MANAGEMENT – DEFINITION

Management is the process of achieving organisational objectives by working with and through others in an ever-changing environment.

Fayol (1916) wrote that all managers perform five main management functions:

- Planning: Planning is an activity which involves making decision about ends.

- Organising: This is concerned with dividing and coordinating tasks.

- Commanding: This refers to the importance of leadership in organisations.

- Controlling: Controlling involves measuring actual performance against agreed standards and taking corrective action if necessary.

- Co-ordinating: This involves ensuring that all activities and groups are brought together to achieve the overall objectives.

Today these functions have been condensed down to the following four:

- Planning

- Organising

- Leading

- Controlling

Planning

Planning is concerned with where the organisation wants to be in the future and how it is going to get there. The planning function includes defining an organisation’s goals, establishing an overall strategy for achieving those goals and developing a hierarchy of plans to co-ordinate all activities. Planning can be long term or short term and takes place at all levels in the organisation.

Organising

Organising generally follows planning and it refers to deciding on an organisational structure, staffing it adequately and making sure the organisation is running efficiently. Managers develop a framework of necessary tasks and available resources called an organisational structure. This structure sets out the groupings of staff organisation. In simple terms organising includes determining how tasks are to be done, who is to do them, how the tasks are to be grouped, who reports to whom and where decisions are to be made. 3. Leading

Leadership involves motivating employees to achieve organisational goals. Leading entails creating a vision, communicating that vision and goals, and influencing others to achieve high levels of performance. It also involves directing the activities of others and resolving conflicts among employees.

Controlling

Activities within an organisation don’t always go as smoothly as planned. Controlling involves monitoring employee activities to determine whether or not they are achieving targets. It involves comparing actual performance against predetermined goals and taking corrective action if necessary.

ROLE OF MANAGEMENT

Mintzberg (1973) suggested that rather than looking at the functions of managers, we should instead look at the roles they perform.

Interpersonal Role

A key aspect of a manager’s job involves interacting with other people. In the role of figurehead the manager represents the organisation by performing ceremonial and symbolic activities. In the role of leader a manager will attempt to motivate, communicate with and influence people. As a liaison a manager develops relations with groups both inside and outside the organisation. These groups could include customers, trade unions and government departments.

Information Role

Information is a very important resource of any organisation. The monitor role refers to the acquiring of information from internal and external resources. The disseminator role refers to the transmitting of information to those who require it. As a spokesman a manager conveys information to groups outside the organisation such as the media.

Decisional Role

The entrepreneur role involves the manger seeking out new ways to deal with problems and find opportunities for the organisation. The disturbance handler role involves resolving conflicts between individuals and teams. In the resource allocator role the manager must make decisions on how to allocate resources such as money, people, materials and time, to best achieve the objectives of the organisation. In the negotiator role a manager will negotiate with various interest groups such as customers, suppliers and other managers.

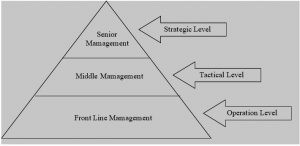

LEVELS OF MANAGEMENT

The following are the three main levels of management:

- Senior Management

- Middle Management

- Front Line Management

Senior Management

Senior management are concerned with strategic issues such as the mission and direction they will take into the future. They must make and implement strategic decisions and communicate these decisions to relevant parties such as the shareholders and customers. Senior managers include the Chairperson, Chief Executive, Directors and members of the Board.

Middle Management

Middle management operates at a tactical level, translating strategic direction and organisational goals into tangible achievable objectives for their division. Middle management acts as a link between the strategic level and the operational levels. Examples of middle managers include Plant and Operations managers.

Front Line Management

This level of management, which is also referred to as “Supervisory Management” and “Operations Management”, is responsible for directly managing and supervising employees involved in the day-to-day operations of the organisation. Front line managers operate between middle management and the operational personnel.

Team Leaders

In the traditional management hierarchy there are three levels of management as shown in Figure 1.2. In these traditional structures the line managers are responsible for the performance of non-managerial employees and have the authority to hire and fire workers, make job assignments and control resources. Williams, C. (2007) identifies a fourth kind of manager – the team leader. This new kind of management job has developed as companies have shifted to self-managed teams. Team leaders are responsible for facilitating team performance. Team leaders help their team members plan and schedule work, learn to solve problems and work effectively with each other. Team leaders act as a bridge between their own teams and other teams. Team leaders are also responsible for internal team relationships.

Planning Horizon

A key task of managers at all levels is planning. However the planning timeframe is different for each level. Senior managers plan for the long term, between 3-5 years. Middle managers focus on a mid-term timeframe, normally for up to three years. Front-line managers plan for the short term normally in term of weeks and months.

Horizontal levels of Management

The three levels of management discussed above are called vertical levels. Different types of management also occur horizontally across the organisation. Functional departments such as marketing, operations, finance and human resources have their own functional managers who are responsible for activities within their department. The various management functions are discussed in Section 3 of this course manual.

MANAGEMENT SKILLS

A manager should posses a range of skills in order to be successful. The skills required can be grouped into three categories (Katz, R. 1973):

- Technical Skills

- Human Skills

- Conceptual Skills

Technical Skills

Technical skills relate to the performance of specific tasks. It relates to expertise in specific organisational functions such as finance, operations etc. Technical skills could also include specialised knowledge and competencies with particular tools and techniques. Technical skills are more important at lower levels of management.

Human Skills

Human skills are often referred to as interpersonal skills and include the ability to work with other people and work effectively in group situations. Human skills are concerned with a manager’s ability to motivate, lead, communicate and resolve conflict. Human skills are important at all levels of management.

Conceptual Skills

Conceptual skills refer to the ability to think strategically, to take a long-term, broad view of the organisation in its entirety and the relationship between each part.

Managers at all levels in the organisation require conceptual skills but they are of greater importance at the senior levels.

In addition to these three categories of skills managers must be effective in a range of other skills such as verbal and written skills.

EFFECTIVE MANAGERS

According to research by John Kotter (1999), Effective Managers spend significant time establishing personal agendas and goals; both short and long-term. Effective managers spend a great deal of time building an interpersonal network composed of people at virtually all levels of the organisation. Managers use their networks to execute personal agendas and accomplish their own goals.

To be an effective manager a person must have the necessary skills required to manage.

Characteristics of Effective Managers

Bateman and Zeithamal (1993) proposed the following three characteristics of effective managers or leaders:

- Active Leadership

- Ability to Motivate Others

- Opportunity of High Performance

Active Leadership

Active leaders are those who take a hands-on role. They make an active contribution to the team effort.

Ability to Motivate Others

Effective managers are able to motivate others to achieve the organisation’s goals. They communicate to workers the importance of these goals and the performance required to achieve the goals.

Provide Opportunity of High Performance

To be able to achieve a high level of performance; managers must have autonomy and control over their area of work. Having control over resource and decision-making is crucial to the effectiveness of managers.

MISTAKES MANAGERS MAKE

Another way to understand what it takes to be a manager is to look at the mistakes managers make. Based on studies of US and British managers, Williams, C. (2007) identifies the following top ten mistakes that managers make:

- Insensitive to others; abrasive, intimidating; bullying style

- Cold aloof, arrogant

- Overly ambitious: thinking of the next job, playing politics

- Specific performance problems with the business

- Over-managing; inability to delegate

- Unable to staff effectively

- Unable to think strategically

- Unable to adapt to a boss with a different style

- Over-dependent on advocate or mentor

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY

Business ethics concerns the moral conduct of an organisation. It concerns the moral judgements that managers have to make, taking into account their own belief and the organisation’s belief of what is right and what is wrong. There are three categories that govern human behaviour (Daft, 2010). The first relates to the law and what is legal, while the third is the area of free choice where the individual (or firm) is free to choose how to behave. In between the two extremes is the second category which is the area of ethics choice. While the law does not govern actions in these areas, there are moral standard, values and expectations that are shared by society and should guide individual and corporate behaviour. For example is it ethical for a profitable company to cut employee’s wages so it can make even greater profits? Ethics presents dilemmas for business as a decision made on an ethical basis may reject the most profitable option in favour of one that is of greater benefit to society.

Ethical Decision Making

To aid organisations that want to pursue an ethical direction in their activities, they can apply one of the following ethical decision making approaches:

- Utilitarian Model

- Moral Rights Model

- Justice Model

Utilitarian Model

Under a utilitarian model an ethical decision is one that produces the greatest good for the greatest number of stakeholders. Therefore a manager would consider the impact of a decision on each stakeholder group and attempt to choose a course of action that would maximise the benefits and minimise the costs overall. Therefore this represents a logical/benefits analysis approach that appeals to managers. However the difficulty is trying to appreciate the value of the decision to each stakeholder group.

Note: Stakeholders would typically include:

- Owners and Senior Managers

- Employees

- Customers

- Suppliers

- Local Community

- Government

Moral Rights Model

This approach proposes that certain rights should be protected, such as freedom of choice, privacy, health and safety, freedom of speech etc. Therefore any decision that violates these rights is considered to be unethical. The difficulty with this approach is deciding the importance of stakeholder’s rights, whose rights takes priority – the right of the individual or the rights of the business.

Justice Model

This approach rests on equity, fairness and impartiality. Therefore, an ethical decision is one which shares the costs and benefits of a decision amongst stakeholders groups, in a fair manner. However, equity does not imply equality, consequently when distributing pay rises it may seem equitable to reward those performing at a higher level. This may be seen as fair but not equal.

Corporate Social Responsibility

Corporate social responsibility is management’s obligation to make choices and take actions that will contribute to the welfare and interests of society as well as to the welfare and interests of the organisation (Daft, 2010). A business has economic responsibilities to produce goods and services that society wants and to generate profits for shareholders. Organisations have legal responsibilities to operate within the law. A business also has an ethical responsibility that may go beyond areas covered by the law to treat individuals fairly and equally, and to respect the rights of the individual and society as a whole. The company can also exercise discretionary responsibilities, which drive voluntary acts that make a contribution to society, for which no economic gain is expected.

Corporate Governance

Corporate governance is concerned with the structures and systems of control by which managers are held accountable to the stakeholders in an organisation (Jacoby, S. 2005). In simple terms corporate governance refers to the system by which companies are directed and controlled. It can include internal elements defined by the company officers, shareholders or the constitution of a company, as well as external elements such as government regulations. The aim of corporate governance is to increase transparency and accountability in the manner in which companies are governed.

Corporate governance deals with how management conduct their affairs and how the board of directors supervise the running of the organisation. Corporate governance is the response to the need for ways of ensuring that an organisation is pursuing its proper ends, typically by keeping directors and managers accountable to the shareholders.

Better, more ethical corporate governance has come to be seen as the answer to the public perception of corporate wrongdoing. People often point to practices such as high dividend payouts to shareholders, high executive compensation and the ‘short-termism’ of many business enterprises, which focus exclusively on immediate profits, as evidence that new codes of conduct are needed.

In response to a series of high profile corporate failures and evidence of corporate wrongdoing in the United States in early 2002 (Enron, WorldCom etc.), many countries enacted laws and put codes of practice in place to improve corporate governance. In the US the 2002 Sarbanes-Oxley Act was put in place to protect shareholders and the general public from accounting errors and fraudulent practices in business.

Whistleblowing

Whistleblowing occurs when an employee informs the public of inappropriate activities going on in the organisation. The whistleblower may be motivated by moral reasons or may have been passed over for promotion or suffered some other injustice in the workplace. The consequences of whistleblowing are often extreme: loss of job and/or home, ostracism by peers, loss of family relationships, personal isolation and effects on physical health. Employers look on whistleblowers as disloyal and unworthy of trust, while their peers may regard them as weak or unbalanced. Legislation has been passed in many countries to protect the whistleblower, because if these individuals do not come forward, many cases of wrongdoing would never be exposed.

The arguments for Ethics and Social Responsibility

Daft, (2010) put forward a number of reasons why it makes good business sense to be concerned about ethics and social responsibility:

- Paying attention to ethics and social responsibility is as important as profits and costs

- Ethical and social actions impact financial performance

- Companies are beginning to measure non-financial factors that create value

- Customers pay attention to a company’s ethics and social responsibility