MONDAY: 5 December 2022. Morning Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Do NOT write anything on this paper.

QUESTION ONE

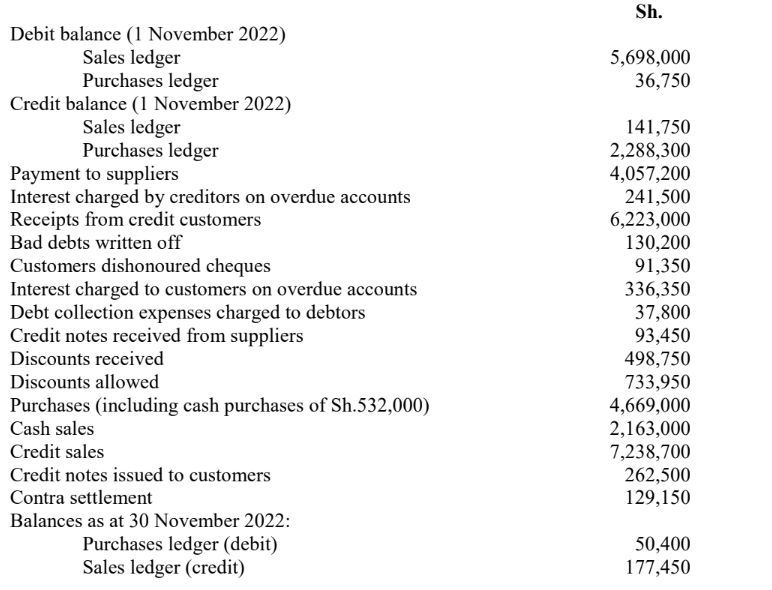

1. The following balances were extracted from the books of Jiwe Traders for the month of November 2022:

Required:

Sales ledger control account for the month ended 30 November 2022. (6 marks)

Purchases ledger control account for the month ended 30 November 2022. (5 marks)

2. Ujenzi Enterprises is a small retail firm. The trial balance of the firm failed to agree on 30 June 2022. The difference was transferred to a suspense account and financial statements prepared. On detailed review of the books, the following errors were revealed:

1. The purchases daybook had been undercast by Sh.1,200,000.

2. Purchases on credit from Demario Ltd. for Sh.600,000 had been posted to their account as Sh.6,000,000.

3. A purchase of a machine worth Sh.8,400,000 had been posted to repairs of machinery account.

4. A customer returned goods worth Sh.1,200,000. This transaction had been entered in the sales returns daybook and posted to the debit of the customer’s account.

5. Sh.7,200,000 owed by Jeru Ltd., a customer, had been omitted when drawing up a schedule of debtors from the ledger.

6. A cash discount of Sh.240,000 had been correctly entered in the cashbook, but has not been posted to the customer’s account.

Required:

Journal entries to correct the above errors. (Narrations not required). (6 marks)

Suspense account duly balanced (including the opening balance). (3 marks)

(Total: 20 marks)

QUESTION TWO

1. Explain the following terms as used in company accounts:

Discount on shares. (2 marks)

Allotment of shares. (2 marks)

Share premium. (2 marks)

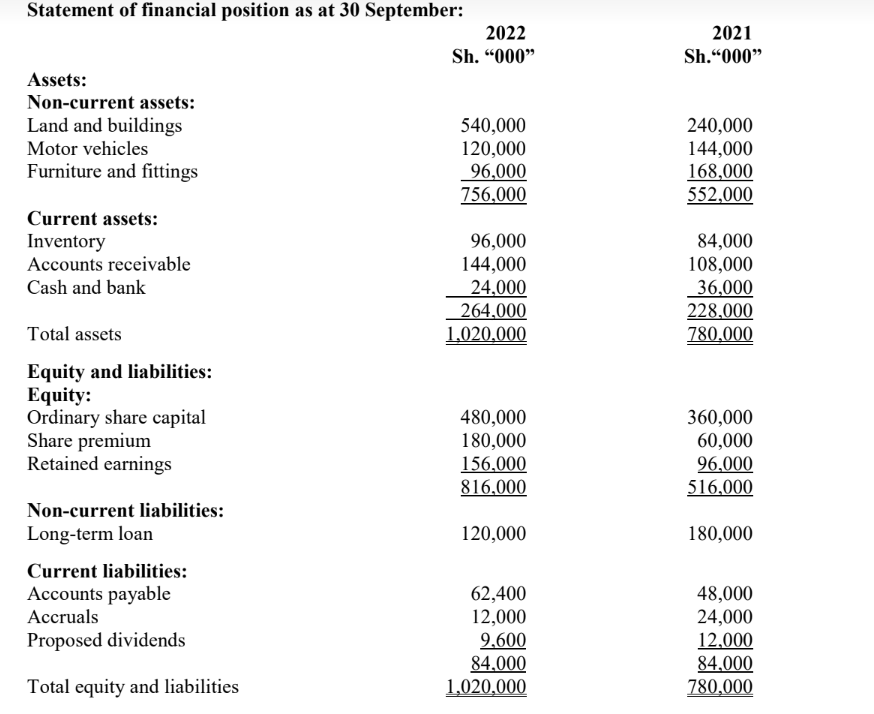

2. The following information was extracted from the books of Viki Ltd. as at 30 September 2021 and 30 September 2022:

Additional information:

1. Profit after tax for the year ended 30 September 2022 was Sh.84,000,000.

2. Interest expense for the year ended 30 September 2022 charged to the statement of profit or loss was Sh.12,000,000.

3. All the taxes and interest for the year ended 30 September 2022 were paid. Total tax for the year ended 30 September 2022 amounted to Sh.48,000,000.

4. Proposed dividends for the year ended 30 September 2022 amounted to Sh.24,000,000.

5. Land and buildings were acquired during the year ended 30 September 2022 at a cost of Sh.360,000,000.

6. During the year ended 30 September 2022, some motor vehicles which had a net book value of Sh.60,000,000 were disposed of for Sh.72,000,000.

7. Motor vehicles are depreciated at 10% on reducing balance.

Required:

Statement of cash flows in accordance with the requirements of “International Accounting Standard (IAS) 7, “Statement of Cash Flows”, for the year ended 30 September 2022. (14 marks)

(Total: 20 marks)

QUESTION THREE

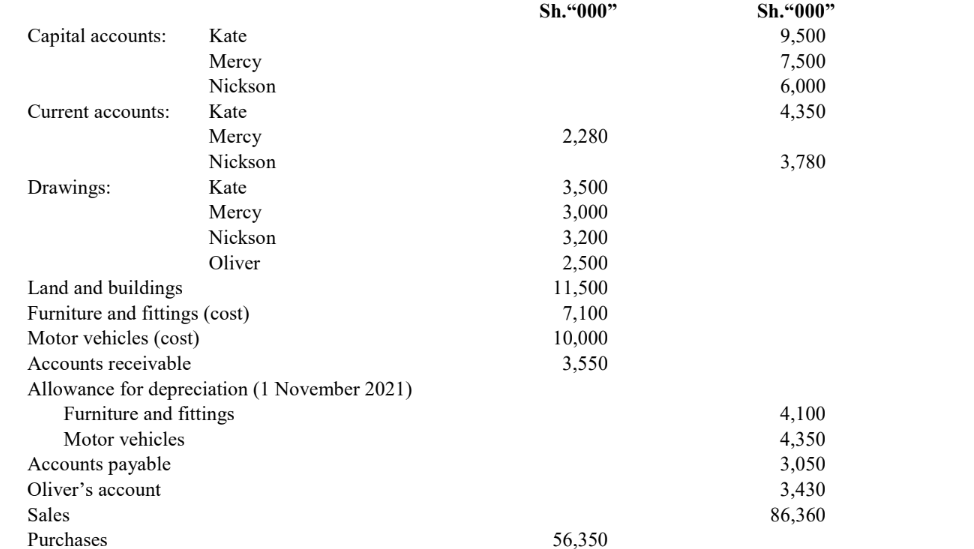

Kate, Mercy and Nickson have been trading as partners under the name Komon Partnership. The partners share profits

and losses in the ratio of 4:3:2 respectively. On 1 November 2021, an employee, Oliver, was admitted as a partner. He

was to bring Sh.1,750,000 as capital and Sh.1,680,000 as his share of goodwill. The partners do not intend to open a

goodwill account. The admission of Oliver has not been fully recorded in the books of account other than the cash record.

The following trial balance was extracted from the books of Komon Partnership as at 31 October 2022:

Additional information:

1. The new profit or loss sharing ratio was agreed at 4:3:2:1 for Kate, Mercy, Nickson and Oliver respectively.

2. On 31 October 2022, inventory was valued at Sh.5,780,000.

3. As at 31 October 2022, accrued salaries and wages and accrued advertising expenses amounted to Sh.1,790,000 and Sh.1,680,000 respectively.

4. As at 31 October 2022, prepaid insurance amounted to Sh.660,000.

5. It was further agreed that since Oliver was a former employee, he would be entitled to a salary of Sh.853,000 per annum with effect from 1 November 2021.

6. The partners resolved that they would receive an interest of 10% per annum on their respective balances of fixed capital at the beginning of the year.

7. Depreciation is to be provided per annum on cost as follows:

Asset Rate per annum

Furniture and fittings 12%

Motor vehicles 25%

Required:

1. Statement of profit or loss and appropriation account for the year ended 31 October 2022. (10 marks)

2. Partners’ current accounts. (4 marks)

3. Statement of financial position as at 31 October 2022. (6 marks)

(Total: 20 marks)

QUESTION FOUR

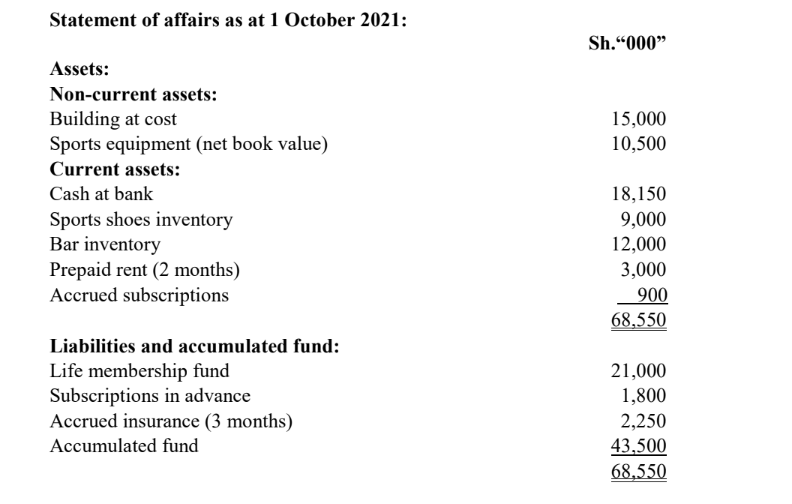

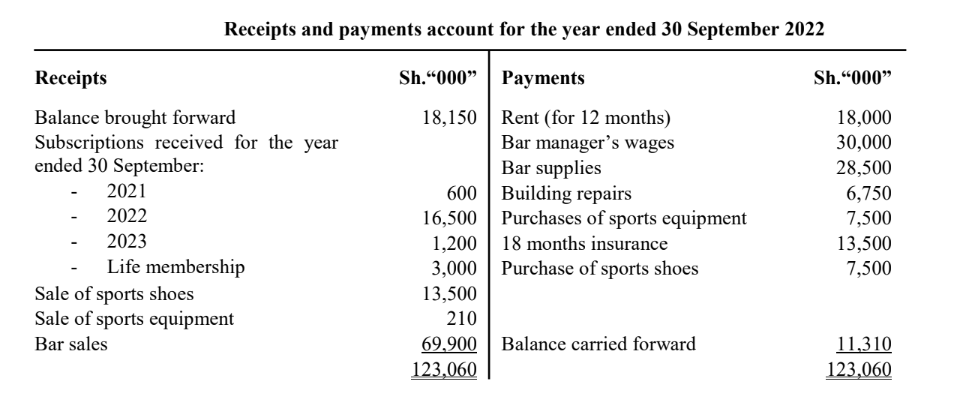

Blaze Sports Club is a members only club. The club generates income through member subscriptions, bar sales and sale

of sports shoes.

The following information relates to Blaze Sports Club for the year ended 30 September 2022:

Additional information:

1. The building was constructed by the club and completed on 30 September 2021. It was commissioned on 1 October 2021 and was estimated to have a useful life of 40 years.

2. Life membership subscriptions are brought into income equally over 10 years in a scheme that begun a few years ago. Since the scheme began, the subscription of Sh.3,000,000 per person has been constant. Prior to the year ended 30 September 2022, eleven (11) life membership subscriptions had been received.

3. As at 30 September 2022, closing bar inventory was valued at Sh.12,750,000 and Sh.1,200,000 was due to the bar suppliers.

4. Four annual subscriptions of Sh.300,000 each had been promised relating to the year ended 30 September 2021, but had not yet been received. Annual subscriptions promised, but not paid, are carried forward for a maximum of 12 months and written off thereafter.

5. As at 30 September 2022, inventory of sports shoes was valued at Sh.13,500,000 while the sports equipment had a net book value of Sh.10,500,000. During the year ended 30 September 2022, sports equipment with a net book value of Sh.200,000 was sold.

Required:

1. Bar statement of profit or loss for the year ended 30 September 2022. (4 marks)

2. Income and expenditure statement for the year ended 30 September 2022. (8 marks)

3. Statement of financial position as at 30 September 2022. (8 marks)

(Total: 20 marks)

QUESTION FIVE

1. Explain the following accounting concepts:

Materiality concept. (2 marks)

Matching concept. (2 marks)

2. In the context of manufacturing accounts:

Explain the term “unrealised profit”. (2 marks)

Describe the treatment of unrealised profits in the books of a manufacturing firm. (2 marks)

3. Explain the following types of funds in the context of public sector accounting:

Revolving funds. (2 marks)

Fiduciary funds. (2 marks)

4. Analyse FOUR objectives of financial statements. (8 marks)

(Total: 20 marks)