What is Internal Control System?

The internal control structure of a company consists of the policies and procedures established to provide reasonable assurance that specific entity objectives will be achieved.

Objectives of Internal Control System

- To ensure that the business transactions take place as per the general and specific authorization of the

- To make sure that there is a sequential and systematic recording of every transaction, with the accurate amount in their respective account and in the accounting period in which they take place. It confirms that the financial statement fulfils the relevant statutory

- To provide security to the company’s assets from unauthorized use. For this purpose, physical security systems are used to provide protection such as security guards, anti-theft devices, surveillance cameras,

- To compare the assets in the record with that of the existing ones at regular intervals and report to the those charged with governance (TCWG), in case any difference is

- To evaluate the system of accounting for complete authorization of the

- To review the working of the organization and the loopholes in the operations and take necessary steps for its

- To ensure there is the optimum utilization of the firm’s resources, e. men, material, machine and money.

- To find out whether the financial statements are in alignment with the accounting concepts and principles.

An ideal internal control system of an organization is one that ensures best possible utilization of the resources, and that too for the intended use and helps to mitigate the risk involved in it concerning the wastage of organization’s funds and other resources.

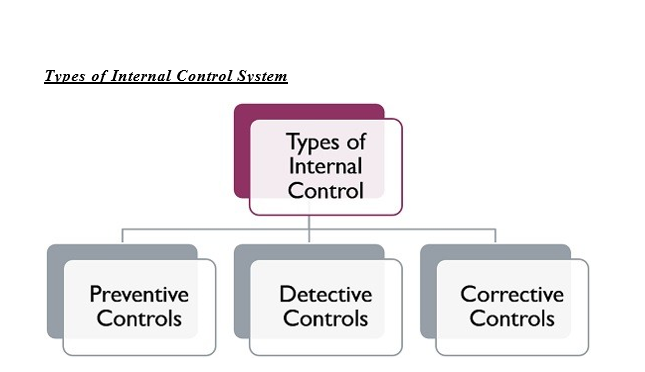

- Preventive Controls: These controls are introduced in the firm to stop errors and irregularities from taking

- Detective Controls: These controls are implemented to reveal errors and irregularities, once they take

- Corrective Controls: These controls are designed to take corrective action for removing errors and irregularities after they are

The type of internal control system implemented in the organization will be based on the company’s nature and requirements.

Internal Control System is important for every organization, for efficient management as well as it also assist in the company’s audit. It includes all the processes and methods to help the company in reaching its ultimate objective.

Components of Internal Control System

1. Controlling the environment

The control environment is the basis of other elements of all other components of the internal control system. Moral values, managerial skills, the honesty of employees and managerial direction, etc. are included in the controlling environment.

2. Risk assessment

After setting up the objective of business, external and internal risks are to be assessed. The management determines risk controlling means after examining the risks related to every objective.

3. Control activities

The management establishes a controlling activities system to prevent risk associated with every objective. These controlling activities include all those measures that are to be followed by the employees.

4. Information and communication

Relevant information for taking decision are to be collected and reported in proper time. The events that yield data may originate from internal or external sources.

Communication is very important for achieving management goals. The employees are to realize what is expected of them and how their responsibilities are related to the activities of others. Communication of the owners with outside parties’ like’s suppliers is also very important.

5. Monitoring

When the internal control system is in practice, the organization monitors its effectiveness so that necessary changes can be brought if any serious problem arises.

Responsibility for Internal Control System

It is the general responsibility of all employees, officers, management of a company to follow the internal control system.

The under-mentioned three parties have definite roles to make internal control system effective:

1. Management

Establishment and maintenance of an effective internal control structure mainly depends on the management. Through leadership and example or meeting, the management demonstrates ethical behavior and integrity of character within the business.

2. Board of directors

The board of directors possessing a sound working knowledge gives directives to the management so that dishonest managers cannot ignore some control procedures. The board of directors stops this sort of unfair activity. Sometimes the efficient board of directors having access to the internal audit system can discover such fraud and forgery.

3. Auditors

The auditors evaluate the effectiveness of the internal control structure of a business organization and determine whether the business policies and activities are followed properly. The communication network helps an effective internal control structure in execution. And all officers and employees are part of this communication network.

Characteristics of a Proper Internal Control System

An effective internal control system includes organizational planning of a business and adopts all work-system and process to fulfill the following targets:

- Safeguarding business assets from stealing and

- Ensuring compliance with business policies and the law of the

- Evaluating functions of each employee and officer to increase efficiency in

- Ensuring true and reliable operating data and financial

It is to be kept in mind, a business organization, be its small or large, can enjoy the benefits of adopting an internal control system.

Prevention of stealing-plundering and wastage of assets is a part of the internal control system.

Protection of assets

A business organization protects its assets in the following ways:

1. Segregating the duties of the employees

Segregation of the duties of the employees means that each employee is assigned with specific tasks. The person in charge of assets is not allowed to maintain accounts of the assets.

Some other person maintains the accounts of these assets. Since different employees perform the same nature of transactions, the work of each is automatically checked. Segregation of the duties of the employees of an organization reduces the possibility of stealing assets and if stolen, detection becomes easier.

For example, there is no scope for stealing cash by a cash-receiving employee where cash receipts accounts are maintained by a different employee.

2. Assigning specific duties to each employee

The employee assigned with a specific duty is held responsible for his assigned activities. If and when any problem arises the manager can immediately identify the person concerned and holds him liable.

Lost documents can easily be detected if the task of maintaining records is assigned to a particular employee and it becomes possible to know the recording process of transactions.

An employee assigned with a particular job can easily provide necessary information regarding that job. Moreover, an employee feels proud if he is assigned a particular job and tries to complete the job using die best of his skill.

3. Rotating job assignments of the employees

Some organizations rotate job assignments of employees at intervals to avoid fraud-forgery by the employees concerned.

Under this policy, the employee concerned can easily understand that on the placement of somebody else in his place his dishonesty if it is done, will be detected. This ensures the honesty of an employee.

4. Using mechanical devices

Business concerns adopt various mechanical devices to avoid stealing, destruction, and wastage of assets. Under the mechanical system, cash register, cheque-protectors, time-clock, mechanical-counters, etc. are used as control methods.

Since a cash-register contains locking-tape, each cash sale is recorded here.

The amount of cheque is written on the cheque by the cheque-protector machine to avoid any sort of alteration. Arrival and departure of employees are recorded properly with the help of time- clock.

While maintaining accounts of transactions the accountant is. to preserve the following four documents:

- Purchase requisition: Written order placed by the officers of the department concerned to the purchasing department for purchasing a certain quantity of goods is called purchase

- Purchase order: Before purchase, the buyer sends a written order to the seller requesting him to send particular goods. This written order is called a purchase order.

- Invoice/Chalan: The seller sends an invoice with the sold goods to the buyer wherein the descriptions, quantity, rates of the goods are

- Receiving report: It is a purchase document prepared by an officer of the purchasing It is treated as documentary evidence of the goods received.

Three elements of the internal control system are:

- Environment control: The attitude, alertness, and work-zeal of directors, managers and shareholders are reflected through environmental

- Accounting system: Accounting system means some procedures and recordings with which identification of business transactions, classification, summarization, statement preparation and analysis for timely presentation of correct information are

- Control procedure: The additional policies and procedures adopted by the business authority for ensuring the achievement of the specific goal of a business organization are the controlling

These control procedures are:

- Proper delegation of power,

- Segregation of responsibility,

- Preparation and use of documents,

- Adoption of adequate security measures to protect the properties, and

- Independent control over the execution of

An internal control system, not only prevent fraud forgery but also fulfills other objects:

- The business organization implements its policies complying with the prevailing laws of the

- Employees and officers discharge their assigned responsibilities to increase efficiency in the execution of work.

- Financial statements provide correct and reliable information maintaining proper

In light of the above discussion, it can be briefly stated that the overall policies and plans adopted by the management for the proper execution of business activities are called the internal control system.