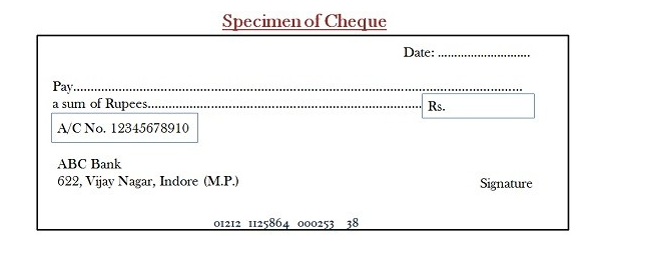

Definition of Cheque

A cheque is a type of bill of exchange, used for the purpose of making payment to any person. It is an unconditional order, addressing the drawee to make payment on behalf the drawer, a certain sum of money to the payee. A cheque is always payable on demand, i.e. the amount is paid to the bearer of the instrument at the time of presentment of the cheque. It is always in writing and signed by the drawer of the instrument.

There are three parties involved in case of cheque:

- Drawer: The maker or issuer of the

- Drawee: The bank, which makes payment of the

- Payee: The person who gets the payment of the cheque or whose name is mentioned on the

It should be noted that the issuer must have an account with the bank. There is a specified time limit of 3 months, during which the cheque must be presented for payment. If a person presents the cheque after the expiry of 3 months, then the cheque will be dishonored. The various types of cheques are:

- Electronic Cheque: A cheque in electronic form is known as an electronic

- Truncated Cheque: A cheque in paper form is known as truncated

Bill of Exchange:

The legal definition is “A bill of exchange is an instrument in writing containing an unconditional order signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument.” It means that if an order is made in writing by one person on another directing him to pay a certain sum of money unconditionally to a certain person or according to his instructions or to the bearer, and if that order is accepted by the person on whom the order was made, the document is a bill of exchange.

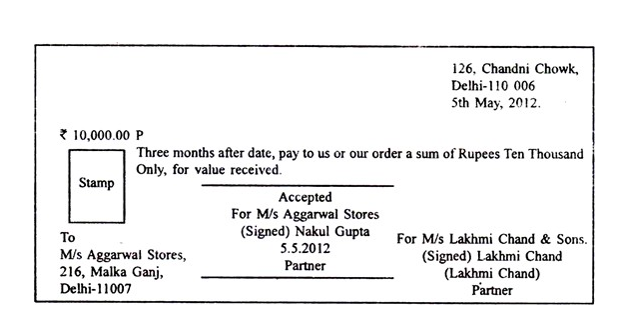

The following is a specimen of bill of exchange:

3. Cheques are also included among negotiable instruments. In the specimen bill of exchange shown above, M/s Lakhmi Chand & Sons are the drawers as well as the payees of the bill of M/s Aggarwal Stores are the drawees and the acceptors of the negotiable instrument. The drawees become habile to pay for the bill of exchange only after they have accepted it. Before acceptance, a bill of exchange is known as a draft.

The following are the advantages of bills:

- Presumption of consideration:

In a bill, consideration is presumed. In other words, the Court presumes that the acceptor of the bills of exchange or maker of the promissory note is indebted to the drawer of the bill or payee of the promissory note. It is a big advantage. In the absence of the bill, the seller of goods and services or the lender of the money has to prove the indebtedness of the purchaser or borrower in case of a default.

2. No locking of money:

A bill provides the payee an option either to wait for money till the date of maturity of the bill or to get cash at any time by getting the bill discounted with the bank at a reasonable rate of interest. The bill can also be used to discharge the liability to a creditor by endorsing the bill in the creditor’s favour. Thus, the seller need not keep the money locked up for the period of credit allowed by him to the customer.

3. Source of finance:

Accommodation bills enable the businessmen to obtain funds at a low rate of interest to meet their temporary financial requirements.

4. Safe and convenient means of transmitting money:

Bill is a safe and convenient means of transmitting money by one person to the other; one can avoid the risk of carrying currency by using a bill.

5. Planning by creditors:

A bill fixes the exact date of payment. The creditor knows when he is required to make payment and can make arrangements accordingly.

There are three parties involved in the bill of exchange, they are:

- Drawer: The maker of the bill of

- Drawee: A person on whom the bill is drawn, e., the person who gives acceptance to make payment to the payee.

- Payee: The person who gets the

There are three days of grace allowed to the drawee, to make payment to the payee, when it becomes due. You might wonder about the days of grace, let’s understand it with an example: A bill is drawn on 5-10-2014 in the name of X, to make payment to Y after 3 months. The bill will become due on 5-01-2015 while the date of maturity is 8-01- 2015 because of 3 days of grace are added to it. The following are the types of bill of exchange:

- Inland Bill

- Foreign Bill

- Time Bill

- Demand Bill

- Trade Bill

- Accommodation Bill

Key Differences Between Cheque and Bill of Exchange

- An instrument used to make payments, that can be just transferred by hand delivery is known as the An acknowledgment prepared by the creditor to show the indebtedness of the debtor who accepts it for payment is known as a bill of exchange.

- A Cheque is defined in section 6 while Bill of Exchange is specified in section 5 of the Negotiable Instrument Act, 1881

- The drawer and payee are always different in the case of a In general, drawer and payee are the same persons in the case of a bill of exchange.

- The stamp is not required in Conversely, a bill of exchange must be stamped.

- A cheque is payable to the bearer on As opposed to the bill of exchange, it cannot be made payable to the bearer on demand.

- The cheque can be crossed, but a Bill of Exchange cannot be

- There is no days of grace allowed in cheque, as the amount is paid at the time of presentment of the cheque. Three days of grace are allowed in the bill of

- A cheque does not need acceptance whereas a bill needs to be accepted by the

Similarities

- They are Negotiable

- Addressing the drawee to make

- Always in

- Signed by the drawer of the

- Express order to pay a certain

Promissory Note:

A promissory note is an instrument in writing (not being a bank note or a currency note) containing an unconditional undertaking, signed by the maker, to pay a certain sum of money only to, or to the order of, a certain person. This definition given by law means that when a person gives a promise in writing to pay a certain sum of money unconditionally to another person (named) or according to his instructions, the document is a promissory note.

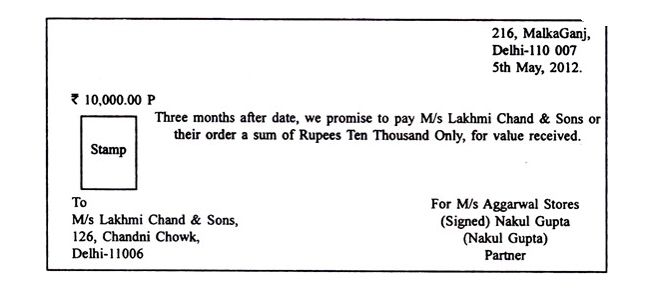

The following is a specimen of promissory note:

In the abovementioned specimen promissory note, M/s Aggarwal Stores are the makers of the promissory note. M/s Lakhmi Chand & Sons are the payees of the note.

Some key features of promissory notes are as follows,

- It must be in writing

- It must contain an unconditional promise to

- The sum payable must be

- The promissory notes must be signed by the

- It must be payable to a certain

- It should be properly

Parties to the Promissory Note

- Maker or drawer: Also called the promisor, he/she is the person makes or draws the promissory note to pay the specified the amount as mentioned in the promissory

- Payee or drawee: Also called the promise, he/she is the person in whose favour promissory note is Usually, the drawer is also the payee.

Components of a Promissory Notes

- Principal amount: It is the amount which is given by the payee and taken/borrowed by the maker of the

- Interest rate: The percentage rate that is multiplied by the principal amount and the period of promissory notes in computing for the

- Interest: Interest is the revenue/income for the payee for loaning out the principal & is an expense for the maker for borrowing the

- Maturity date or due date: The date on which final payment is to be done by the maker of the promissory

- Maturity value: The principal amount due at the maturity date of note in case of non-interest bearing promissory And the sum of principal and interest due at the maturity date of note in the case of interest-bearing promissory notes.

- Place of issue: The place where the maker executed the promissory

Types of Promissory Notes

- Non-interest bearing note: They are promissory notes which do not carry any interest rate with The amount that will be paid at the time of maturity is equal to the face value of the promissory note.

- Interest-bearing Note: Promissory notes which carry an interest rate with The amount that will be paid at the time of maturity is the sum of the face value & interest.

Key Differences Between Bill of Exchange and Promissory

- Bill of Exchange is a financial instrument showing the money owed by the buyer towards the seller. Promissory Note is a written document in which the debtor promises the creditor that the amount due will be paid at a future specified

- Bill of Exchange is defined in Section 5 of the Negotiable Instrument Act, 1881 whereas Promissory Note is defined in Section

- In a bill of exchange, there are three parties while in the case of a promissory note the number of parties is 2.

- Creditor creates Bill of On the other hand, Promissory Note is prepared by the debtor.

- The liability of the maker of the bill of exchange is secondary and Conversely, the liability of the maker of the promissory note is primary and absolute.

- Bill of Exchange can be made in copies, but Promissory Note cannot be made in

- In the case of the bill of exchange, the drawer and payee can be the same person which is not possible in case of the Promissory

The notice of dishonor of a bill of exchange must be given to all the parties concerned, however, in the case of promissory note such notice need not be given to the maker.

Crossing of Cheque

Definition: Crossing of a cheque is nothing but instructing the banker to pay the specified sum through the banker only, i.e. the amount on the cheque has to be deposited directly to the bank account of the payee.

Hence, it is not instantly enchased by the holder presenting the cheque at the bank counter. If any cheque contains such an instruction, it is called a crossed cheque.

The crossing of a cheque is done by making two transverse parallel lines at the top left corner across the face of the cheque.

Types of Crossing

The way a cheque is crossed specified the banker on how the funds are to be handled, to protect it from fraud and forgery. Primarily, it ensures that the funds must be transferred to the bank account only and not to encash it right away upon the receipt of the cheque. There are several types of crossing

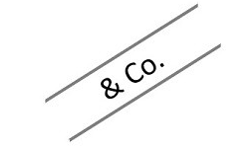

1. General Crossing:

When across the face of a cheque two transverse parallel lines are drawn at the top left corner, along with the words & Co., between the two lines, with or without using the words not negotiable. When a cheque is crossed in this way, it is called a general crossing.

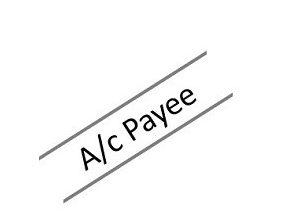

2. Restrictive Crossing:

When in between the two transverse parallel lines, the words ‘A/c payee’ is written across the face of the cheque, then such a crossing is called restrictive crossing or account payee crossing. In this case, the cheque can be credited to the account of the stated person only, making it a non-negotiable instrument.

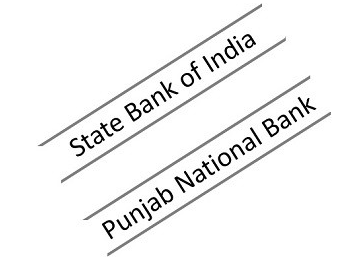

3. Special Crossing:

A cheque in which the name of the banker is written, across the face of the cheque in between the two transverse parallel lines, with or without using the word ‘not negotiable’. This type of crossing is called a special crossing. In a special crossing, the paying banker will pay the sum only to the banker whose name is stated in the cheque or to his agent. Hence, the cheque will be honored only when the bank mentioned in the crossing orders the same.

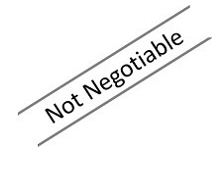

4. Not Negotiable Crossing:

When the words not negotiable is mentioned in between the two transverse parallel lines, indicating that the cheque can be transferred but the transferee will not be able to have a better title to the cheque.

5. Double Crossing:

Double crossing is when a bank to whom the cheque crossed specially, further submits the same to another bank, for the purpose of collection as its agent, in this situation the second crossing should indicate that it is serving as an agent of the prior banker, to whom the cheque was specially crossed.

The crossing of a cheque is done to ensure the safety of payment. It is a well-known mechanism used to protect the parties to the cheque, by making sure that the payment is made to the right payee. Hence, it reduces fraud and wrong payments, as well as it protects the instrument from getting stolen or uncashed by any unscrupulous individual.

Negotiability:

Promissory notes, bills of exchange and cheques are negotiable instruments. This means that the holder can claim payment on them.

However, this is subject to the conditions that the holder takes them:

- Without notice of defect in the title of the transferor, e., in good faith

- For consideration

- Before If these conditions are fulfilled, it does not matter if the title of the transferor was defective.

Thus, if A steals a bill of exchange and passes it on to B who is not aware of A s mode of acquiring the bill and who takes it for value and before the due date of the bill, B will be entitled to get payment on the bill. Here B is a holder in due course. A holder in due course always gets good title except in case of forgery. Moreover, whoever gets the bill (or promissory note) after the holder in due course, will also get a good title to it; it has been purged of all defects

The instrument is passed on from one person to another by endorsement and delivery. Endorsements on bills of exchange and promissory notes are done in exactly the same manner as those on cheques. The liability of the endorser to subsequent parties is also the same. Thus, if a bill of exchange is dis-honored, that is, if payment is not made on the due date by the promisor (drawer in case of bill of exchange), money can be claimed from any of the previous endorsers, the payee and the maker of the instrument.

Negotiability plus this liability of the endorsers make a bill of exchange or promissory note an excellent security. Bills of exchange or promissory notes are, therefore, quite willingly purchased by banks. The bank is sure that within a short time the money advanced on the bill will be returned. Bills of exchange are, therefore, excellent ways of granting or receiving credit. A purchaser of goods may not be able to pay immediately, but the seller may not be able to wait.

A bill of exchange or a promissory note will admirably solve the difficulty. The purchaser promises, in writing, to pay the seller or his order the sum due and hands it over to the seller. The seller goes to die bank and gets the note discounted. The seller thus gets the payment immediately, while the purchaser is not compelled to find money immediately. Bills of exchange or promissory notes, therefore, are excellent lubricating oils to the wheel of commerce.

Although a bill of exchange or a promissory note really amounts to nothing more than a promise that the money will be paid on such and such date or on demand, the willingness of banks to advance money (technically called discounting) makes it a special type of asset only one degree removed from balance at bank, Hence, in business houses, a person is deemed to have cleared his debt when a bill of exchange (duly accepted) or a promissory notes is received from him.

The person who gives a bill of exchange or a promissory note considers that the money due has been paid and debits the creditor’s account accordingly. A person who receives a bill of exchange or promissory note can adopt any one of the three courses.

He can:

- Keep it till the date of maturity

- Pass it on to one of his creditors

- Get it discounted with a bank

Date of Maturity is always calculated by adding three days of grace. Thus, if a bill, dated 8th January is for 2 months after date, the date of maturity will be 11th March. If the due date falls on a holiday, the due date will be the previous day. A bill falling due for payment on August 15 will have to be paid on August 14.