Knowledge from other ACCA exams

4 builds on the knowledge of organisational structure and the value chain from the SBL exam.

2 Introduction

In this we will look at the information and information system requirements of different business structures. We will also discuss the implications of a particular structure for performance management.

An important element of structure is business integration. Performance management can improve as a result of linkages between people, operations, strategy and technology. Section 7 of this reviews two important frameworks for understanding business integration; Porter’s value chain and McKinsey’s 7s model.

The then introduces the topic of business process re- engineering. This is the fundamental redesign of business processes and, amongst other things, it can result in a change of structure.

3 Organisational forms

3.1 Functional, divisional and network (virtual) structures

In the exam, you may be asked to discuss the particular information needs of an organisation adopting a functional, divisional or network structure and the implications of these structures for performance management.

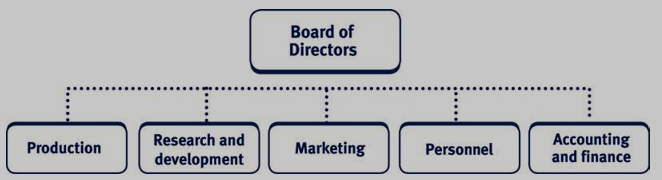

3.2 Functional structure

Functional organisations group together employees that undertake similar tasks into departments.

What is a functional structure?

- The organisation is divided into activities or functions.

- A manager is placed in charge of each function.

- A narrow band of senior management co-ordinates the functions and retains the authority to make most of the decisions, i.e. decision making tends to be centralised.

Information needs

The centralised structure results in:

- Data being passed from the functional level to the upper level.

- Data is then aggregated and analysed at the upper level for planning and control purposes.

- Feedback is then given at functional level.

Performance management

There are a number of advantages and disadvantages of a functional structure for performance management:

| Advantages | Disadvantages | |||||

| | Lower costs since roles are not | | Unsuitable for diversified or | |||

| duplicated. | growing organisations since it is | |||||

| | Better control due to | hard to assess the performance of | ||||

| an individual product or market. | ||||||

| standardisation of outputs/ | ||||||

| systems etc. | | Functional managers may make | ||||

| | Greater levels of employee | decisions that are good for | ||||

| themselves and their function but | ||||||

| motivation since specialists are | ||||||

| do not optimise organisational | ||||||

| grouped together so don’t feel | ||||||

| performance. | ||||||

| isolated and due to the defined | ||||||

| | ||||||

| career path that often exists | Decision making slow due to the | |||||

| within the function. | long chain of command. | |||||

| 164 | ||||||

3.3 Divisional structure

In a divisional structure the organisation is split into several divisions (sometimes referred to as strategic business units or subsidiaries) – each one autonomously overseeing a product or geographic region.

Information needs

The decentralised structure results in:

- Information being required lower down the hierarchy due to the high level of autonomy that exists.

- For example, information will be required by the divisions for budgeting purposes.

Implications for performance management

There are a number of advantages and disadvantages of a divisional structure for performance management:

| Advantages | Disadvantages | |||

| | Easier for an organisation to | | Inefficiencies due to duplication | |

| grow and diversify. | of functions. | |||

| | Easier to assess the performance | | Potential loss of goal congruence | |

| of individual products or markets. | if the division makes decisions | |||

| | There is clear responsibility for | that benefit itself to the detriment | ||

| of the overall organisation. | ||||

| the performance of each division. | ||||

| | Cost arising from development | |||

| | Performance management | |||

| and maintenance of appropriate | ||||

| systems can be tailored to meet | ||||

| information and control systems. | ||||

| divisional needs. | ||||

| | Difficult to set a transfer price to | |||

| | Top management should be free | |||

| fairly reflect the performance of | ||||

| to concentrate on strategic | ||||

| the divisions. | ||||

| matters. | ||||

Test your understanding 1

Company A is a diversified business with strategic business units (SBUs) in very different business areas. It is organised with each SBU being a separate division.

Company B is a multinational with different parts of the supply chain in different countries. It is also divisionalised.

Required:

Comment on the differences in performance management issues for each company.

3.4 Network (virtual) structures

A network (or virtual) organisation occurs when an organisation outsources many of its functions to other organisations and simply exists as a network of contracts, with very few, if any, functions being kept in-house.

Characteristics include:

- The organisation has little or no physical premises.

- Employees and managers work remotely (often from home) and are connected using IT such as emails, video conferencing, intranets and extranets.

- Suppliers and customers are linked using IT systems which can add to the impression that they all form part of the same organisation.

- The organisation appears to the outside world to be just like any traditional organisation.

Illustration 1 – Network structures

Amazon.com

Many internet companies are examples of networks – Amazon being perhaps one of the best known on-line retailers.

- Amazon operates its website but relies on external suppliers, warehouses, couriers and credit card companies to deliver the rest of the customer experience. Most orders placed on Amazon’s website are forwarded to suppliers, who then send the goods directly to the customer.

- These partners are also expected to provide Amazon with information on, for example, stock availability, delivery times and promotional material.

- The customer feels that they are dealing with one organisation, not many.

Information needs

With network structures, targeted information is needed to make decisions:

- Each party needs to have feedback as to how it is performing in relation to expectations and to others.

- Those responsible for regulating the performance of the organisation will also need information for decision making to enable them to make resource allocation decisions.

- Control is normally exercised via shared goals and, in the case of inter-organisational collaborations, contractual agreements.

Test your understanding 2

The idea of the network organisation emphasises:

- the decentralisation of control

- the creation of more flexible patterns of working

- a greater empowerment of the workforce

- the displacement of hierarchy by team working

- the development of a greater sense of collective responsibility

- the creation of more collaborative relationships among co-workers.

Required:

Comment on the importance of information to such an organisation.

Implications for performance management

Advantages:

- The organisation has the flexibility to meet the specific needs of a project.

- It can compete with large, successful organisations – they look and feel bigger than they are.

- It can assemble the components needed to exploit market opportunities.

- Lower costs, for example due to low investment in assets.

Disadvantages:

- It may be difficult to reach agreement over common goals and measures.

- Planning and control may be difficult – a traditional system of standard costing and variance analysis is less relevant since the core organisation does not need detailed information regarding the costs incurred by its business partners. Instead, they will require financial information (such as the prices that partners will charge) and non-financial information from partners (such as the quality of the goods/services, delivery times and ethical behaviour).

- This loss of control may result in a number of problems, for example a fall in quality or a greater/lesser degree of risk taking than would be desired.

- Confidentiality of information is a risk since the core organisation will share information with its partners (some of these partners may also work with competitor’ organisations).

- Monitoring of the workforce may be difficult since the core organisation will not employ many of the virtual organisation’s workforce and those that it does employ will often work remotely.

- It may be difficult to capture and share information if the systems are not integrated or are not compatible.

- Partners may work for competitors thus reducing competitive advantage. (The retention of the organisation’s core competencies in-house should help to minimise this issue).

Many of the problems identified above can be addressed through the use of a robust service level agreement (SLA). This is a negotiated, legal agreement between the core organisation and its partners regarding the level of service to be provided. It should include the following:

- An agreement of common goals and measures.

- Areas of responsibility should be identified. Action to be taken if KPIs are not met should be stated (for example, the use of fines).

- The activities expected of each partner together with the minimum standards expected, for example with regards to quality.

- A confidentiality agreement.

- An agreement of the standards and procedures to be adhered to by the workforce. It is worth noting that other actions outside those stated in the SLA may be used to effectively manage the workforce, for example the use of payment by results or the creation of cultural controls and a climate of trust.

- The information and reporting procedures to be followed. It is worth noting that the core organisation may put a common interface system in place to assist with information gathering.

Student accountant article: visit the ACCA website, www.accaglobal.com, to review the article on ‘complex business structures’.

- Information system requirements of different business structures

The information system requirements will be driven by the characteristics of the organisational structure. For example:

| Characteristics of organisation | Information system | |

| structure | ||

| Large, complex structure. | A sophisticated system will be | |

| necessary and beneficial and should | ||

| be cost effective. | ||

| High level of interaction between | System should aid communication | |

| business units. | between managers. | |

| Responsibility centres in place, | Management accounting systems | |

| i.e. the business is split into parts | should be designed to reflect the | |

| which are the responsibility of a single | responsibility structure in place and | |

| manager. The area of responsibility | ensure that costs and revenues can be | |

| may be a cost centre, profit centre or | traced to those responsible. Managers | |

| investment centre (see 9). | of responsibility centres will require: | |

| | the correct information | |

| | in the correct form | |

| | at the correct intervals. | |

Responsibility centres

Responsibility accounting is a system of accounting based upon the identification of individual parts of a business which are the responsibility of a single manager.

Budgetary control and responsibility accounting are inseparable.

- An organisation chart must be drawn up in order to implement a budgetary control system satisfactorily. It may even be necessary to revise the existing organisation structure before designing the system.

- The aim is to ensure that each manager has a well-defined area of responsibility and the authority to make decisions within that area, and that no parts of the organisation remain as ‘grey’ areas where it is uncertain who is responsible for them.

- This area of responsibility may be simply a cost centre, or it may be a profit centre (implying that the manager has control over sales revenues as well as costs) or an investment centre (implying that the manager is empowered to take decisions about capital investment for his department). Appropriate performance measures for such structures are discussed in later

- Once senior management have set up such a structure, with the degree of delegation implied, some form of responsibility accounting system is needed.

- Each centre will have its own budget, and the manager will receive control information relevant to that budget centre.

- Costs (and possibly revenue, assets and liabilities) must be traced to the person primarily responsible for taking the related decisions, and identified with the appropriate department.

- Some accountants would go as far as to advocate charging departments with costs that arise strictly as a result of decisions made by the management of those departments.

Management accounting systems should be designed to reflect the responsibility structure in place and ensure that costs and revenues can be traced to those responsible.

Controllability

The principal of controllability is very important in responsibility accounting. Whilst controllability refers mainly to costs, it is important to remember that its principles can also apply to revenues and investments.

- Controllability can depend on the time scale being considered.

– Over a long enough time-span, most costs are controllable by someone in the organisation.

– In the short-term some costs, such as rent, are uncontrollable even by senior managers, and certainly uncontrollable by managers lower down the organisational hierarchy.

- There may be no clear-cut distinction between controllable and non-controllable costs for a given manager, who may also be exercising control jointly with another manager.

- The aim under a responsibility accounting system will be to assign and report on the cost to the person having primary responsibility. The most effective control is thereby achieved, since immediate action can be taken.

- Some authorities would favour the alternative idea that reports should include all costs caused by a department, whether controllable or uncontrollable by the departmental manager. The idea here is that, even if he has no direct control, he might influence the manager who does have control.

5 Problems associated with complex business structures

Complex business structures may include those discussed in section 3

(i.e. divisional and network structures) but may also include structures such as:

- joint ventures

- strategic alliances

- franchising

- licensing

- multinationals and

- complex supply chains.

There are a number of problems in planning, controlling and measuring performance in these complex business structures. For example:

| Business structure | Problems in planning control | |||

| Joint venture (JV) – a separate | | In terms of measuring performance, | ||

| business entity whose shares are | the primary difficulty is establishing | |||

| owned by two or more business | the objectives of the JV. The different | |||

| entities. Useful for sharing costs, | partners may have different goals, risk | |||

| risks and expertise. | appetites and timescales. Hence a | |||

| large variety of performance | ||||

| measures will be required and there | ||||

| will have to be some agreement on | ||||

| common goals. | ||||

| | Attributing accountability for | |||

| performance is difficult since each JV | ||||

| partner will bring different skills and | ||||

| knowledge to the venture. This | ||||

| accountability should be established | ||||

| at the outset. | ||||

| | Reporting of joint profits/losses difficult | |||

| if partners are unwilling to share | ||||

| information or do not have an | ||||

| integrated system. | ||||

| | Quality, cost control and risk | |||

| management difficult if partners have | ||||

| different opinions. | ||||

| | The JV partners may be reluctant to | |||

| share too much information about | ||||

| their own business with the other JV | ||||

| partner. However, in order to succeed | ||||

| a climate of trust must exist which will | ||||

| rely on compatible management styles | ||||

| and cultures. | ||||

| 171 | ||||

| Strategic alliance – similar to a | Many of the difficulties above also apply but | ||

| joint venture but a separate | more specifically: | ||

| business entity is not formed. | | Independence is retained making it | |

| difficult to put common performance | |||

| measures in place and to collect and | |||

| analyse management information. | |||

| | Security of confidential information a | ||

| concern. | |||

| Multinationals – have | | Co-ordination of subsidiaries or | |

| subsidiaries or operations in a | operations to ensure they are working | ||

| number of countries. | towards the overall mission and | ||

| objectives can be difficult. | |||

| | Cultural, language, currency and time | ||

| zone differences may make planning | |||

| and control difficult. | |||

| | Measuring and reporting performance | ||

| may be difficult if common systems | |||

| don’t exist. | |||

| | Open to greater levels of uncertainty, | ||

| for example due to exchange rate | |||

| movements, changes in government | |||

| policy and recession. | |||

Question practice with additional assistance

The question below is taken from a past exam. It is an excellent test of your ability to add depth to your answer and to use the scenario since there is only one requirement worth 17 marks.

Additional guidance has been included within both the question and the answer. Take the time to read this guidance and use the advice given when attempting future questions.

This is an excellent question to learn from. Ensure that you attempt it and take time to review the answer before sitting the exam.

Test your understanding 3

Callisto Retail (Callisto) is an on-line reseller of local craft products related to the historic culture of the country of Callistan. The business started ten years ago as a hobby of two brothers, Jeff and George. The brothers produced humorous, short video clips about Callistan which were posted on their website and became highly popular. They decided to use the website to try to sell Callistan merchandise and good initial sales made them believe that they had a viable business idea.

Callisto has gone from strength to strength and now boasts sales of $120m per annum, selling anything related to Callistan. Callisto is still very much the brothers’ family business. They have gathered around themselves a number of strategic partners into what Jeff describes as a virtual company. Callisto has the core functions of video clip production, finance and supplier relationship management. The rest of the functions of the organisation (warehousing, delivery and website development) are outsourced to strategic partners.

The brothers work from their family home in the rural North of Callistan while other Callisto employees work from their homes in the surrounding villages and towns. These employees are involved in video editing, system maintenance, handling customer complaints and communication with suppliers and outsourcers regarding inventory. The employees log in to Callisto’s systems via the national internet infrastructure. The outsourced functions are handled by multinational companies of good reputation who are based around the world. The brothers have always been fascinated by information technology and so they depend on email and electronic data interchange to communicate with their product suppliers and outsourcing partners.

Recently, there have been emails from regular customers of the Callisto website complaining about slow or non-delivery of orders that they have placed. George has commented that this represents a major threat to Callisto as the company operates on small profit margins, relying on volume to drive the business. He believes that sales growth will drive the profitability of the business due to its cost structure.

Jeff handles the management of outsourcing and has been reviewing the contracts that exist between Callisto and its strategic partner for warehousing and delivery, RLR Logistics. The current contract for warehousing and delivery is due for renewal in two months and currently, has the following service level agreements (SLAs):

- RLR agree to receive and hold inventory from Callisto’s product suppliers.

- RLR agree to hold 14 days inventory of Callisto’s products.

- RLR agree to despatch from their warehouse any order passed from Callisto within three working days, inventory allowing.

- RLR agree to deliver to customers anywhere in Callistan within two days of despatch.

Breaches in these SLAs incur financial penalties on a sliding scale depending on the number and severity of the problems. Each party to the contract collects their own data on performance and this has led to disagreements in the past over whether service levels have been achieved although no penalties have been triggered to date. The most common disagreement arises over inventory levels held by RLR with RLR claiming that it cannot be expected to deliver products that are late in arriving to inventory due to the product suppliers’ production and delivery issues.

Required:

Assess the difficulties of performance measurement and performance management in complex business structures such as Callisto, especially in respect of the performance of their employees and strategic partners.

(Total: 17 marks)

Question assistance

Step 1 – Review the requirements

Assessment = is an alternative to ‘evaluate’ where both pros and cons are needed and final judgement on their balance is required.

Performance measurement AND performance management – so need to go further than just the measures and think about how to improve performance.

‘Complex business structures such as Callisto’ – what constitutes a complex business structure and how does Callisto meet this definition?

Ensure employees and strategic partners are specifically addressed.

Step 2 – Review scenario for relevant information relating to requirements

Examples here include:

- ‘on-line reseller’

- ‘They have gathered around themselves a number of strategic partners into what Jeff describes as a virtual company’

- ‘The rest of the functions of the organisation (warehousing, delivery and website development) are outsourced to strategic partners’

- ‘The employees log in to Callisto’s systems via the national internet infrastructure’

- ‘outsourced functions are handled by multinational companies of good reputation’

- ‘so they depend on email and electronic data interchange to communicate with their product suppliers and outsourcing partners’

- ‘complaining about slow or non-delivery of orders’

- ‘the company operates on small profit margins’

- The current contract for warehousing and delivery is due for renewal in two months’

- ‘Each party to the contract collects their own data on performance and this has led to disagreements in the past’.

Step 3 – Plan the answer

You need to plan your answer identifying sufficient points for each part of the requirement. Use headings to structure your plan – this will help you keep focused when you write your answer.

Difficulties for Performance Measurement

- Employees

- Strategic partners.

For each heading you need to be identifying the difficulties for a virtual organisation (the ‘textbook’ answer) and combine this with relevant examples and information regarding Callisto. Both of these elements are essential for your answer otherwise you are either just describing the scenario or merely repeating textbook content.

Step 4 – Check requirements

Quick recap of requirements – have you covered everything?

Step 5 – Write your answer

Use space, headings and short paragraphs to clearly signpost to the marker that you have covered all the necessary parts. If you have planned properly this will be the easiest part of the whole question.

6 The needs of modern service industries

6.1 Introduction

Although not strictly a type of structure, it makes sense to look at service industries as part of this .

Traditional manufacturing companies have been replaced by modern service industries, e.g. insurance, management consultancy and professional services.

The differences between the products of manufacturing companies and those of service businesses:

- can create problems in measuring and controlling performance and

- this, in turn, affects the information needs of service organisations.

3 Measuring service quality

Service providers do not have a physical product so base competitive advantage on less tangible customer benefits such as:

- soundness of advice given

- attitude of staff

- ambience of premises

- speed of service

- flexibility/responsiveness

- consistent quality.

Test your understanding 4

Required:

State the performance measures that may be used in order to assess the surgical quality provided by a hospital indicating how each measure may be addressed.

7 Business integration

7.1 What is business integration?

An important aspect of business structure is business integration.

Business integration means that all aspects of the business must be aligned to secure the most efficient use of the organisation’s resources so that it can achieve its objectives effectively.

Rather than focusing on individual parts of the business in isolation, the whole process from the initial order to final delivery of the product and after sales service needs to be considered.

Hammer and Davenport

Modern writers such as Hammer and Davenport argue that many organisations have departments and functions that try to maximise their own performance and efficiency at the expense of the whole.

Their proposed solution is twofold:

- Processes need to be viewed as complete entities that stretch from initial order to final delivery of a product.

- IT needs to be used to integrate these activities.

Four aspects in particular need to be linked:

- people

- operations

- strategy

Test your understanding 5

Required:

XYZ has a conventional functional structure. Assess how many different people in the organisation may have to deal with customers, and the problems this creates.

There are two frameworks for understanding integrated processes and the linkages within them:

- Porter’s value chain model.

- McKinsey’s 7S model.

7.2 Porter’s value chain

The value chain model is based around activities rather than traditional functional departments (such as finance). It considers the organisation’s activities that create value and drive costs and therefore the organisation should focus on improving those activities. The activities are split into primary ones (the customer interacts with these and can ‘see’ the value being created) and secondary (or support) activities which are necessary to support the primary activities.

Margin, i.e. profit will be achieved if the customer is willing to pay more for the product/service than the sum of the costs of all the activities in the value chain.

Illustration 2 – Value chain activities

Primary Description

activity

Inbound Receiving, storing and

logistics handling raw material

inputs

Operations Transformation of raw

materials into finished

goods and services

Outbound Storing, distributing

logistics and delivering finished

goods to customers

Marketing and Market research and

sales the marketing mix

(product, price, place,

promotion)

After sales All activities that occur

service after the point of sale,

such as installation,

training and repair

Secondary Description

(support)

activity

Firm How the firm is

infrastructure organised

Technology How the firm uses

development technology

Human How people contribute

resource to competitive

management advantage

Procurement Purchasing, but not

just limited to

materials

Example

- just-in-time stock system could give a cost advantage (see 13)

Using skilled craftsmen could give a quality advantage

Outsourcing activities could give a cost advantage

Sponsorship of a sports celebrity could enhance the image of a product

A flexible approach to customer returns could enhance a quality image

Example

Centralised buying could result in cost savings due to bulk discounts

Modern computer-controlled machinery gives greater flexibility to tailor products to meet customer specifications

Employing expert buyers could enable a supermarket to purchase better wine than their competitors

Buying a building out of town could give a cost advantage over High Street competitors

Illustration 3 – Value chain

Value chain analysis helps managers to decide how individual activities might be changed to reduce costs of operation or to improve the value of the organisation’s offerings. Such changes will increase margin.

For example, a clothes manufacturer may spend large amounts on: buying good quality raw materials (inbound logistics) hand-finishing garments (operations)

building a successful brand image (marketing)

running its own fleet of delivery trucks in order to deliver finished clothes quickly to customers (outbound logistics).

All of these should add value to the product, allowing the company to charge a premium for its clothes.

Another clothes manufacturer may:

- reduce the cost of its raw materials by buying in cheaper supplies from abroad (inbound logistics)

- making all its clothes using machinery that runs 24 hours a day (operations)

- delaying distribution until delivery trucks can be filled with garments for a particular location (outbound logistics).

All of these should enable the company to gain economies of scale and to sell clothes at a cheaper price than its rivals.

Evaluation of the value chain

Advantages of the value chain model

- Particularly useful for focusing on how each activity in the process adds to the firm’s overall competitive advantage.

- Emphasises CSFs within each activity and overall.

- Examines both primary activities (e.g. production) and support activities, such as HRM, which may otherwise be dismissed as overheads.

- Highlights linkages between activities.

Disadvantages of the value chain model

- It is more suited to a manufacturing environment and can be hard to apply to a service provider.

- It is intended as a quantitative analysis tool but this can be time consuming since it often requires recalibrating the system to allocate costs to individual activities.

Test your understanding 6

Many European clothing manufacturers, even those aiming at the top end of the market, outsource production to countries with lower wage costs such as Sri Lanka and China.

Required:

Comment on whether you feel this is an example of poor integration (or poor linkage in Porter’s terminology).

Uses in performance management

- Used as part of strategic analysis to identify strengths or weaknesses and to focus on how each activity does or could add to the firms competitive advantage.

- Used for ongoing performance management. It emphasises the CSFs within each activity and targets can then be set and monitored in relation to these.

- In addition to examining primary activities (for example, production) it looks at support activities (for example, HRM), which may have otherwise have been dismissed as overheads.

- It highlights the linkages between activities. The idea of a chain is important. Value will be created by linking activities and hence:

– information systems should allow the free flow of information between activities and across departmental boundaries.

– job descriptions and reporting hierarchies should reflect activities.

Test your understanding 7

Kudos Guitar Amplifiers (KGA)

Kudos Guitar Amplifiers (KGA) was set up by Phil Smith two years ago in the UK. Phil, an electrical engineer and musician, started repairing and then building guitar amplifiers for himself and friends. Initially Phil based his amplifiers around existing classic circuits but soon discovered a potential to tweak these to produce modern variations and improved tones. Partly as a result of the excellent sound but also the low prices compared to established brands, Phil soon found himself inundated with requests and so started the business and employed more staff.

The big break came when a number of high profile professional musicians started using KGA amplifiers. Despite operating in a highly competitive market sector, Phil has struggled to meet demand since and has waiting lists for the hand-built, top of the range models, even having increased prices considerably.

Phil is looking to expand the business further, extend the range of products offered to include cheaper models and look to sell into additional markets. He has recruited more staff, built a state of the art, dedicated factory and appointed managers. To ensure the longevity of his business Phil commissioned a strategic consultant who advised him to adopt a competitive strategy of differentiation.

Extracts from the value chain analysis produced by the consultant are as follows:

- Inbound logistics

As well as Phil’s proprietary circuit designs, part of the sound of KGA amplifiers comes from the use of rare “new old stock” (NOS) components, some originally manufactured in the 1960s. Locating sufficient numbers of such components to the required quality is a major challenge and it is felt that KGA’s relationship with two key suppliers is vital.

- Operations

The top of the range models are hand built by master craftsmen with point to point wiring and specialist components. Given normal variations in some of these, different elements are tested and matched by ear to optimise tonal characteristics. Extensive quality control tests are done before an amplifier is ready for sale. Newer, cheaper models use pre-assembled circuit boards bought from a SE Asian supplier.

The factory also uses “clean room” technologies and fume extraction safety processes that far exceed current industry requirements and add to the factory running costs.

- Outbound logistics

Originally selling direct to customers, Phil has now agreed distribution contracts with two national UK retailers and is hoping to secure similar deals in Germany and the USA.

- Marketing and sales

Marketing currently consists of word of mouth, advertising in guitar magazines and sponsorship of high profile musicians. The company will also be setting up a website and Facebook page. It is felt that continued publicity from famous guitarists and online exposure are vital to achieving growth targets.

The new ranges have the same brand name as the original hand-built products.

- Service

Phil offers a lifetime warranty on his top of the range amplifiers with a guaranteed turnaround of 5 days, although he did have a problem repairing an amplifier in time for a rock band headlining at a major festival. Cheaper ranges have an industry standard 12 months’ warranty.

Required

Identify the performance management issues arising from the above analysis.

Value system

More recently, organisations have started to consider supply chain partnerships. The value system looks at linking the value chains of suppliers and customers to that of the organisation. A firm’s performance depends not only on its own value chain, but on its ability to manage the value system of which it is part.

Illustration 4

In 2 we looked at an illustration on the UK supermarket giant, Tesco and its high wastage levels of products such as bagged salads. Tesco’s ‘farm to fork’ methodology has engaged with producers, suppliers and customers to collect data on the levels and causes of food waste and to give an overall waste ‘footprint’ for a selection of products. This has shown where waste ‘hotspots’ have occurred and has enabled Tesco to develop a waste reduction action plan and targets for each product. For example, ‘display until’ dates have been removed from fruit and vegetables.

This emphasis on reduced wastage should help Tesco to cut costs and should contribute to meeting its objective of being a socially responsible retailer.

7.3 McKinsey’s 7s model

The McKinsey 7S model describes an organisation as consisting of seven interrelated internal elements.

A change in one element will have repercussions on the others. All seven elements must be aligned to ensure organisational success.

McKinsey’s 7S model

There are three hard elements of business behaviour

- Strategy – what will the company do?

- Structure – how should it be organised?

- Systems – what procedures need to be in place (few or many)?

Hard elements are easier to define or identify and management can directly influence them.

There are four soft elements.

- Staff – what staff will we require?

- Style – what management style will work best?

- Shared values – what culture (attitudes) will be most suitable?

- Skills – what skills will our staff/company need?

Soft elements are more difficult to describe, less tangible and are more influenced by culture.

8 Business Process Re-engineering (BPR)

8.1 What is BPR?

The discussion of BPR follows on from the value chain. As discussed, the value chain shows the way in which the various activities of an organisation work together to add value. The ways these activities function and interrelate constitute an organisation’s processes. This process perspective is the emphasis of BPR.

BPR is the fundamental rethinking and radical redesign of business processes to achieve dramatic improvements in critical, contemporary measures of performance, such as cost, quality, service and speed. Improved customer satisfaction is often the primary aim.

Illustration 5 – IBM and BPR

Prior to re-engineering, it took IBM Credit between one and two weeks to issue credit, often losing customers during this period.

- On investigation it was found that performing the actual work only took 90 minutes. The rest of the time (more than seven days!) was spent passing the form from one department to the next.

- The solution was to replace specialists (e.g. credit checkers) with generalists – one person (a deal ‘structurer’) processes the entire application from beginning to end.

- Post re-engineering, the process took only minutes or hours.

Test your understanding 8

A business process is a series of activities that are linked together in order to achieve given objectives. For example, materials handling might be classed as a business process in which the separate activities are scheduling production, storing materials, processing purchase orders, inspecting materials and paying suppliers.

Required:

Suggest ways in which materials handling might be re-engineered.

8.2 The influence of BPR on the organisation

BPR cuts across traditional departmental lines in order to achieve more efficient delivery of the final product.

- This change to a process view will require a change in culture with a move towards process teams rather than functional departments.

- Employees will need to retrain in order to gain additional skills.

- The change will require much communication and leadership from senior management as a result.

- BPR results in more automation and greater use of IT/IS to integrate processes. The rise of BPR in the 1990s coincided with the widespread adoption of new IT systems based on personal computers, networks and the internet.

8.3 Does BPR improve organisational performance?

Advocates of BPR would argue that organisational performance will improve:

- BPR encourages a long-term strategic view by asking questions about how core processes can be honed in order to achieve corporate goals more effectively.

- BPR revolves around customer needs; the fulfilment of which is vital for sustaining competitive advantage.

- BPR can help reduce organisational complexity by eliminating unnecessary activities.

- A process should be made cheaper and more responsive to customer needs by stripping away the peripheral activities and bureaucratic layers that sometimes emerge from excessive focus on functional boundaries.

However, the approach does have a number of weaknesses which may make it ill-suited to an organisation today. BPR often produced a quick fix to perceived problems but at a long-term cost. Practical problems include:

- A decline in morale due to staff cuts and a perception that BPR is all about cost cutting.

- Staff may feel devalued when their current role is fundamentally changed with a re-organisation into new teams with different goals and expectations.

- BPR often strips out different layers of middle management. This may lead to a loss of co-ordination and communication.

- BPR often utilised outsourcing; farming out business processes and elements of production. However, this sometimes had adverse consequences on quality and flexibility.

- In many cases, business processes were not redesigned but merely automated.

Numerous organisations have attempted to redesign their business processes but have failed to enjoy the enormous benefits promised. It is now widely accepted that BPR may be a backward-looking approach. It takes what has happened in the past and seeks to improve it, but with limited regard for what will happen in the future.

8.4 The influence of BPR on systems development

Remember ‘what gets measured gets done’. Therefore, the systems will have to be redesigned to capture new performance measurement data, focusing on factors such as:

- quality

- innovation

- ability to work as a team

- on time delivery.

It is also said that ‘what gets rewarded gets repeated’ so the reward system (for example, the payment of a bonus) should be aligned to these new measures. The basic part of the remuneration may also increase to reflect the increased skills base, autonomy and responsibility of employees.

- The impact of a change in structure, culture and strategy on performance measurement

A change in organisational structure, culture or strategy may result in a requirement for new performance measurement techniques and methods:

| Organisational change | Examples of impact on performance | |

| measurement | ||

| Structure | | Highly centralised and/or functional structures |

| will require a performance measurement | ||

| system that enables data to be collected at | ||

| functional level, analysed at the upper level | ||

| and then fed back to the functional levels. | ||

| These structures tend to inhibit a manager’s | ||

| discretion to try out new performance | ||

| measurement techniques. | ||

| | A task centred and/or decentralised structure | |

| will require a performance measurement | ||

| system that allows data to be collected and | ||

| analysed lower down the hierarchy. | ||

| Managers will have more discretion to try out | ||

| new performance measurement techniques. | ||

| Culture | | An innovative or creative culture will be |

| willing to embrace new performance | ||

| measurement techniques. Measurement | ||

| techniques will need to focus on the | ||

| performance of the innovations. | ||

| | A restrictive, bureaucratic culture will be less | |

| open to the adoption of new performance | ||

| measurement techniques. | ||

| Strategy | | The performance measurement techniques |

| adopted should be aligned to the strategy the | ||

| organisation is pursuing. | ||

| | For example, an organisation that focuses on | |

| quality and has adopted a TQM approach will | ||

| need performance measures that focus on | ||

| factors such as the quality of the product or | ||

| service, the cost of prevention and speed of | ||

| response (quality is discussed in 13). | ||

10 Exam focus

| Exam sitting | Area examined | Question | Number |

| number | of marks | ||

| Mar/June 2016 | BPR | 2 | 25 |

| June 2015 | Value chain | 1(v) | 6 |

| June 2014 | BPR | 2(a)(b) | 17 |

| June 2014 | Complex business structures | 3(c) | 8 |

| June 2013 | Differences between services and | 1(i) | 5 |

| manufacturing organisations | |||

| June 2013 | Change in divisional structure | 4(c) | 9 |

| June 2012 | Performance management and | 5 | 17 |

| measurement in complex business | |||

| structures | |||

| June 2012 | Complex business structures | 5 | 17 |

Test your understanding 1

Company A

- Given that business units are in unrelated markets, there is likely to be more devolved management, with the use of divisional performance measures and reliance on the measurement systems, particularly financial reporting, for control.

Company B

- There is a need for a high level of interaction between business units, so senior management control is more important, whether in terms of standardisation or detailed operational targets.

- The performance measurement system may aid communication between managers and provide a common language.

Test your understanding 2

Information is key to a successful network organisation:

- This is mainly through the systems that facilitate co-ordination and communication, decision making and the sharing of knowledge, skills and resources.

- Information systems can reduce the number of levels in the organisation by providing managers with information to manage and control larger numbers of workers spread over greater distances and by giving lower-level employees more decision-making authority.

- It is no longer necessary for these employees to work standard hours every day, nor work in an office or even the same country as their manager. With the emergence of global networks, team members can collaborate closely even from distant locations. Information technology permits tight co-ordination of geographically dispersed workers across time zones and cultures.

Test your understanding 3

Tutor tip: Splitting your answer into the measurement and

management sections is a good start. You can break it down further by separating employees, strategic partners and other issues.

Performance measurement problems at Callisto

In a virtual organisation such as Callisto, performance measurement can be difficult due to the fact that key players in the business processes and in the supply chain are not ‘on site’. Callisto has the problem of collecting and monitoring data about its employees working from home and the outsourcing partners.

Tutor tip: This identifies the key issue relating to the ‘virtual’ nature of a company like Callisto.

At Callisto, there is a reliance placed on information technology for handling these remote contacts. Collecting and monitoring performance should therefore be done automatically as far as possible. A large database would be required that can be automatically updated from the activities of the remote staff and suppliers. This will require the staff and supplier systems to be compatible.

Tutor tip: Another specific issue relating to virtual organisations that

has been linked to information regarding Callisto. This paragraph goes further than just identifying the issue and explains the implications.

Employees

The employees can be required to use software supplied by Callisto and in fact, at Callisto, they use the internet to log in remotely to Callisto’s common systems. Although this solution requires expenditure on hardware and software, it is within the control of Callisto’s management.

Tutor tip: Part of ‘assessing’ the difficulty may involve explaining why it is not too much of an issue – so here identifying the fact that Callisto still have control over their employees.

Even with reviews of system logs to identify the hours that staff spend logged in to the systems, there is still the difficulty of measuring staff outputs in order to ensure their productivity. These outputs must be clearly defined by Callisto’s managers, otherwise there will be disputes between staff and management.

Tutor tip: Again, the implication of the problem has been described.

One further outstanding issue is the need to ensure that such communication is over properly secured communication channels, especially if it contains customer or financial data. There are likely to be significant penalties if data protection regulations are breached, not to mention the reputational impact.

Strategic partners

The strategic partners, such as RLR, will have their own systems. A problem for Callisto is that there is disagreement over the measurement of the key SLAs. In order to resolve such disputes, lengthy reconciliations between Callisto’s and RLR’s systems will have to be undertaken otherwise there are no grounds for enforcement of the SLAs and the SLAs represent Callisto’s key control over the relationship.

Tutor tip: The implication has been explained with specific reference to information in the scenario. This ensures your answer is not just a generic ‘textbook’ answer.

The solution would be for the partners to agree a standard reporting format for all data that relates to the SLAs which would remove the need for such reconciliations.

Tutor tip: Part of ‘assessing’ a difficulty may involve thinking about how it can be resolved.

Finally, there is the problem that Callisto and the partner organisation may have differing objectives – the obvious conflict over price between supplier and customer being one. However, at Callisto, this is being addressed by the use of detailed SLAs which both organisations can use to develop performance measures such as inventory levels and delivery times.

Performance management problems at Callisto

Tutor tip: Performance management goes a step further than merely measuring output and considers how improvements can be made.

Employees

The performance management of employees is complicated due to the inability of management to ‘look over their shoulder’ since they are not present in the same building. However, employees will enjoy the advantages of home-working, such as lower commuting times, more contact with family and greater flexibility in working hours. The disadvantages are the difficulties in measuring outputs mentioned above and ensuring motivation and commitment.

Tutor tip: This nicely combines an identification of the problem, the implications of the problem along with an upside to the situation.

The motivation and commitment can be addressed through suitable reward schemes which would have to be tied to agreed outputs and targets for each employee. Work could be divided into projects where the outputs are more easily identified and pay and bonuses related to these.

Tutor tip: Further assessment of the problem considers the possible solutions.

Strategic partners

When managing the performance of the strategic partners it is crucial that there is a balance between consideration of security and control issues and encouraging a positive and collaborative relationship.

Tutor tip: This introduces the difficulty faced regarding performance management of strategic partners.

One difficulty which may arise concerns confidentiality as the partners will have access to commercially sensitive information about customers’ locations and suppliers’ names and lead times. Callisto must control access to this information without affecting the relationship. Leakage of such data will have a detrimental effect on the company’s reputation. However interface between the organisations can create wasteful activity if there is not an atmosphere of trust. At Callisto, this is illustrated by the problem of reconciliation of performance data.

Tutor tip: The problem is further explained and the possible implications considered.

It is also important to consider reliability where the partner is supplying a business critical role (as for RLR with Callisto) such that it would take considerable time to replace such a relationship and affect customer service while this happened.

Finally Callisto must carefully consider profit sharing. The collaborative nature of the relationship and the difficulty of breaking it combine to imply that it will be in the interest of both parties to negotiate a contract that is motivating and profitable for both sides. For Callisto, the business aim is to increase volume and this will require customer loyalty so the quality of service is important.

Tutor tip: The ‘difficulty’ identified here is how to determine the appropriate split of profit between Callisto and its partners.

Test your understanding 4

- The percentage of satisfied patients which could be measured by using the number of customer complaints or via a patient survey.

- The time spent waiting for non-emergency operations which could be measured by reference to the time elapsed from the date when an operation was deemed necessary until it was actually performed.

- The number of successful operations as a percentage of total operations performed which could be measured by the number of remedial operations undertaken.

- The percentage of total operations performed in accordance with agreed schedules which could be measured by reference to agreed operation schedules.

- The standards of cleanliness and hygiene maintained which could be measured by observation or by the number of cases of hospital bugs such as MRSA.

- The staff to patient ratio which could be measured by reference to personnel and patient records.

- The responsiveness of staff to requests of patients which could be measured via a patient survey.

Test your understanding 5

- Sales staff to make the original sale.

- Delivery staff to arrange delivery.

- Accounts staff chasing up payment if invoices are overdue.

- Customer service staff if there is a problem with the product. Possible problems include:

- delivery staff may be unaware of any special delivery requirements agreed by the sales staff

- accounts staff may be unaware of any special discounts offered

- aggressive credit controllers could damage sales negotiations for potential new sales

- credit controllers might not be aware of special terms offered to the client to win their business

- customers may resent having to re-explain their circumstances to each point of contact

- customer service may be unaware of the key factors in why the client bought the product and hence not prioritise buying.

Customer service could be improved by having one customer-facing point of contact.

Test your understanding 6

Firms following a cost leadership strategy have found that outsourcing to China, say, has cut costs considerably, even after taking into account distribution costs.

Differentiators have, on the whole, found that they have saved costs without compromising quality. Thus the apparent conflict between low cost production and high quality branding has not been a problem. Furthermore the perceived quality of Chinese garments is rising with some manufacturers claiming that quality is higher than in older European factories.

Note: Commercial awareness – given that many firms do it, be wary of criticising the approach too heavily! They must have their reasons.

Test your understanding 7

Introduction

Generally, the value chain is a model of business integration showing the way that business activities are organised. This model is based around activities rather than traditional functional departments (such as finance). A key idea is that it is activities which create value and incur costs. The activities are split into two groups: primary ones which the customer interacts with directly and can ‘see’ the value being created and secondary ones which are necessary to support the primary activities. By identifying how value is created, the organisation can then focus on improving those activities through its performance measurement system.

Context – competitive strategy (note: this aspect of the analysis has

considerable overlap with the SB: case study)

If KGA is going to adopt a strategy of differentiation as recommended, then it needs to ensure that all aspects of the value chain are coordinated to support this.

In particular the following issues are relevant:

- There is a risk that the cheaper range could undermine the brand perception as the inherent quality will be lower than the hand-built models. Whether this is a significant risk is unclear as the cheaper models may still offer exceptional sound quality compared to rival products within their price range. If there is a risk, then it might be worth considering using a different brand strategy for them.

- Non value-added activities should be discontinued. In particular, excessive spending on clean room and extraction processes seems unnecessary as it does not add to the perceived quality of the amplifiers and does not appear to be valued by customers.

- Activities that are vital for the high sound quality – sourcing NOS components, being hand built and tested by craftsmen and the publicity gained from being used by famous guitarists – need to be strengthened and consolidated.

Performance management – establishing CSFs and KPIs

Based on the above analysis, KGA will need to establish a system of

CSFs and KPIs, which could include the following:

| CSF | Comment | KPIs | ||

| Securing | The NOS components | | Number of each | |

| sufficient | are a vital part of the final | component in stock | ||

| volumes of | sound quality for the | | % returns back to | |

| high quality | hand built amplifiers. | |||

| suppliers due to quality | ||||

| NOS | ||||

| problems | ||||

| components | ||||

| | Lead times by | |||

| component and | ||||

| supplier | ||||

| Ensuring | KGA’s success is | | % rejected by quality | |

| build and | underpinned by the | control | ||

| sound | sound quality of its | | % requiring reworking | |

| quality of top | amplifiers. If this suffers | |||

| or repair | ||||

| of the range | for any reason then | |||

| | Average scores in | |||

| amplifiers | customers will by | |||

| competitors’ offerings | online reviews | |||

| instead. | | Staff turnover of | ||

| master craftsmen | ||||

| Meeting | Many customers are | | Turnaround time on | |

| sponsored | drawn to KGA products | repairs and servicing | ||

| guitarists’ | because they see guitar | | No (%) of returns | |

| needs | heroes using the | |||

| | Time taken to build | |||

| products. If these guitar | ||||

| players chose to use | new equipment for | |||

| different brands then | them | |||

| sales would drop and the | ||||

| brand be undermined. | ||||

| 4 | ||||||||

| Effective | The website is seen as | | No of hits | |||||

| website | key to new growth. | | Average length of visit | |||||

| sales and | ||||||||

| | % of hits that translate | |||||||

| marketing | ||||||||

| into sales | ||||||||

| | Average purchase | |||||||

| value | ||||||||

| | % down time | |||||||

Performance management – MIS issues

Another feature of the value chain is the idea of a chain. This is the thought that value is built by linking activities and so there must be a flow of information between the different activities and across departmental boundaries. In performance management terms, this will affect:

- information systems which will have to ensure good communication across functional boundaries and

- job descriptions and reporting hierarchies as these will have to reflect activities.

The chain does not stop at the organisation’s boundaries. This is likely to be obvious to KGA given the importance of supply chain management but the value chain will allow the organisation to focus on those relationships on which value most depends.

Specifically for KGA, the value chain would emphasise the importance of supplier management to obtain suitable NOS components, leading through to operations in the form of testing and matching components, resulting in finished amplifiers.

Test your understanding 8

In the case of materials handling, the activity of processing purchase orders might be re-engineered by:

- integrating the production planning system with that of the supplier (an exercise in supply chain management (or SCM)) and thus sending purchase orders direct to the supplier without any intermediate administrative activity

- joint quality control procedures might be agreed thus avoiding the need to check incoming materials. In this manner, the cost of material procurement, receiving, holding and handling is reduced.