considered in the same order as they come to apply.

The number should be consecutive based on the loan purpose and loan amounts and shall unless normal circumstances be filled in by the members.

Considering the loan purpose stipulates the number of areas to be invested into the month when the loan will be needed the amount in kind in cash and totals.

All these shall be in accordance to the loan packages

The society field officers or reps will visit the applicant farm, lack of the land , access its size and possibilities of increased yields as well as quality production together to the applicant he will work out a crop package that will give the farmer an optimal return on his investments

He shall also advice the farmer on the most productive methods ,what seed and fertilizers and spreading chemicals to use for various crops as well as when and how to use those inputs.

Finally the society will assist the farmer to fill in the particulars of the application farm

- If some of the crops are to be produced in a leased land the number of acres and the name of the owner shall add be put in the application.

The value of the crop proceeds shall be filed in these values shall have been calculated beforehand in the crop proceeds farm.

- The society representative will discuss the security part with the member and fill in the securing crop the acreage and the number of incase of milk.

In case loan applied form is ksh. 30,000 and above the security part in this section shall be completed .the society committee shall discuss the value

Guarantor qualification

The guarantor’s qualifications are similar to those of loan application (borrowers qualified)

NB: Guarantors production should cover the total amount which is guaranteed plus possible own loans.

Loan Agreement

A loan agreement is an unrevokable order form which shall be filled in at the same time as the application.

After the loan granting meeting the general managers shall be seen to it that the loan agreement are ready for all successful applicants and shall be signed by the borrowers immediately after the loan granting meeting.

Loans which are given in kind, a delivery order has to be filled I and signed by the borrowers

The loan agreement form shall be filled in as follows:-

- A/C no which is comprehensive containing the society activity and the member’s number.

- The lenders name- this is the name of the tender in block letters

- The name of the borrowers in block letters

- Borrowers age

- Borrowers address including home village, location and society

- Loan amount inwards and figures

- Loan purpose which shall be the same as the loan application form

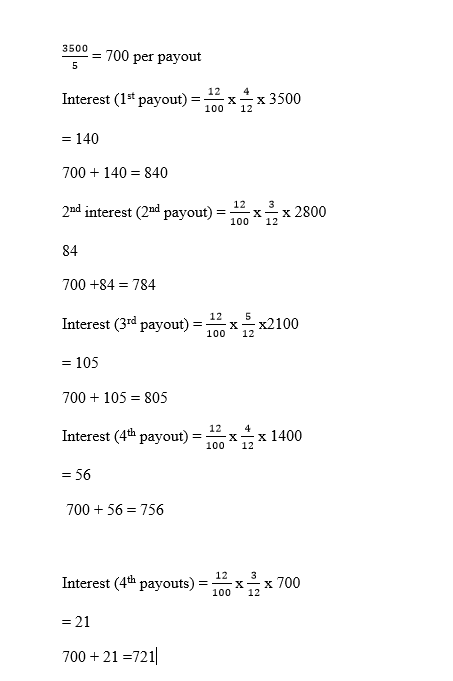

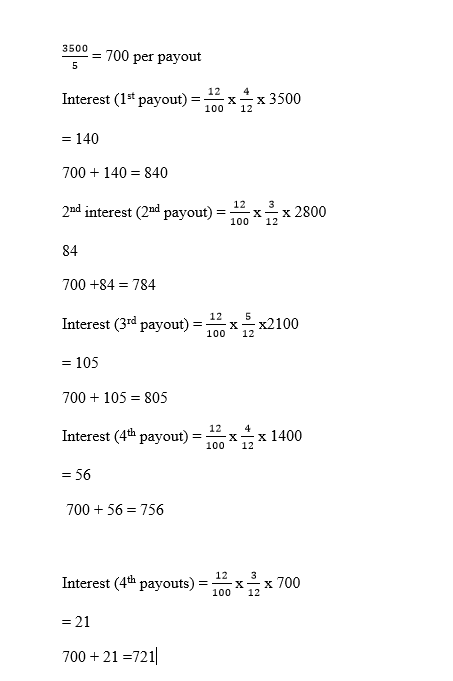

- Conditions of loan repayments (they should be divided into monthly or quarterly installments depending on the type of loans.

- On the type of loans the loan installment will be deducted from the member’s proceeds until loan is fully repaid.

- The dates on which the 1st and final installment falls due from due should be indicated.

- The rate of interest- it should be stated and the date from which it shall be charged

- Transfer to this part shall be filled in only when the loans to be paid in cash to the borrowers and credited to the member’s savings a/c. The a/c no, the amount and the date when the 1st withdrawal will take place shall be indicated

- Quote the guarantors name and the member’s number in block letters from the loan application

- Witness -the witness signature shall be followed by their names in block letters ad addresses

NB: after the preparation the loan agreement shall be filled activity wise in member number order

This facilities easy tracing of the respective loan agreement.

The society shall in good time order for the revenue stamp is needed when the loan agreement is being signed.

The language used when explaining the agreement shall be indicated

The borrower’s confirmation as well as the guarantor’s pledges and the witness as certificate shall also be completed.

Roles of borrowers, guarantors and witnesses

Loan agreement shall be signed by four different parties namely,

- Lender /Society

- Borrower

- Guarantors e.g. two friends and must be society member’s

- Witness e.g. 2 society members.

Name of these categories can act as dual capacity on the same agreement form.

This means for instance a guarantor is not allowed to act as a witness

It also means that a society chairman/banking manager cannot appear as a guarantor in a loan agreement

They shall not sign on behalf of a society in agreement is established with a member’s the society is bound to:-

Roles of a society

- lend during a specified period of time a certain amount of money for a certain purpose to a certain person against a stated security

Roles of borrowers

The borrower shall be a member of the society and when he signs a loan agreement he is legally undertaking to/ entitled to:-

- Borrow a certain amount of money for a certain purpose from the society

- Repay the loan within a stipulated period of time the interest at a specified rate

- Deliver his produce for making through the society

- Care for then property security or item interested in with the assistance of the loan and not sell without the consent of the society such items/ properties until the loan is fully repaid.

- Adhere to all of the conditions concerning the loan whereby the borrower has a right to withdraw his loan and of course somebody else in writing to make withdrawals of this loan.

The guarantors are jointly and severally responsible for the repayment of the loan should the borrower default

In case the borrower refuses to pay an installment which has fallen due the society can ask the guarantor to pay the loan.

Scrutiny of loan documents

All loans application/ agreements after the approval and having been completed shall be submitted to the credit section for final scrutiny.

The society banking manager/ sec manager shall implement a system for control of dispatched documents.

For this purpose, use of research for valuable documents will be dispatched

The receipt is filled in duplicate and taken to the credit section together with the filer containing the loan application and agreements.

Upon receipts of the application ad loan agreement the credit manager will sign the above receipts and file the duplicate.

While the original is taken to the banking manager/ sec manager where it will be kept in a file proving that the loan documents are now with the credit section

The society credit officer is responsible for seeing to it that a register for loan agreement is opened.

With society credit officer shall see to it that the loan agreements are thoroughly scrutinized.

Main points to observe in the loan agreement

- All signatures appear in the correct place. Whereby the borrower shall sign across a revenue stamp.

- that the witness are not biased and nobody is supposed to SIGN IN DUAL CAPACITY

- that the loan amount is the same as the approved amount in THE APPLICATION

- That the loan purpose is the same as in the application

- That the terms of the loan payment fall written with limitations and reasonable in relating to the loan purpose.

- the security is appropriate

- the guarantors are the same as mentioned in the loan application

NB : Any irregularities are the same as mentioned in the loan application available on the application or any other information that is missing but known by the society credit officer can completed at the society credit system.

Loan agreement register

A register of loan agreement shall be maintained by the society credit section

Entries into this register hall be made from already scrutinized agreement

Separate register shall be kept on the basis of the type of credit

The fallowing information will be filled in extracted from the loan agreements into the loan agreements register.

- the society name and the date ,year, page no, member no, members name as in the loan agreement

- Amount of loan, type, final due date as in the loan agreement, security-indicates e.g. crop proceeds.

- The signature of the person filling in the loan agreement

- Date of filling –state the date in which the agreement has been finally filled in the society

- Remarks-this column may be used when the agreement is return to members for correction or completion.

Loan agreement register

Charge as security

According to the credit policy all loans of ksh.30,000 and above are to be secured by a charge of the land owned by the loaned.

Where land as security is not suitable other properties can be provided /used.

Various terms used in charge procedure

- Change –it’s a farm of security provided for payment of loan

- Charge-this is the lender or the proprietor of the charge i.e. the society

- Charges-this is proprietor of charged land i.e. the owner of the land, loanee or borrower.

- proprietor-in relation to a charge of land ,the person named in the register of the land

- land certificate-it’s a certificate issued by the land register and it’s a sufficient proof for the properties ownership

The charge I to have the 1st priority and the value of their land charge must exceed the total amount the charger is borrowing from the society.

In case where the property of the loanee has already been given as security from another loan the society an in special cases accept a 2nd priority charge a security for the loan.

In such a case the value of the property charged will have to be sufficient to cover the second loan borrowed.

A written consent of 1st charge will have to be obtained

When the society estimates the value of the land the fall points should be taken into consideration

- the size of the land

- any size of the land

- Quality of the land i.e. is it suitable for cultivation, is there enough water, are there roads close to the land, is the land bushy or cleared, is there any other fact that might influence the market value of the land e.g. electricity.

- conditions of the permanent buildings

- Estimated value of any permamment crop e.g. coffee, tea, pyrethrum etc.

The comet considers the above information to access the value of the land according to current price of the land of particular area.

The security of charge is considered sufficient if the loan applied for the does not exceed 80% of the estimated value of charge property

E.g. the value of property is estimated as ksh.40,000. The amount applied for is shs. 30,000

- calculate the amount to be granted

- will the loan be granted or not?

Solution

x 40,000 = 32,000

The loan will be granted:

In this case the maximum value of security offered will be 80% of the property hence the loan applied for falls within the value of security offered and the loan may be granted provided that no obstacles are faced when registering the charge.

Procedure to follow when one wants land as security

The loan handling procedure for a loan secured by a charge of land will be as follows

- The potential loanee applies to the society for a loan

- the society loan conte considers the application and especially the value of the property belonging to the applicant has to be scrutinized if the loan is ksh.30,000 and above.

- If the applicant is granted a loan more than kshs.30,000 and above the society demands a change over his land in addition to the normal security of crop proceeds and guarantors

- Then loan agreement is to be filled in

- The loan farmer is asked to arrange for the charge and the 1st step in this exercise is to send an application to the divisions land control bond for its consent to charge the land.

- If the land control approves the application it issues a letter of consent which is returned to the applicant.

- The loanee brings the letter of consent and the copy of application together with his land certificate to society.

- The society credit officer files the land certificate together with the loan agreement and the application and issues a receipt to the lonee for the document.

- The society will assist the loanee to register a charge

- Once the charge has been registered and the document has been returned to the society it should be ascertained that

- The charged property is sufficiently insured

- The insurance co. has notified the society of the same.

- Thereafter the loan can be released to the loanee.

Application for consent

Consent is given only when the land control bond ensures that land is used for other purposed other than agriculture, and that it is not transferred to others who do not intend to develop the land properly.

It is necessary to follow the rules in the land control act so that the charges become security for loans.

Application is made in duplicate in form1 and forwarded to the land control bond.

If the land control bond gives its consent to the transaction if issues a letter of consent.

The loanee brings the documents from the control bond to the society in order to register a charge.

Registration of a charge

When registering a charge the following documents and stationeries will be used

- Letter of consent

- The land certificate

- The charge form (R.l.9) –filled in triplicate

- Application for official search (R.l.26)

- Application for registration

When all the documents are ready the members are assisted by the loan officers to prepare for the registration of charge.

The form R.l.9 (the charge form) will be filled in triplicate and this together the application official search will be submitted to the district land registrar.

The land district registrar returns the duplicate and triplicate and keeps original on his own file .

The charge has to to be signed both by the loanee and the charge

The loanee must be informed alt the contents on a charge before signing it

They should be informed told of the implications that.

- If default is made on payment of the principle sum or of any interest or any other periodical payment or any part therefore or in the performance or observation of any agreement experienced in any charge and continues for one month the charge may serve on the charge notice in writing to pay the money owing or to perfom and observe an agreement or as the case may be.

- If the charge (loanee) does both comply within 3 months form the date of serves the charge May

- Appoint a receiver of the income of the charged property

- Sell the charged property

If the charge who has appointed a receiver may not exercise the power of sales unless the charge fails to comply them in 3 months of the date of service.

NB a loan secured by a charge should not be released to the loanee before the fails is carried out

- The charge is properly registered by the district land registrar and returned to the society

- The certificate of official search is received from the district land registrar.

- The land certificate must be deposited in the society

- Valid insurance cover is shown and the insurance company informed about the interest of the society

- A loan agreement has to be signed by the loanee and the guarantor.

Lodgment of loan document’s

Loan document in many ways are as variable as money

In case of default it’s through the different documents that the society will be able to recover the loans

In order to protect this variables its necessary to have a system for registration and safekeeping of this document’s

The entire document’s involved are:-

- Land certificate

- Loan application

- Charge form

- Insurance policy

- Letter of consent

- Loan agreement

All documents to be registered and filled should indicate the society, the type of credit and re and the member’s on top of the 1st page.

The mentioned documents are registered and stored on a lodgment journal which printed in a set of 3 copies each, whereby:-

- The 1st copy has lodgment journal on the first side

- The 2nd copy has the loanees receipts

- The 3rd copy has lodgment envelope

All these 3 copies are filled simultaneously down the double line using carbon papers

The credit manager should check in advance the insurance register and in case there is any insurance policy that is about to expire, he should take the necessary steps to find out whether it has been renewed or not.

In case there is same premium which has not been paid the society can pay on behalf of the member’s and debt the amount to his loan a/c.

All the documents therefore related to the loan shall be filed in the lodgment envelope

The lodgment envelopes are then placed in member ordered in a lockable cupboard /carbon to be kept in a strong room.

Whenever somebody wants to remove something from the envelope, he has to write on the envelopes what he has removed and sign for it

On return the person shall write the date of replacement and sign for this

Purpose of lodgment journal

- To keep all necessary information of the loanee in one document only

- To keep all necessary information of security of the loan in one document only

- It forms the main register where special information such as an insurance expiry register is extracted

- It is used by audition while checking whether registration has been carried out properly

Discharge of a charge

When loan is fully repaid the charge will be discharged

There is a discharging fee collected from the loanee and an official receipt is issued

Some of these fees includes: – i) Stamp duty ii) registration fees

The following stationery will be used when discharging a charge

- Discharge over form (R.l. 10)

- Application for registration

The society submits to the district land registrar an application for registration while the society retains a copy.

When the loan is fully repaid the back side of the lodgment journal shall be used for notification of what has happened to the various documents securing the loans.

It is up to the loanee to decide whether the charge can be discharged or kept in force for later use his decision shall be noted on the receipt

There are several cancellation which have to be carried out once the loan if fully paid.

- Cancellation of the insurance register by removing the expired card from the register

A letter to the insurance company has to be sent to inform them that the interest of the society on the property is terminated

- The loan agreement has to be stamped “PAID and returned to the filling envelope.

- The land title dead must be returned to the owner. This is where the loaness should be informed either by person or sent in person and be told to come to the society to collect the land title deed and he should sign for it.

- The charge can be in same cases be used as security for a new loan

- The lodgment envelope is removed from the current loans and placed to paid loans lodgment envelope in the society

- The lodgment journal is removed from the current files and is transferred to the society credit stations

NB Any valuable document given to the owner or cancelled, a receipt is issued to the owner.

Formalization of debts

Formalization-refers to the process of either recovering or securing of all overdue debts

The ultimate aim of this procedure is to clear the books of the union /societies of all overdue debts whether they are recoverable or not.

All debts due to a union or a society which have fallen due have not been repaid are termed as overdue debts

There are mainly two types of debts to a society namely:-

Members and non-member’s which includes committee, staff members of other affiliated societies are

- Members debts (unions)

The society should be requested to pay in cash and if the society is unable to pay cash it should sign an irrevocable letter of instruction to the source of crop proceeds authenticating payments to the union.

In case a society denies owning any debt to the union the matter should be referred to the necessary authorities as a dispute

2. Nonmember’s debts

If a debtor is a member of an affiliated society, and he is active in that society, the union should send a letter to the society and request that the debt be recovered on its behalf from the member’s crop proceeds

Incase it’s an employee /staff their salaries should be attached to recover the debts

Incase all the efforts are failed then such a debt should be recommended to the union AGM for write off.

The formalization of debt should be done on the fail guidelines

- Reconciliation-this is where by the posting of data ledgers must not be brought up to date. This is to ascertain the corrections in the individuals member’s a/c and ensure that they are reconciled in the control a/c

- Listing of cover overdue debts

After the individual a/c have been reconciled the balance on them should be considered as the correct balance. Then the secretary manager should prepare a list of overdue debts showing

- The members name and no

- Action taken to recover the debt

- Amounts used

- Whether active or inactive.

- Recovery this requires all the debts to pay their debts in cash and if a member cannot repay the debt in cash, the debt shall be recovered in the subsequent payout.

If the debt is too large the members will be required to fill a loan agreement with the society for regular loan repayment not exceeding 12 months

If a member is unwilling i.e. disputing the debt with matter should be referred to the to the co-op tribunal as a dispute

If there are no supporting document’s then the debt can be recommended for write off in the next AGM

If a member has left the area of operation of the society and cannot be traced, the debts should be offset against the shares in the society

In case a member is salaried person a bank order limiting money to the society should also be signed by a particular member

In case of staff, salary deductions should be made until the whole debt is recovered

If the staffs are also members then deductions from crop proceeds should be made.

If a member of the staff uses unfair means to obtain the debt salary reductions of up to 50% should be made

TOPIC 6:

Loan withdrawal and recording procedures

How loans are withdrawn

There are 3 main ways of loan withdrawal

- Loan withdrawal in kind

- Loan withdrawal in cash

- Loan withdrawal credited to members savings account

- Loan withdrawal in kind

In case the loan agreement provides for loan in kind , a delivery order has to be filled in and signed by the loanee at the same time as the loan agreement form

The duplicate of delivery order will be given to the loanee who then can collect required goods from the society or union store or from any other dealer recognized by the society. The original is retained by a society and the order is valid for a period of 3 months from the date of issue.

When the loanee or somebody authorized by the loanee collects the goods, the suppliers delivery note or invoice is signed by the person who collects the goods. The serial no of the order shall be quoted by the supplier in the delivery note or in the invoice.

An outside supplier will send the invoice to the society where its particulars will be checked against the original of the order and if found correct, a cheque for the amount will be issued to supplier. The society cash journal for that day, a payment will be prepared and an entry made in the interim account of member’s loan in the ledger.

At the same time the entry in member’s loan account shall be made from the invoice received from the supplier

This operation shall be repeated for every loan in kind.

Document used when withdrawing loan in kind

- Loan sales journal- The credit manager of the society should ensure that all summaries of loan withdrawals in kind are properly scrutinized and reconciled the relevant invoices.

The loan clerk will carry out the recording of the transactions of the member’s loan account as follows:-

- Fill in the member’s number from the loan sales journal

- Indicate the date in the loan sales journal

- In the details column indicate the invoice number

- The previous balance will be the same as the debit balance on the previous line as the members loan account.

- Entre the amount shown on the loan sales journal as withdrawn in the debit column

- Calculate and enter the new balance in the balances column (i.e. previous balance + debit entry=balance)

- Tick off the line used in the journal and replace the member’s loan account with the ledger card box

The above routine will be repeated for all members who appear in the loan sales journal

- Loan withdrawal in cash

It can be done in two ways (i) from the UBS (ii) from the society

The loan being withdrawn in cash should be paid to the member when he/she is going to use it to avoid the risk of misuse.

The credit secretary should be responsible for ensuring that sufficient funds for member’s loan withdrawal are requested for in due time

A day should be arranged when all the loanees should come to collect the money

A cheque shall be issued and signed by the union signatories

A list of all loanees eligible for loan in cash shall be attached to support the cheque

The union cashier will collect the money from the bank and hand it over to those responsible for payment to the loanee

The following stationaries shall be used during the loan repayment

- The tellers cash report

- Loan withdrawal voucher /journals

- List of member’s eligible for loan in cash

- Summary of the member’s loan withdrawal

- Carbon papers

Loan withdrawal voucher /journal

It’s composed of 3 pages

The 1st page consist of withdrawal vouchers- These are torn off and given to the members when they receive the money

The 2nd page is the loan withdrawal journal- It’s the union credit section copy

The 3rd page is also a withdrawal journal to the accounts section.

Contents of loan withdrawal voucher

- Name of the society in full

- Official stamp of the society

- Member’s name as contained in the loan agreement

- Date of withdrawals

- Member’s loan as per loan agreement

- Loan a/c number as per the loan agreement

- Amount of loan withdrawn in cash

Contents of loan withdrawal journals

Information (i) – (vii) in the voucher is carbonized and all the information on the voucher (except the society stamp) will be copied into the journal when the voucher is filled in

- The date from which the journal is used to the last date shown at the bottom of the journal

- The loan journal page used to post the withdrawal into the member’s loan a/c

- The members signature or thumb print

- Total withdrawals made on the withdrawals voucher

- Total withdrawals carried forward from the withdrawal voucher

- Addition of number xi and xii to get the balance carried forward

NB the 3rd copy will have similar information as the 2nd copy.

- Loan withdrawal credited to members savings account

The cash portion of a member’s loan shall always be credited to the member’s savings account in accordance with the loan agreement. This is done in case the society is operating both on credit and the savings scheme

The union credit secretary shall see to it that this is done in due time for member’s appropriate use of their loans.

Stationaries and equipment used in number (iii)

- Loan agreement duly completed and scrutinized

- Loan withdrawal credited to the members savings account

- Summary of member’s loan withdrawal

The loan clerk responsible for recording the loan transactions of the society will take the forms of loan withdrawals credited to the member’s savings and insert a carbon paper in between the original and duplicate of the set.

The loan clerk will fill in the form with the following particulars;

- The society name

- Society registration number

- The amount to be credited to the member’s savings account according to member’s instructions

- The date of transaction

- Activity number

- Page number (which is reprinted)

- Account number i.e. the savings account number which the loan amount shall be credited to

- name of the member’s concerned

- tick the line used

- page number of the journal used

- page number of the savings journal used

- Total withdrawals credited to the member’s savings a/c.

Opening of member’s loan account

After the loan granting meeting, all those members who have been granted loans are supposed to sign loan agreements

The loan agreement forms are sent to the union private sections where the credit secretary after a proper scrutiny of both the loan application forms and the loan agreement forms asks the loan clerk to open the member’s loan account

The opening of the members loan account should be done actively wise

The following procedure should be followed when opening the account

- Name of the society as shown in the loan agreement form

- Member’s name as shown in the loan agreement form

- The name of the activity where the member comes from – This can be a coffee factory, milk collection center or center to which the member deliver his produce

- The total amount of loan granted as shown in the loan agreement form

- The final date by which the member’ has to finish the loan repayment as shown in the loan agreement form

- The members number as shown in the loan agreement form

- Number of the activity as given by the society

- The co-op society number i.e. the society registration number

- The amount of installments to be deducted –this is the principal amount + interest

- The date or year when the 1st withdrawal will take place

The detail should be extracted from withdrawal documents e.g. loan withdrawal journals

- The balance before the present transaction if any

- The amount of loan withdrawn by an individual is posted in the debit column and any other charges such as ledger fees and interest on loans

- Credit all loan repayments

The balance is equal to the previous balance + debit balance-credit balance. The number of months from the latest repayments or loan withdrawals

- Amount of interest charged.

- Amount of loan which is overdue and its calculated by deducting the actual installments

Installments –deductions= overdue loans

NB the members loan account shall be used throughout the loan period to take care of the loan repayment, interest on loans and any other loan charges.

Preparation of the loan granting meeting

The society chairman may remind his committee and other participants of the meeting that

- All the information contained in the member’s application as well as any other information about the members shall not be disclosed to persons outside the society committee.

- The regulation of credit policy shall be adhered to when considering the application

- Committee members shall be guided by their knowledge of the applicants and before taking a decision on application they shall discuss the following questions

- Will the loan assist the farmer to reach a high production and thereby a higher net income?