ROLE OF PLANNING

In Chapter 1, the four basic functions of management process were identified as planning, organising, leading and controlling. It could be argued that planning is the most important of these functions as everything else flows from it. Planning takes place in all organisations either formally or informally. It is important that organisations know where their future lies and that they have planned for it. Planning is future oriented and involves selecting from a number of possible courses of actions. The rapid rate of change that faces all firms makes planning more difficult but also more important.

Definitions

A plan is a statement of action to be undertaken by the organisation aimed at helping achieve its objectives.

Planning is defined as “The establishment of objectives, and the formulation, evaluation and selection of policies, strategies, tactics and action required to achieve them” (Foulks & Lynch, 1999).

Planning and control are closely linked, as a plan is effectively a road map that tells everyone in the organisation where they are going and control ensures that they get there.

LEVELS OF PLANNING

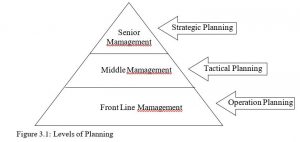

In general there are three levels of planning within organisations as shown in Figure 3.1.

Strategic Planning

Strategic planning is concerned with determining the major goals and mission of an organisation and crafting a strategy to achieve them. Strategic planning is normally carried out at the senior management level. A strategic plan is a long-term plan that will stretch from three to five years.

All other planning in an organisation is derived from the strategic plans.

Tactical Planning

Tactical planning takes place at the middle management level and is concerned with the various component parts of the organisation. A tactical plan is normally a medium term plan covering a period of up to 1 year. Tactical plans will be focused on achieving the overall objectives of the organisation.

Operational Planning

Operational planning is concerned with the short-term, day-to-day functions of the organisation. It is concerned with achieving the operational targets set out in the tactical plans. Operational planning is normally undertaken by front line managers and supervisors within the different functions of the business including sales, production, human resources and finance.

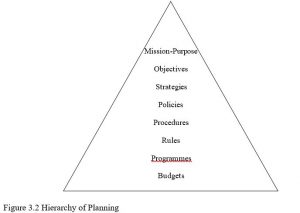

HIERARCHY OF PLANNING

Organisations typically use a wide variety of plans to assist in their planning process. Weihrich and Koontz (1993) state that there are eight different types of plans, which form a hierarchy as shown in Figure 7.2.

Mission or Purpose

The mission or purpose is set out in a mission statement that is used to communicate the strategic vision through the organisation. A mission statement will set out how to make the firm distinctive in the eyes of its employees, customers and suppliers. A mission statement will generally include a description of the company’s basic product or service and its target market.

Goals and Objectives

Organisational goals set out the long-term targets that have to be achieved if the hopes in the mission statement are to be attained. Objectives set out in the medium-term outline how these goals are to be achieved. Sample goals and objectives might include:

Goal: To become Africa’s number one low cost airline with five years.

Objectives: To become market leader on Kenyan and Ugandan routes within two years, to increase market share on Kenyan to Ugandan routes by 10% per year, to open 6 new routes per year and to increase seat occupancy by 3% per year.

It is possible for objectives/goals to be in direct conflict with each other. For example, the organisation might have set a goal to reduce costs and at the same time improve product/service quality. The basic conflict in this example is that improving product or service quality can lead to increased costs and reducing costs can have a negative effect on quality. The organisation in this example must strike a balance between the two or drop one.

Strategies

The fundamental plans that an organisation devises in order to achieve its goals and objectives are called strategies. Strategies are the set of activities identified to achieve goals and objectives. Strategies should take account of the company’s strengths and weaknesses and the opportunities and threats that exist in the external market.

A company’s strategy represents the management’s answer to such issues as whether to concentrate on a single business or build a diversified group of businesses, whether to cater for a broad range of customers or concentrate on a niche market, whether to develop a narrow or broad product line and whether to pursue competitive advantage through low cost or product superiority.

Policies

Policies provide a framework to assist managers in their decision-making. Policies tend to limit an area within which a decision can be made and ensure that the decision will be consistent with and contribute to the overall organisational objectives.

Policies can be in two forms, namely express or implied. An express policy is a written or verbal statement, which guides managers in their decision-making. For example personnel may state an organisation is an equal opportunities employer. An implied policy is inferred from looking at the organisation’s behaviour and actions. Sometimes an organisation’s expressed and implied policies may conflict or contradict each other, with the organisation pursuing an expressed policy openly yet privately applying an implied policy.

Procedures

Procedures are used to standardise activities ensuring consistency. They provide a framework to assist management in decision-making. Procedures are set out for the different functions. For example there might be purchasing procedures, hiring procedures, procedures to handle bad debts, customer complaints procedures etc.

Procedures exist at all levels in the organisation but tend to proliferate at lower levels often as a means of control. Weihrich and Koontz (1993) argue that one of the reasons for the widespread use of procedures at lower levels is that routine jobs can often be completed more efficiently when management details the best way to carry them out.

Well-established procedures are commonly termed ‘standard operating procedures’. These are procedures that the organisation uses in a routine manner.

Rules

Rules are statements that either prohibit or prescribe certain actions by clearly specifying what employees can and cannot do. Examples of rules would include “No Smoking”, “Safety helmets must be worn on the building site” and “No cheques accepted without cheque card”. Unlike procedures rules allow no discretion in their application.

Programmes

Programmes provide a link between strategy and execution. Programmes are a method by which middle management can translate organisational strategy into activities to meet its goals and objectives. For example an IT manager may develop a computer replacement program to reduce maintenance costs of obsolete equipment. The introduction of a program within an organisation may lead to the development of a number of supporting programmes.

Budgets

A budget is a numerical expression of a plan, which deals with future allocation and utilisation of resources over a given period of time. Budgets are normally expressed in financial terms, person hours, productivity or any other measurable unit.

Budgeting is an important planning tool in many businesses. Financial budgets are developed in conjunction with a programme and they set out the financial resources available to achieve the programme’s objectives.

A budget also serves as an important control mechanism. One of the advantages of a budget is that it forces people to plan in a precise way.

THE PROCESS OF PLANNING

To gain an understanding of the planning process we will look at one type of planning (Strategic planning) and describe the steps involved.

Strategic planning involves the following stages:

- Developing a mission statement

- Setting objectives

- Analysing the company’s internal and external environment

- Developing plans

- Implementation of plans

- Evaluating performance

Developing a Mission Statement

This stage involves an analysis of the organisation’s current position and an investigation of the external environment, in order to establish where the company is and where it is headed. It also involves identifying gaps in human (skills) and materials resources that need to be filled. The purpose is to provide a long-term direction on what the company is trying to become.

Setting Objectives

This stage involves translating the strategic vision or mission into specific performance targets to be achieved. Objectives should be Specific, Measurable, Achievable, Realistic and Time-bound (S.M.A.R.T)

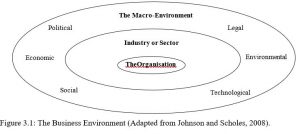

Analyse the Company’s Internal and External Environment

Before preparing a strategy, an organisation needs to carry out an analysis of both its internal and external environment. The business environment is made up of a number of different layers as shown in Figure 3.1. These layers include the macro-environment and the industry or sector in which it operates.

Macro-Environment

The Macro-Environment: This “general” layer consists of broad environmental factors that impact almost all organisations. It is important to build up an understanding of how changes in the macro-environment are likely to impact on individual organisations. While the firm may have little control over these factors it must be in a position to deal with these effects whether they represent a threat or an opportunity for the firm. The PESTEL framework can be used to identify how future trends in the political, economic, social, technological, environmental and legal environments might impact on organisations.

PESTEL ANALYSIS

- Political Factors: The political and legal factors are shaped by the activities of governments at both national and international levels. On a national level, a government

can affect business through its policies in relation to industrial development, and in particular by the tax incentives, capital grants and expansion schemes made available. On an international level, the political environment influences business through policies in relation to international trade and deregulation.

- Economic Factors: The economic environment affects the purchasing power of a given market and therefore will affect the level of demand for a firm’s products and services.

- Societal Factors: The culture of a society in terms of basic beliefs, values and norms within which a firm operates can affect the type of products the society needs and wants. Demographic factors relate to the nature and structure of the population from which the firm’s customer base is chosen. Factors such as population increase or decrease, movement of population, age of the population and education level will all have to be considered when preparing the organisations strategy. Organisations will need to establish what the current and emerging trends are in fashion and lifestyle, what demographic changes are occurring and what the likely impact on the firm’s markets is.

- Technological Factors: The pace of technological change can affect the product service offering available in the marketplace, the methods of production used and the channels of distribution used. Organisations need to determine which emerging technological trends are likely to affect the industry in which they are operating.

- Environmental Factors: The cost-effectiveness of raw materials and energy, and the need for a cleaner environment have a major impact on the type of product and service offerings available and the way in which they are produced. Organisations need to be aware of their environmental responsibilities.

- Legal Factors: There is a wide range of laws that can impact an organisation which include the following:

- Competition law: Unfair competition, below cost selling, regulated industries.

- Employment law: Unfair dismissal, minimum wage, holiday pay, redundancy etc.

- Health and safety: All employers are required by law to protect the safety, health and welfare of their employees.

- Product safety: Laws to protect the consumer.

Industry or Sector:

This is the next layer within the broad general environment. The industry or sector is a group of organisations producing the same products or services. The five forces framework can be useful in understanding how the competitive dynamics within and around an industry are changing.

Porter’s Five Forces Framework

Porter identified five competitive forces that can be used to analyse the intensity of competition within an industry, and the attractiveness and profitability of an industry. By understanding these forces management can develop effective strategies.

Porter’s framework states that competition in an industry is a composite of five competitive forces (see Figure 3.3):

- The threat of new entrants

- The bargaining power of supplier

- The bargaining power of buyers

- The threat of substitute products

- The intensity of rivalry

Each of these forces is now discussed in detail.

THREAT OF NEW ENTRANTS

The threat of new entrants will depend on the extent to which there are barriers to entry. Barriers to entry are factors that need to be overcome by new entrants if they are to compete successfully. Typical barriers include; capital cost of building and equipment, economies of scale, access to supply or distribution channels, customer loyalty, experience, government regulations and differentiation.

BARGAINING POWER OF SUPPLIERS

Whether the suppliers to an industry are a weak or strong competitive force depends on market conditions in the supplier industry and the importance of the item they supply. Supplier-related competitive pressures tend to be minimal whenever the item supplied is a standard commodity available on the open market from a large number of suppliers with ample capacity. Suppliers also tend to have less leverage to bargain over price and other terms of sale when the firm they are supplying is a major customer. Supplier’s power is likely to be high when there are only a few main suppliers of the product or service, or when the costs of switching from one supplier to another are high. Supplier power is also strong if there is the possibility of the supplier competing directly with their buyers (forward integration).

BARGAINING POWER OF BUYERS

The bargaining power of the buyer is strong when some of the following conditions exist:

- Where there are a few dominant buyers and a large number of small suppliers

- Where the number of buyers is small

- If the costs of switching to a competing product or substitute are relatively low

- If the buyer poses a credible threat of backward integration into the business of the supplier

THREAT OF SUBSTITUTES

Firms in one industry are quiet often in close competition with firms in another industry because their products are good substitutes. Substitution reduces demand for a particular class of products as customers switch to the alternatives.

INTENSITY OF RIVALRY

This is normally the strongest of the five competitive forces. In some industries rivalry is centred around price competition, which sometimes results in lowered prices. In other industries rivalry is focused on factors such as performance features, new product innovation, quality, warranties, after-sale service and brand image.

Rivalry intensifies as the number of competitors increase and as competitors become more equal in size. Also rivalry is usually stronger when demand for a product is growing slowly or shrinking.

SWOT Analysis

SWOT is a Strategic planning tool used to assess the Strengths, Weaknesses, Opportunities and Threats of a business. Strengths and weaknesses are internal to the organisation while opportunities and threats are external to the organisation.

STRENGTHS

Strengths are what a company is good at doing or a feature of its operation that gives it a competitive advantage. Strengths can be the skills of the workforce, patented technology, organisational resources, quality products, strong brand names or low manufacturing costs.

WEAKNESSES

Weaknesses are those features of its operations that have a negative impact on its performance and profitability. Weaknesses put companies at a disadvantage and if they are not corrected can make them vulnerable. Weaknesses might include high cost of production, low skilled workforce, outdated products, poor brand image etc.

OPPORTUNITIES

Industry opportunities are an important element in determining a company’s strategy. Industry opportunities relevant to a company are those that provide the best ways of achieving growth in sales and profitability by taking into account the company’s skills and resources.

THREATS

These are factors that have ability to impact negatively on the company. Threats can come from substitute products, increased power of suppliers and buyers, new entrants to the market, increased rivalry within the industry and new competitor products. Threats might also come from new government legalisation, slowdown in economic growth, changes in customer’s tastes or rapid technology change.

Opportunities and threats highlight the need for strategic action. A SWOT analysis can be used to complete a detailed evaluation of a company’s strengths, weaknesses, opportunities and threats, in order to highlight the need for change and to build this into the organisation’s strategy.

Develop Plans

This stage involves developing the plan to achieve the desired objectives. The objectives are the ends and the strategy is the means. The strategic plan will consist of a number of planned actions to address such issues as: how to satisfy customer needs, how to overcome rivals, how to respond to changing market conditions and how to develop specific organisational capabilities. Two important steps in strategic planning are SWOT Analysis and evaluating alternative strategies.

EVALUATING ALTERNATIVE STRATEGIES

The organisation will develop a list of strategic options that will help it achieve its strategic objectives. Options could include expanding into new markets with existing products or launching new products on the existing market of even acquiring a competitor. The company will need to evaluate each of the alternatives and choose the most viable one(s).

Implementation of Plans

This stage involves implementing the strategic plan. The task on management includes such actions as assessing what needs to be done to put the strategy in place, executing it proficiently and achieving good results. Implementing strategy involves developing the capabilities of the organisation, creating a suitable culture and motivating the people to pursue the target objectives. It also involves developing and controlling a budget towards the resources critical to the strategic plan.

Evaluating Performance

This stage involves evaluating performance and initiating corrective adjustments in the direction, objectives, or implementation in light of changing conditions or new opportunities that may arise.

MANAGEMENT BY OBJECTIVES

Management by Objectives (MBO) is an approach which encourages managers and employees to set their own goals within a framework set out by senior management. It is based on the idea that when employees are set specific and challenging goals, accompanied by feedback, they are more likely to be motivated to give their best.

The specific stages of the MBO process are:

- Senior management set long-term goals for the organisation

- Each department within the organisation is assigned specific targets.

- Lower level manager’s objectives and targets are set and agreed with the managers and employees involved.

- Progress towards achieving objectives is constantly monitored and corrective action is taken where necessary.

The management writer Peter Drucker argued in his book “The Process of Management” that MBO was the ideal way of delegating authority in a large organisation.

Benefits of MBO

- It encourages managers to employ a result focus to their planning.

- It can help identify deficiencies in the organisational structure as MBO forces managers to clarify organisational roles and structure.

- Can lead to improved moral and motivation among the managers and employees involved as they have input into the goals that are set.

- Can increase employee commitment to achieving the goals set for them.

- Supports the development of management control and performance measurement.

Weaknesses of MBO

- MBO relies on commitment of all management to succeed and it will fail without top management commitment.

- It can be difficult to set goals for all managers in all circumstances

- Management can become disillusioned if unrealistic and unachievable targets are set for them.

- It can encourage individual achievement at the expense of a team focus.

MANAGEMENT DECISION MAKING

Decision-making is defined as choosing one alternative from several. This definition could be extended to include an identification phase, where problems and opportunities are identified that require decisions to be made. Decision-making is a key task of management, in particular in the context of planning.

Types of Decisions

There are basically two types of decisions:

- Programmed Decision: This is a decision or problem that recurs regularly enough for a decision rule to be developed. The decision rule tells the manager which alternative to select.

- Non-programmed Decision: This is a decision or problem not encountered before where the decision maker cannot rely on previously defined decision rules.

The Decision Making Process

Despite the fact that decisions will be made in different organisational contexts, it is possible to create a model that can be applied to most situations. A six-step model called the Rational Model (Moorhead and Griffin, 1995) is one that can be applied to a variety of decisionmaking situations. The six steps are as follows:

- Stating the goal: The first step is to establish the goal or desired end state against which solution will be measured.

- Identifying the problem: The problem is in effect the difference between the current and the desired or goal state.

- Determining the decision type: The type of decision must be determined. If the decision is a programmed decision, then there should already be policies or rules that can be used. If a non-programmed decision is involved, the decision makers will have to generate solutions as well as evaluate them.

- Choosing an alternative: The alternative chosen will be the one with the highest possible benefits while taking into account the risks involved.

- Implementation: In this phase the chosen alternative will be implemented. The implementation phase will involve planning and communication to ensure that all those affected are aware of the decision and what is required of them.

- Measurement and control: Measurements should be taken to establish the success or otherwise of the implementation. Corrective action should be taken where required.

The Administrative Model of Decision Making

The administrative model describes how decisions are made in difficult situations of uncertainty and ambiguity.

Three important aspects of this model are:

- Bounded rationality – means people have limits or bounds on how rational they can be. Organisations are very complex and have time only to process limited amounts of information to make decisions. Therefore they choose the first solution that satisfies the minimal decision criteria.

- Intuition – entails a quick apprehension of a decision situation based on past experience but without conscious thought. Intuitive decision making is not arbitrary or irrational because it is based on past experience.

- Coalition building – entails forming an informal alliance among managers who support a specific goal. Managers gain support through discussion, negotiation and bargaining.

The administrative model is more realistic than the rational model as it focuses on organisational factors that influence individual decisions.

Group Decision Making

Group decision-making can be a very powerful tool if utilised successfully as it can bring a wide range of knowledge, skills and experiences to a particular problem or situation. However, the disadvantage is that too many strongly held viewpoints can make it difficult to reach consensus. A number of different formats/techniques have been developed to facilitate group-decision making.

- Interactive Groups: A group is brought together face to face with a specific agenda. The discussion group will generate ideas and all ideas will be discussed. A vote is taken to reach consensus on a chosen solution.

- Brainstorming: This is a creative process used to generate ideas involving a group of people who are encouraged to contribute ideas. All ideas are written down without evaluation and are examined in more detail once the brainstorming process is completed.

- Nominal Groups: Group members assess the problem and ideas are generated by the individuals. These ideas are then presented and discussed as a group. Group members then rate ideas individually and the idea with the highest score is chosen.

- Delphi technique: This is a decision making process that was designed to avoid conflict between participants and to prevent any one participant having undue influence on the decision making. A chairman or facilitator asks each participant to fill in a questionnaire. The chairman summarises the replies and sends the summary to each participant for their opinion. The process continues until consensus is reached. The main disadvantage of this technique is its slowness.

Individual versus Group Decision Making

Benefits of Individual Decision Making

The benefits associated with individual decision-making are:

- Speed

- Clear Accountability

- Consistency

Benefits of Group Decision Making

The benefits associated with group decision-making are:

- Wider range of skills and experience used in the decision making process

- Higher quality decisions

- Greater acceptance of the decision made

ORGANISATIONAL CONTROL

Organisational control can be defined as the process through which managers regulate organisational activities to make them consistent with present performance standards.

Management control is designed to provide information on progress against present performance targets. Control is crucial to managers as it enables them to:

- Prevent problems for growing and becoming crises

- Standardise output in terms of quality and quantity

- Carry out performance assessment of employees

- Update plans – actual progress against planned progress

- Protect assets by preventing inefficiency and waste

THE PROCESS THEORY OF CONTROL

The careful design of a management control system can ensure that all employees, work teams and functional departments meet the objectives and targets of the organisation with minimum deviation. The basic activities involved in a control process are:

- Setting Performance Standards

- Performance Measurement

- Corrective Action

Setting Performance Standards

Standards set out what must be achieved in terms of quantity or quality to meet the organisation’s objectives. Performance standards are set at a specific point in an implementation program and will assist managers in gauging the actual performance against the planned performance objectives. Setting performance standards is a key aspect of the planning process at all levels in the organisation. To be effective standards must be measurable so that they can be recorded and monitored.

Performance Measurement

This stage involves measuring or evaluating actual performance against standards. There are various reasons why performance could fall below the standards set out at the planning stage:

- Standards may have been inappropriately set

- Lack of effort by employees or managers in meeting the standards

- Failure to use the resources efficiently

When examining performance results it is normal for management to concentrate on deviations that lie outside the upper and lower limits set.

Corrective Action

The final stage in the control process involves taking action to correct deviations from the standards. In some situations the standards may have to be revised especially if they are based on historical data that is no longer appropriate.

CATEGORIES OF CONTROL SYSTEMS

There are three general categories of control systems:

- Feedforward: These types of controls are implemented before the plan becomes operative and attempt to prevent problems from occurring. It analyses the inputs (e.g. human, materials and financial) to establish if they are adequate in terms of quantity and quality.

- Concurrent: These types of control monitor the process of transformation of inputs to outputs and enable adjustments to be made during the operation of the process. It is normal with these types of controls to have guidelines for dealing with contingencies that may arise.

- Feedback: This type of control monitors the quality and/or quantity of output after the transformation of input has occurred. This enables managers to decide whether to instigate new plans or continue with existing ones. A customer satisfaction survey is an example of this type of control.

The category of control to be used will depend on the stage of operation in which it is to be applied. Feedforward controls would be appropriate before the process commences while concurrent controls would be used during operation and feedback controls after operation.

CHARACTERISTICS OF EFFECTIVE CONTROL SYSTEMS

For an organisational control system to be effective it must be linked to the organisational strategy and be accepted by employees. The information it produces must be accurate and timely. Effective controls display the following characteristics:

- Appropriateness

- Cost Effectiveness

- Acceptability

- Focus on Critical Points and Exceptions

- Flexibility

- Reliability and Validity

- Accessibility and Comprehensibility

Appropriateness

The type of control to be used depends on factors such as the size of the organisation, the area or function to which they are being applied, and the management level that they are designed for. Controls should be aligned with the organisational structure when assigning responsibility for implementing plans and for correcting any deviations. Controls should be geared to provide relevant information only and avoid generating redundant data.

Cost Effectiveness

Control mechanisms should be designed to work in a cost effective way. They control system should save more money than it costs to implement.

Acceptability

Controls should be designed in a way that avoids causing antagonism between management and staff.

Focus on Critical Points and Exceptions

Controls should focus on significant variations and on those points that are important to the overall objectives of the organisation. A small deviation on one point could be more significant than a larger deviation at a different point.

Flexibility

The control mechanism should ideally be flexible to cater for changed circumstances. A budget would be an example of an inflexible control mechanism because of its inability to cater for changed circumstance.

Reliability and Validity

The information supplied by the control mechanism must be dependable and must measure what it claims to measure.

Accessibility and Comprehensibility

Employees should have access to feedback on their performance and should understand how the control process operates. This will make them more likely to get involved in the corrective actions suggested by the control mechanism.

FINANCIAL METHODS OF CONTROL

Financial methods of control include:

- Financial Statements

- Budgetary Control

- Financial Analysis

Financial Statements:

Financial statements are summaries of an organisation’s accounting records and are concerned with three key areas of financial performance: namely liquidity, profitability and general financial health. Financial statements are prepared based on past information and can provide managers with useful information about trends. The main financial statements are:

- Balance Sheets

- Income Statements

- Cash Flow Statements

Budgetary Control

Budgets are the most widely used means of planning and controlling activities at every level of an organisation. Budgets are widely used as they provide a clear standard of performance within a specified time. At regular intervals during the time period addressed by the budget, actual results are compared with budget figures and this allows deviations to be detected and corrected.

In general, budgets are drawn up by middle managers in response to guidelines set by senior management and are then submitted to higher management for approval. Note: Budgets are discussed in more detail in Chapter 11

Financial Analysis

Analysis of a firm’s performance can be undertaken using a number of different forms of financial analysis which include:

- Ratio Analysis

- Break Even Analysis

Ratio Analysis

Ratio analysis can be used by managers and others to evaluate a firm’s past and current performance. Ratio analysis is a useful method of comparing a company’s financial performance against competing firms in the industry (benchmarking). Financial ratios are calculated from information contained in the financial statements.

The four key categories of financial ratios used by companies are:

- Profitability Ratios: These measure the efficiency of a firm in generating profit which is achieved by comparing its sales performance to the assets of the firm.

- Liquidity Ratios: This measures a firm’s ability to pay back its short-term debt.

- Leverage Ratios: These identify the source of an organisations capital.

- Activity Ratios: These measure the efficiency of a firm in using the resources it deploys.

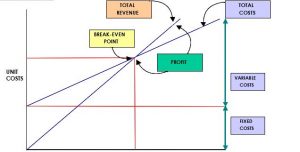

Break Even Analysis

Break-even analysis seeks to identify the point (break even point) at which revenue generated from a given volume of output matches total costs (fixed costs + variable) of that output (See Figure 3.4). Break-even analysis can be used to calculate the output volume necessary to break even or to make a specific level of profit.

Break-even analysis is widely used both in decision-making and control situations as it is reasonable easy to use.

NON-FINANCIAL METHODS OF CONTROL

The main non-financial control methods are:

- Functional Audits

- Quality Control

- Inventory Control

- Production Control

Functional Audits

Functional Audits evaluate the accuracy of accounting and related records. These audits should be comprehensive, systematic, independent and periodic. The audits can be internal or external. Internal audits concentrate the financial health of the company – sales, resources, production etc. Audits may be conducted in each of the functional areas of the business, namely production, marketing, finance and human resource.

External audits, which relies on information that has been made public about competitor firms has the objective of analysing the performance of individual competitors or the industry as a whole.

Quality Control Systems

Quality control relates to the activities employed by a firm to achieve and maintain a certain level of quality for a product, a process or a service. Traditionally quality control was a monitoring activity but is increasingly concerned with identifying and eliminating the root causes of poor quality.

Japanese organisations introduced the concept of quality circles, which involved groups of employees getting together to solve problems in the workplace related to quality.

ISO Standardisation

ISO is an internationally recognised set of quality standards related to design, manufacture supply and servicing of products. Before a company can obtain ISO certification, they must re-examine their operations, document procedures and put a quality systems in place.

Inventory Control

The goal of inventory control is to reduce the cost of handling and storing inventory. The aim is to have adequate inventory at hand but no more than is required. To achieve this aim an inventory control system is used to indicate how much inventory should be bought and at what point it should be reordered. Factors that have to be taken into account include the leadtime involved and the amount of safety stock kept in reserve in case of problems with suppliers. The inventory control system must also decide on the Economic Order Quantity. The Economic Order Quantity is the point where the cost of ordering the goods is not greater than the cost of holding the goods. The task of inventory control has been simplified by the widespread availability of information technology.

Production Control

Production control systems are used to determine where and when a task is to be performed so that an order can be delivered at the appropriated time. These systems also support monitoring of the production process to enable early detection of problems. The type of production control system being used will depend on the organisations production methods. An assembly plant will use a flow control system to reduce bottlenecks. A specialist firm making one off products may use an order control system to track the order from design through to delivery.