TUESDAY: 6 December 2022. Afternoon Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Do NOT write anything on this paper.

QUESTION ONE

1. Describe how the following factors could affect an individual investor’s risk tolerance:

Source of wealth. (1 mark)

Measure of wealth. (1 mark)

Stage of life. (1 mark)

2. Capital market expectations are the essential inputs to deciding on a strategic asset allocation.

In relation to the above statement, identify the SEVEN steps involved in the process of capital markets expectations setting. (7 marks)

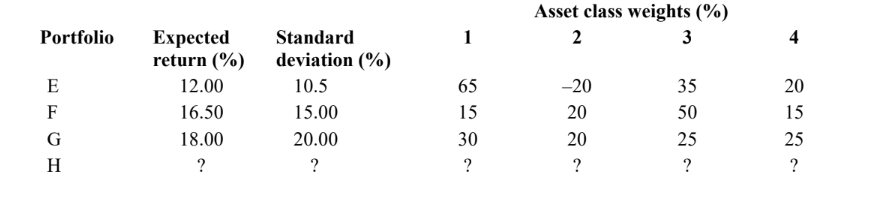

3. XYZ is an investments practitioner and is analysing Elimu Msingi endowment fund with Sh.20 million in assets.

The fund has a targeted spending rate of 4.5%. The fund has been incurring 0.75% as management costs.

The trustees would like to preserve the purchasing power of the fund and curtail the risk in terms of standard deviation to no more than 10%. Inflation expectation for the coming year is 2%.

Additional information:

1. XYZ is considering the following domestic investments to recommend to Elimu Msingi Board of trustees for incorporation into their investment portfolio:

The risk free rate applicable for these investments is 3% and XYZ estimates Elimu Msingi to be moderately risk averse with a numerical ranking of 5.

2. XYZ identifies further foreign investment opportunities presented by various portfolios listed below:

Required:

Determine Elimu Msingi’s endowment fund required rate of return. (1 mark)

Advise XYZ on the most appropriate domestic investment to recommend to the Board of trustees of Elimu Msingi using the utility adjusted rate of return. (5 marks)

Given that portfolio H is composed of 35% of portfolio E and 65% of portfolio F, determine the optimal asset class weights in portfolio H. (4 marks)

(Total: 20 marks)

QUESTION TWO

1. Describe THREE primary portfolio rebalancing strategies. (6 marks)

2. Daniel Menzo who is 35 years old has recently retired from playing football. He is meeting with his portfolio manager to update his investment policy statement (IPS):

Income

He will receive an annual pension of Sh.1,000,000 before tax in the coming year. In future years, this amount will

be indexed for inflation which is expected to be 5% per year. The pension is taxed at 30%.

Expenses

His living expenses over the previous twelve months were Sh.1,200,000. He expects these expenses will grow at the expected rate of inflation this year and in each future year.

Assets

In addition to his pension payments, his investment portfolio is currently valued at Sh.15 million. Next month, he wants to make a direct equity real estate investment of Sh.1,000,000 in a junior school sports training facility. He also anticipates that he will receive a performance cash bonus of Sh.3,500,000 which will be immediately invested in his portfolio. This bonus and all investment returns are taxed at 30%.

Goals

Daniel wants his portfolio to fund any expenses not covered by his pension, while maintaining its real value over time. He is eager to consider investments in more risky asset classes. He is not concerned about volatility in the value of his portfolio as long as it continues to support his living expenses. He does not intend to seek further employment in retirement.

Required:

Calculate Daniel’s nominal after tax required rate of return for the coming year. (8 marks)

Identify FOUR factors that indicate Daniel has a high ability to take risk. (4 marks)

Formulate the time horizon and unique circumstances constraints section of Daniel’s IPS. (2 marks)

(Total: 20 marks)

QUESTION THREE

1. Describe TWO spread duration measures used for fixed rate bond. (4 marks)

2. An investor gathers the following information relating to Kimbo shares listed at the securities exchange:

• On Wednesday, the shares closed the day at Sh.40 per share.

• On Thursday morning before market open, the investor decides to buy Kimbo Ltd.’s shares and transfers a limit order for Sh.39.95 per share for 1,000 shares. The price never falls to Sh.39.95 during the day and the order expires unfilled. The shares closes the day at Sh.40.04 per share.

• On Friday, the order is revised to limit of Sh.40.05. The order is partially filled that day as 700 shares are bought at Sh.40.05. The commission is Sh.17. The share closes at Sh.40.08 and the order is cancelled.

Required:

Calculate the following:

Explicit cost of trade. (1 mark)

Realised profit or loss. (1 mark)

Delay cost. (1 mark)

Missed trade opportunity costs. (1 mark)

Implementation shortfall. (2 marks)

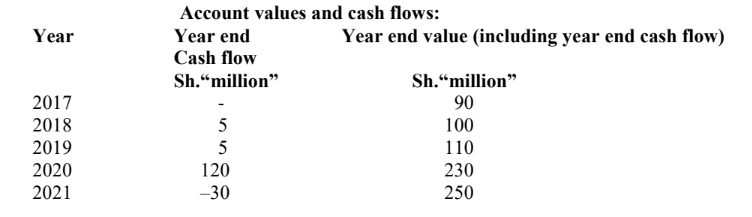

3. Silvester Onyango, a high net worth (HNW) investor has approached Antony Makau, an independent financial consultant to review the performance of his investment account over the past four years. The account is managed by

an external portfolio manager, but Silvester Onyango has full control over the timing and the size of the cash flows

being invested into and withdrawn from the account.

Required:

The annualised time weighted rate of return (TWRR). (4 marks)

The annualised money weighted rate of return (MWRR). (4 marks)

Advise on the most appropriate return measure for use in evaluating the external portfolio manager’s investment performance. (2 marks)

(Total: 20 marks)

QUESTION FOUR

1. Assess THREE potential sources of excess return for an international bond portfolio. (6 marks)

2. Explain THREE guiding principles that firms should consider while applying the global investment performance

standards (GIPS) to wrap fee portfolios. (6 marks)

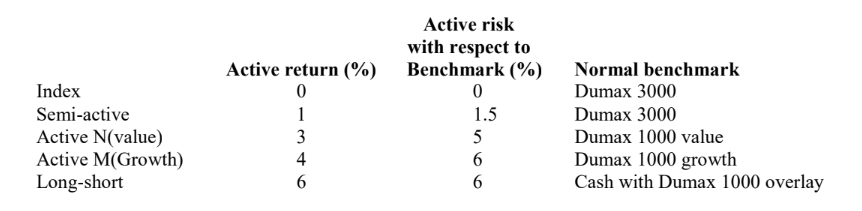

3. Caroline Wesula is evaluating several alternatives for the Ugandan equity portfolio of her company’s pension plan

involving the following managers:

Additional information:

1. Active versus misfit risk is 7.13%.

2. Active returns are uncorrelated.

3. Overall equity portfolio benchmark is Dumax 3000.

4. Caroline Wesula has taken information in the table above and used mean-variance optimizer to create an implementation efficient frontier. The highest risk point on the efficient frontier is 100% allocation to the long-short manager with a 100% Dumax 1000 overlay.

5. The active risk of this portfolio with the adjustments in point (4) above is 6.1%.

Required:

Justify why the active risk is greater than 6%. (2 marks)

Calculate the total active risk for Active N. (2 marks)

Caroline Wesula’s current equity manager allocation is 30% Dumax Index and 70% semi-active:

Calculate total current expected active return, active risk and information ratio. (4 marks)

(Total: 20 marks)

QUESTION FIVE

1. Describe TWO approaches used in constructing an index portfolio. (4 marks)

2. Explain THREE components of returns for commodity futures contracts. (6 marks)

3. A portfolio manager has a portfolio worth Sh.100 million, Sh.30 million of which is his own funds and Sh.70 million is borrowed. If the return on the invested funds is 6% and the cost of borrowed funds is 5%.

Required:

Calculate the return on the portfolio. (4 marks)

4. Brian Maritim is the portfolio manager of Rich Corporate Bond investors. His current Sh.100 million bond position

is as follows:

The investment policy statement (IPS) allows the portfolio manager to leverage the portfolio by 20%.

Required:

The effective duration of the bond portfolio. (2 marks)

The contribution of bond B to the effective duration of portfolio. (1 mark)

Identify THREE types of risks that Brian’s bond portfolio is potentially exposed to. (3 marks)

(Total: 20 marks)