UNIVERSITY EXAMINATIONS: 2018/2019

EXAMINATION FOR THE DIPLOMA IN BUSINESS INFORMATION

TECHNOLOGY

DBIT402 COST ACCOUNTING

FULLTIME/PARTTIME

DATE: NOVEMBER 2018 TIME: 2 HOURS

INSTRUCTION: Answer Question ONE and any other TWO questions.

QUESTION ONE: (30 MARKS)

(a) Identify and explain FIVE main benefits of inventory management/ control system

(10 Marks)

(b) Briefly discuss FIVE limitations of Break even analysis (5 Marks)

c) ABC Ltd has an aggregate demand of 5000 units. Each time they place an order there is an

ordering cost of shs.400 the price per unit is sh.1,000 and holding cost is shs.100 per unit.

Required

Determine:

i. Economic Order Quantity (3 Marks)

ii. The number of orders to be made based Economic Order Quantity

(3Marks)

d) Give FIVE detailed differences between marginal and absorption costing (5 Marks)

i) Distinguish between Period costs and product costs (2 Marks)

ii) Semi fixed cost and semi-variable cost as used in cost accounting

(2 Marks)

QUESTION TWO: (20 MARKS)

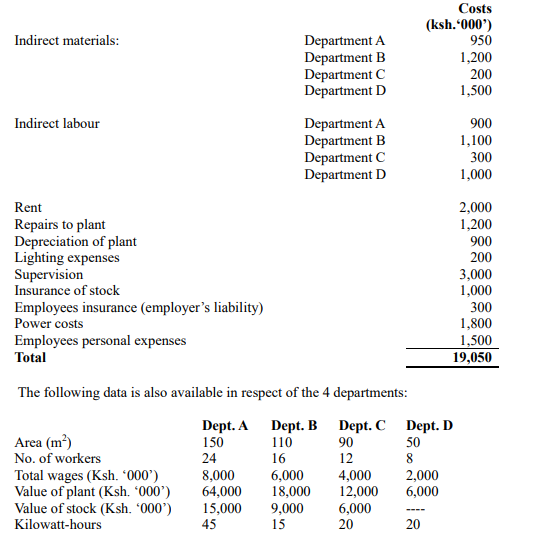

A modern company (X ltd) has 4departments A, B, C and D. The actual cost for a given period

was extracted from their books as follows:

Required:

A) Apportion the above costs to the various departments on the basis of the most equitable basis.

(12Marks)

B) Define marginal costing and give its limitations. (5 Marks)

iii)C) Distinguish between Period costs, product costs and semi fixed cost as used in cost

accounting (3 Marks)

QUESTION THREE: (20 MARKS)

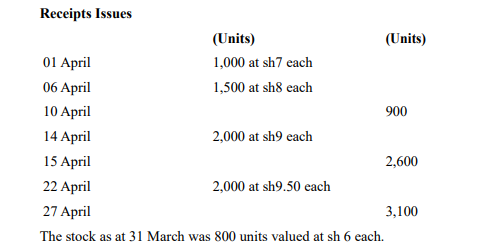

a) The following are the stock movements of stock item PX660

The stock as at 31 March was 800 units valued at sh 6 each.

Required:

b) Prepare stock cards for stock item PX660, showing the value of EACH of the two issues

and the value of closing stock using EACH of the following stock pricing methods:

i). FIFO (8 Marks)

ii). LIFO (8 Marks)

c) Elaborate TWO problems of overstocking and two problems of under stocking (4 Marks)

QUESTION FOUR: (20 MARKS)

a) Differentiate between Financial accounting and cost accounting (10 Marks)

b) Keshi Enterprises has provided the following data in respect of its major raw

materials. Maximum consumption 2,400 units

Normal consumption 1,800 units

Minimum consumption 1,200 units

Re-Order Period 8-12 weeks

Re-order quantity 12,000 units

Required:

i. Re-order level (2 Marks)

ii. Maximum stock level (3 Marks)

iii. Minimum stock level (3 Marks)

iv. Average stock level (2 Marks)

QUESTION FIVE: (20 MARKS)

a) Nutristar is a manufacturer of peanut Butter and has spare productive capacity

which it is seeking to utilize with the introduction of a new product, NutriHoney

You have been provided with the following information which relates to the

product NutriHoney.

Sh

Selling Price per unit 200.00

Direct Material Cost per unit 65.00

Direct Labour Cost per unit 55.00

Fixed Overheads per month 168,000

Required:

i. Calculate the unit contribution for product NutriHoney. (4 Marks)

ii. (4 Marks)

Calculate the break-even point for product NutriHoney.iii.

Calculate the Break Even when the target profit is set at Ksh.

100,000. (4 Marks)

Iv Determine the profit when 1000 units are sold (4 Marks)

B) Distinguish the following types of costs and terminologies.

(i) Cost tracing and cost accumulation (2 Marks)

(ii) Sunk costs and standard costs (2 Marks)