Purpose: To introduce the learner to the general rules and technical knowledge of lending.

Each lending case has to be treated on its own moment however these are a number of general principles which should be applied in all cases.

Specific Objectives

By the end of the lesson the learner should be able to:

1.1 Philosophy of Lending

A lender “lends” money and does not give it away, he/she applies judgment that at some future date repayment will take place. The lender needs to look into the future and ask the question whether the customer will pay at agreed date. There will always be some risks that the customer will be unable to repay. In assessing the risk of non-repayment the lender needs to demonstrate both skill and judgment. The lender’s objectives are to assess the extent of the risk and try to reduce amount of uncertainty that exist over the proposed repayment period.

While there are guidelines to be followed there is no “magic” formula. The lender must gather enough and relevant information and apply skills in making a judgment. The skills applied in one the proposal may never apply in another that is why experienced lenders

describe lending as an “art” rather than a science. Lenders must seek to arrive at an objective decision. The approach of true professionalism is to resist outside pressures and insist on sufficient information and time in order to understand and evaluate the proposal.

A lender who is confident in his / her ability will apply the following:

- Take time to reach a decision because detailed financial information requires time to be absorbed.

- Get a second opinion from another experienced lender

- Get full information from customer and not to rush in making assumptions or “fill in” missing details.

- Not to take customers statements at face value ask for evidence.

- Distinguish between facts, estimates and opinions when forming a judgment.

- Think again when “gut reaction” suggest caution even though factual assessments look satisfactory.

1.2 Methodical Approach to Lending

There are five stages in analyzing a new lending proposition.

- Introduction to the customer

- Application by the customer

- Review of application

- Evaluation

- Monitoring and control

1. Introduction to the customer

Lenders can only do successful business with individual they know and feel comfortable with. References are not taken only every occasion an account is opened. Nevertheless, all the account opening procedures should be followed. Account opening procedures

must be followed to the latter to ensure that the customer is honest and trustworthy. This is especially important when the customer wishes to borrow at a later stage. An important source of new business to lenders is introduced from professional advisors such as

accountants and advocates. However this not to say banks are obliged to lend to customers introduced in this way. The lender must treat each case on its merit.

2. Application by the customer

This can take away many forms but should include a plan for repayment of borrowing and an assessment of contingencies which might arise and how the borrower will deal with each item. The application may be in a detailed written form or verbal. The lender

must draw out sufficient further information to enable risks in the application to be fully assessed.

3. Review of application

At this stage all relevant information which is required needs to be tested and other data sought if necessary. Either formally or informally the lender applies the canons or principles of lending. It is sometimes difficulty to remember all the points to cover during

an interview and many lenders use a mnemonic as a check list. There are a number of mnemonics in common use, but the most common are CCCPARTS (Character, Capital Capacity, Purpose, Amount, Repayments, Terms, and Security), PARSER (Person,

Amount, Repayment, Terms, Security, Expediency, Remuneration) and CAMPARI (Character, Ability, Margin, Purpose, Amount, Repayment, Insurance). CAMPARI is the most popular of the mnemonics and will be discussed later.

4. Evaluation

Once all available information has been assembled, an evaluation of proposal should be made. It’s done in two stages:

- An assessment of the feasibility of the borrowers plan for repayment. If the proposal is not viable it’s pointless to continue.

- A critical appraisal of what might go wrong. It involves likelihood of such events occurring and the effect on bank’s position.

The aim of this evaluation is to establish risk involved. Listing the pros and cons of a proposition is helpful more regard is placed on facts and evidence rather than estimates and opinions. Once a lending has been made, the risk lies in the way the customer handles any problem which might arise. The lenders evaluation concentrates on understanding borrower’s risks and assessing the borrower ability the deal with them. In cases where the lender feels that the risk is not bearable, and wishes to help a good customer advice the customer to the ‘re-engineer’ it into a more acceptable form.

5. Monitoring and control

It’s highly unlikely that is a customer expectation will exactly go as planned. It’s therefore necessary for lenders to review progress regularly. The earlier the problems are identified the better will be the chances of controlling them and providing practical advice to the customer which in turn protects lenders position. Regular monitoring of corporate account can also enhance the lenders image on eyes of customer. This provides evidence to the customer of a wish to understand the underlying business and to be involved in solving future problems. A monitoring plan should be established at the beginning and where provision of regular information is necessary suitable arrangements should be made and a follow-up.

1.3 Principles / Canons of Lending

C – Character

This can be deduced from past relationship with the customer to find out:

- How reliable is customer words regarding details of proposition and the promise of payment.

- If customer’s track record; was there any previous borrowing and if so was it repaid without trouble.

- If customer is new, why is he approaching the lender?

- Can bank statement be seen to assess conduct of the account?

A – Ability

This relates to borrowers capacity in managing financial affairs and it’s similar to character as far as personal customers are concerned. The following points relate to business customers:

- Is there a good spread of skills and experience among management team e.g. production, marketing and finance?

- Does the management team hold relevant professional qualifications?

- Are they committed in making the business successful?

- If the funds are earmarked for specific activity do they have necessary skills and experience in that area?

M-Margin

Refer to the relationship between amount to be borrowed and value of security being offered as collateral. If the proposal is risky the bank requires the security value to be almost equal to the money to lend. Margin also relate to interest, commission and other

fees. Collateral required and charges like interest and other fees should reflect the inherent risk in the proposal.

P-Purpose

The purpose should be legal and acceptable to bank policy. The facility should be the in customers best interest and customers should be able to carry out the project successfully.

A-Amount

Evaluate whether the customer is asking too mush or too little. Establish the amount required by the project and to cover other incidental expenses. The amount to be lent should be in proportion with the customer’s resources and contribution. A reasonable

contribution by the customer in the project indicates commitment and acts as a buffer against misuse of funds borrowed.

R-Repayment

The risk in lending is found in assessment of repayment proposals. It’s important that the source of repayment is made clear by the customer and the lender must establish the degree of certainty that the promised funds will be received. Where the source of income

/cashflow, the lender requirement projections to ensure that there are surplus funds to cover repayment after meeting other commitments.

I- Insurance / Security

The cannons of lending should be satisfied irrespective of availability of security or insurance. However, security is necessary in the event the repayment proposal fail to materialize. It provides an alternative source of recovery or fall back position should the promised source of repayments fails. It’s important that no advance is made until security procedures have been completed or at least at a stage where the completion can take place without the need to involve borrower.

Example 1.1

Jeremy has maintained an account at your branch for many years. You have very little detailed information on file regarding him but you are aware he has business interests in the city. He is a director of three companies and from time to time sits up board of

enquiry set by government.

No regular credits are seen in the account but over the past three years credits totaling Ksh 250,000 have been received including six dividends warrant amounting Kshs75, 000.

Nine months ago you wrote to him suggesting that the dividends should be mandated but there was no response to his letter.

Over 2 years ago Jeremy wrote to you regarding the prestige card issued by your bank card company. Subsequently a formal application was made and a card was issued. As part of this facility an unsecured overdraft limit of 75,000 has been recorded on his

account.

Today you receive a letter from Jeremy enclosing a cheque of Kshs200, 000 in his favour by a firm of Nairobi lawyers and three share certificates all in his name with a current market value of 800,000. He explains that he is involved in a small syndicate of investors

they are about to complete the purchase of a significant investment in the US but at this time he can give no details. He is therefore likely to issue a cheque over the next week for Kshs 1,000,000 and asks you to increase his overdraft by 750,000. Set out in detail you

reply to Jeremy.

Solution

Apply CAMPARI in your analysis

Character connection and capital initial reaction

This is a relatively a long standing customer who has presumably operated the account satisfactory. You would therefore wish to help if at all it’s possible especially because of the customers standing. Furthermore you do not have any advanced information about

him. As a director of three companies and sitting on government board of enquiry shows that he is a person with vast business operations and of high integrity.

There is evidence of capital from share certificate of Kshs.800, 000 and annual dividends of Kshs.75, 000. He has also been issued a prestige card facilities unsecured. As far as connections are concerned they exists (evidence by board of directorship in three

companies and sitting on government board of enquiries and the investment syndicate group). However you must not let this description influence your judgment.

Ability

Jeremy has satisfactory serviced his Kshs 75,000 prestige card facility. As the same time Jeremy could be having other account in other financial institutions. The bank needs to get clarification from him, what other bank account he holds, other securities and

commitments and liabilities in order to evaluate his ability to repay the loan. Furthermore the source of repayment could also be from realizing investment from which the bank is being asked to finance. This required to be clarified.

Margin

This is a speculative venture as Jeremy and his group want o engage in overseas investment which he doesn’t have full information and even if he had all information the bank cannot adequately ascertain its accuracy as the investment is to be undertaken far

away in the USA. The bank should charge interest at a premium adequate enough to cover this high risk.

Purpose

This is not fully given and it’s presumably a speculative investment you need much information as to the investment and the payback period.

Amount

The bank is being asked to provide additional borrowing of Kshs 750,000 making the bank total exposure of 825,000 be fully utilized assuming he keeps the original limit of Kshs 75,000 overdraft. However you need to check this information.

Repayment

The source of repayment is not given however if it is o come from realization of investor he must provide cashflow projections which must be by the bank. It’s possible that Jeremy is multi-bank and the bank must not have seen some of his income, its important

to find out from him which other bank account he hold and facilities he is enjoying at the moment. The bank also needs to find out the duration of the loan (how long loan is required.)

Insurance / security

This proposal seem to be a speculative venture therefore the risk is high the bank therefore needs to be fully secured and although the share certificate current market value of 800,000 a margin of 20% is required giving security value of 640,000 which may not

be enough to cover the borrowing.

Conclusion / decision

Despite Jeremy excellent credentials, the bank does not have sufficient information to assess the risk attached to the proposal. A top businessman Jeremy should appreciate the need for further information if he really wants the bank to assist him. The proposal is

declined at the moment as it is.

Example 1.2

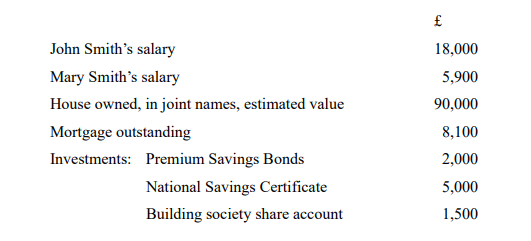

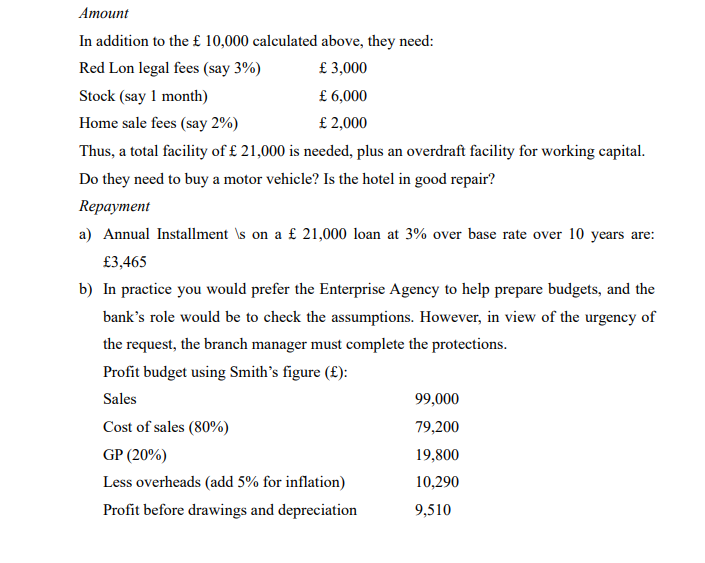

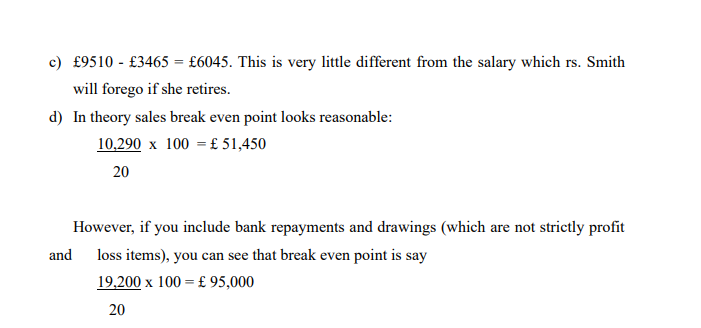

John Smith and his wife (both aged 50) have been customers of your branch for over 20 years. Their account is conducted impeccably. Mr. Smith is employed as the sales manager of a local poultry processing company and Mrs. Smith works as a secretary for a firm of’ solicitors. Their present financial situation is as follows:

On retirement Mr. Smith will receive a pension of some £ 100 per week, and he has been given to understand that his employers are prepared to allow him to retire early, in six months time, on full pension. It will not be possible for Mr. Smith to draw a ‘lump sum’.

Mrs. Smith’s employment is not pensionable.

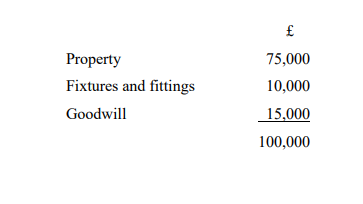

Mr. and Mrs. Smith call to advice you that they wish to purchase a public house (The Red Lion) in a village in a country district some fifty miles away. The Red Lion is not tied to a brewery and therefore does not have to purchase all its supplies of alcohol beverages

from one company. The consideration is as follows:

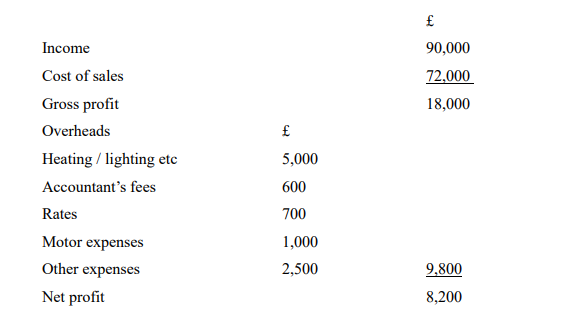

In addition, stock will be purchased at valuation. There are six bedrooms for letting and light meals are provided at the bar. Trading accounts for the existing owners (who are retiring, age 68 and 62) are as follows:

The Smiths are confident that sales can be increased by 10% during the first 12 months following their taking over of the business.

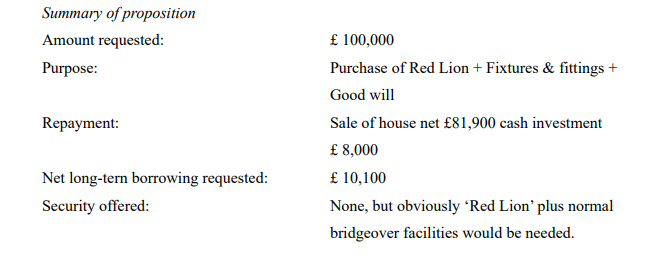

They have been told that other buyers are interested in The Red Lion and whilst it may be possible to defer completion of this purchase, they wish to make their offer today. Therefore they require your immediate decision

Capital / amount

There is no problem on this score as the Smiths’ state is well in excess of the bank’s.

The bank would wish to assist if at all possible because the account has been trouble free for 20 years. You need to establish at the interview whether the Smiths are prepared for the complete change in life style. They will be ‘on call’ seven days a week. Do they seem capable of running the Red Lion? Could Mrs. Smith cope with the books from her work experience?

Purpose

If you are satisfied as to the bridgeover element, then a 10 year loan would be reasonable, bearing in mind their age.

The Smiths must obtain a valuation from an independent professional valuer to see if the asking price is reasonable.

This leaves virtually no margin of safety.

In any event, you need to test the assumptions:

- Why Smith confident he can increase sales?

- You must have independent confirmation that the trading accounts from the present owners are accurate. (In practice balance sheets may not be available.)

- You need a breakdown of sales into bar, food and bedrooms.

- Are there any staff employed (other expenses?

On the face of it repayment would be difficult, and Smiths would suffer a reduced standard of living.

Is the Smiths’ house worth £90,000 and will it sell quickly for that price?

Insurance

If the bank is happy about the bridgeover element, then security is not a problem. A legal mortgage over the ‘Red Lion’ should suffice, provided the independent valuation shows it is worth the asking price on the open market.

Services

Permanent health insurance would be a condition of granting the facility. The bank could also insure the ‘Red Lion’ premises and provide public liability insurance. A 1% arra ngement fee would be required.

Conclusion

The bank is not at risk, but you would only lend if the Smiths could satisfy you that they could generate sufficient profits to repay the bank and provide themselves with a goodstandard of living. On the information provided, the bank must decline.

1.4 Monitoring and Control

Reasons for monitoring account

- To be fully aware of update situation on an account.

- To ensure any borrowing which has been granted remain within the customer’s capacity to repay.

- To observe any adverse trends so that an easily action can be taken.

- To discover any irregular practices bank have recently been criticized for allowing proceeds of claims to be laundered through account without sufficient enquiry.

- To be informed about customers activities to credit worthiness for example evidence of gambling.

- To ensure that the customer is using the account for agreed purpose.

- To confirm information provided by customer e.g. amount of salary and monthly commitment.

Methods of Monitoring

It’s unrealistic to monitor every personal customer, concentrate effort of those accounts which are likely to accuse for concern.

Bank branches have a lot of information can be categorized into 3 main types:

1. Computer print outs.

2. Customer statement sheets

3. Entry vouchers

Computer print outs

Different banks have different computers systems and produce different printouts. However all of them have the capacity to supply historical information of the trend on individual customers’ accounts. When looking at this information the main questions

which should be asked are:-

- What is the worst balance trend?

- What is the best balance trend is there any evidence of a hardcore developing?

- Is the average balance figure worsening?

- Is the turnover through the account out of line with what might have been expected?

- Has there been a change in the run of account compared to previous years.

An adverse trend in one of this need not to be a cause of concern but when deterioration is evident in more than one then some action maybe necessary even if its limited to keeping the account under more regular review.

Customer statements sheets

Customer statement information tends to be standard among banks. The information given / produced is to give the customer an account of individual debits and credits and is not therefore an ideal form for bank monitoring purposes. Specifically produced

computers printouts maybe more user friendly. The question which an examination of statements will help answer includes:

- Is there any pressure on an overdraft limit? Or is the account working satisfactory and showing healthy fluctuations?

- Does the balance give a true picture or it has been distorted by unusual amount?

- Is the turnover through the account rising sharply this might be evident of cross firing?

- When are credits received? Is the monthly salary been received regularly?

- To whom are regular payments out of account paid?

- Is there any change in character of the account?

- Are there any unusual items passing through the accounts?

Entry vouchers

An examination of all debits and credit through a customers account may be time consuming and lender needs to be selective, efforts should be concentrated on:

1. Those accounts which require special attentions.

2. Entries for large amounts

An examination of debit entry will show:-

Evidence of customer interest and financial activities e.g. borrowing – payment to hire purchase company or other finance companies associates – membership fee to clubs or payments to charitable organizations.

Thrifts – regular payment to saving institution and insurance companies.

Whether borrowing is being used for purpose agreed.

This may not represent a problem but it gives evidence of customer truthfulness and might be a cause of concern. An examination of credit will show:

- Source of customers’ income, salary, divided.

- Suspicious transactions. Can large cash receipts be explained?

- Whether uncleared effect are possibly going to be a problem.

Methods of Control

Process can be split into two elements

- Review

- Action

Review

The most common form of lending decision is that which involves the payment of a cheque or where an overdraft limit exists or the limit which is marked is being exceeded. Major banks have daily computers printouts which identify such cheques and debit on

daily basis. Items which are to be returned need to be dealt with before noon so period available for decision is a quick review of the account has to be carried out using the monitoring information discussed above and then applying cannons of lending.

The review of other types of personal lending can be a measured process with time set for discussion with customer and ability to call for more information if necessary. Having reached a decision its useful to make a sort of brief note which can quickly be referred to

in the future to avoid duplication of effort in any subsequent review. Action after review has taken place of action has to be taken. The causes of action available to lenders when things seriously go wrong will be discussed later.