OVERVIEW OF WORKING CAPITAL MANAGEMENT

Definition of Working Capital

Working Capital (Net Current Assets) = Excess of Current Assets over Current Liabilities.

Current Assets: Stock (Finished Goods, WIP and Raw Materials), Debtors, Marketable Securities and Cash/Bank.

Current Liabilities: Creditors Due Within One Year, Trade Creditors, Prepayments received, Tax Payable, Dividends Payable, Short-term Loans and Long-term Loans Maturing Within the Year.

It may be regarded loosely as: STOCKS + DEBTORS – CREDITORS.

Working Capital Management is basically a trade off between ensuring that the business remains liquid while avoiding excessive conservatism, whereby the levels of Working Capital held are too high with an ensuing large opportunity loss. Obviously, the levels of Working Capital required depend to a large extent on the type of industry within which the company is operating ; contrast service industries with manufacturing industries.

Matching Concept

Long-term assets must be financed by long-term funds (debt/equity). Short-term assets can be financed with short-term funds (e.g. overdraft, creditors) but it may be prudent to finance partly with long-term funds. Working capital policies can be identified as conservative, aggressive or moderate:

- Conservative – financing working capital needs predominantly from long-term sources of finance. Current assets are analysed into permanent and fluctuating – long-term finance used for permanent element and some of the fluctuating current assets. This will increase the amount of lower risk finance, at the expense of increased interest payments and lower profitability.

- Aggressive – short-term finance used for all fluctuating and most of the permanent current assets. This will decrease interest costs and increase profitability but at the expense of an increase in the amount of higher-risk finance used.

- Moderate (or matching approach) – short-term finance used for fluctuating current assets and long-term finance used for permanent current assets.

Short-term finance is more flexible than long-term finance and usually cheaper. However, the trade-off between the relative cheapness of short-term debt and its risks must be considered. For example, it may need to be continually renegotiated as various facilities expire and due to changed circumstances (e.g. a credit squeeze) the facility may not be renewed. Also, the company will be exposed to fluctuations in short-term interest rates (variable).

Overtrading/Undercapitalisation

This occurs where a company is attempting to expand rapidly but doesn‟t have sufficient long-term capital to finance the expansion. Through overtrading, a potentially profitable business can quite easily go bankrupt because of insufficient cash.

Output increases are often obtained by more intensive use of existing fixed assets and growth is financed by more intensive use of working capital. Overtrading can lead to liquidity problems that can cause serious difficulties if they are not dealt with promptly.

Overtrading companies are often unable or unwilling to raise long-term capital and rely more heavily on short-term sources (e.g. creditors/overdraft). Debtors usually increase sharply as credit is relaxed to win sales, while stocks increase as the company attempts to raise production at a faster rate ahead of increases in demand.

Symptoms of Overtrading

- Turnover increases rapidly

- The volume of current assets increases faster than sales (fixed assets may also increase)

- Increase in stock days and debtor days

- The increase in assets is financed by increases in short-term funds such as creditors and bank overdrafts

- The current and quick ratios decline dramatically and Current Assets will be far lower than Current Liabilities

- The cash flow position is heading in a disastrous direction.

Causes of Overtrading

- Turnover is increased too rapidly without an adequate capital base (management may be overly ambitious)

- The long-term sources of finance are reduced

- A period of high inflation may lead to an erosion of the capital base in real terms and management may be unaware of this erosion

- Management may be completely unaware of the absolute importance of cash flow planning and so may get carried away with profitability to the detriment of this aspect of their financial planning.

Possible means of alleviating overtrading are:

- Postponing expansion plans

- New injections of long-term finance either in terms of debt/equity or some combination

- Better stock/debtor control

- Maintaining/increasing proportion of long-term finance Undertrading/Overcapitalisation

Here the organisation operates at a lower level than that for which it is structured. As a result capital is inadequately rewarded. This can normally be identified by poor accounting ratios (e.g. liquidity ratios too high or stock turnover periods too long).

Assessment of Liquidity Position

The liquidity position of an organisation may be assessed using some key financial ratios:

Current Assets

| Current Ratio | = | Current Liabilities |

| Quick Ratio or (“Acid Test”) | = | Current Assets – Stock

Current Liabilities |

| Debtors Collection Period | = | Debtors x 365 days

Sales |

| Creditors Payment Period | = | Creditors x 365 days

Purchases |

| Stock Period | = | Stock x 365 days

Cost of Sales |

| Alternatively: | ||

| Stock Turnover Period | = | Cost of Sales

= Y times |

Stock

Benchmarks often quoted are a Current Ratio of 2 : 1 and a Quick Ratio of 1 : 1 but these should not be adopted rigidly as organisations have vastly different circumstances (operating in different industries, seasonal trade etc.).

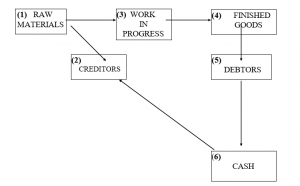

Working Capital Cycle

Often referred to as the “Operating Cycle” or the “Cash Cycle” this indicates the total length of time between investing cash in raw materials and its recovery at the end of the cycle when it is collected from debtors. This can be shown diagrammatically:

The Working Capital Cycle can also be expressed as a period of time, by computing various ratios:

| Stock | Avg. Stock

Cost of Sales |

x 365 | = | Y days |

| Debtors | Avg. Debtors

Sales |

x 365 | = | D days |

| Less: Creditors | Avg. Creditors

Purchases |

x 365 | = | (C days) |

| Working Capital Cycle (days) | W days

|

It is difficult to determine the optimum cycle. Attention will probably be focussed more on individual components than on the total length of the cycle. Comparison with previous periods or other organisations in the same industry may reveal areas for improvement.

The factors determining the level of investment in current assets will vary from company to company but will, generally, include:

- Working Capital Cycle – companies with longer working capital cycles will require higher levels of investment in current assets.

- Terms of Trade – period of credit offered; whether discounts permitted.

- Credit Policy – company‟s attitude to risk (“conservative” v “aggressive”).

- Industry – some industries have long operating cycles (e.g. engineering), whereas others have short cycles (supermarket chain)

CASH MANAGEMENT

Cash is an idle asset and the company should try to hold the minimum sufficient for its needs.

Three motives are suggested for holding liquid funds (cash, bank deposits, short-term investments):

- Transaction Motive – to meet payments in the ordinary course of business – pay employees, suppliers etc. Depends upon the type of business, seasonality of trade etc.

- Precautionary Motive – to provide for unforeseen events e.g. fire at premises. Depends upon management‟s attitude to risk and availability of credit at short notice.

- Speculative Motive – to keep funds available to take advantage of any unexpected

“bargain” purchases which may arise – e.g. acquisitions, bulk-buying etc.

Cash Budget

A very important aid in cash management: most organisations, whether small or large multinationals, will prepare a Cash Budget at least once a year. It is usually prepared on a monthly/quarterly basis to predict cash surpluses/shortages.

The opening cash surplus of RWF50,000 turns into a negative figure from end of January onwards, mainly due to capital expenditure, and peaks at (RWF96,000) in March. Thus, the company will have to arrange an overdraft in advance to cover the shortfalls. Alternatively, the company could take action to avoid the potential negative results. Some possibilities are:

- Deferring replacement of fleet of cars.

- Deferring purchase of machine – impact on production and sales must be considered.

- Considering leasing cars/machine.

- Negotiating more generous credit period from supplier.

- Encouraging earlier payment by customers, possibly by offering a discount.

- Chasing bad debts and reducing below 10%.

- Liquidating investments – consider yield etc.

- Selling any non-essential assets

- Rescheduling loan repayments

- Reducing dividend payments

- Deferring Corporation Tax (penalties!)

Bank Overdraft

This is one of the most important sources of short-term finance. It is a very useful tool in cash management, particularly for companies involved in seasonal trades.

The main advantages are:

- Cost may be lower than other sources (generally, short-term finance is cheaper than long-term).

- Less security required than for term loans – overdraft can be recalled at short notice.

- Repayment is easier as there are no structured repayments – funds are simply paid into the account as they become available.

- Interest is only charged on the amount outstanding on a particular day.

- Extra flexibility is provided as all of the facility may not be used at any one time. The unused balance represents additional credit which can be obtained quickly and without formality.

The main disadvantages are:

- Renewal is not guaranteed.

- Technically, the advance is repayable on demand – could lead to a strain on the company‟s cash flow. Variable rate of interest – the facility may be renewed on less favourable terms.

Term Loan

Finance is made available for a fixed term and usually, at a fixed rate of interest. Repayments are in equal instalments over the term of the loan. Early repayment may result in penalties.

The main advantages are:

- The term can be arranged to suit the borrower‟s needs.

- The repayment profile may be negotiable to suit the expected cash flow profile of the company (e.g. interest only basis to keep ongoing repayments lower).

- Known cash flows assist financial planning.

- The interest rate is fixed, so the company is not exposed to increases in rates.

Cash Lodgement

It is important that cash is lodged as quickly as possible so that the organisation gets the benefit through an increase in investments or a reduction in overdraft. However, apart from the security risk of cash lying idle there are costs of making lodgements (bank, clerical, transportation etc.) It becomes a “Balancing Act” to minimise costs and maximise benefits (interest).

Centralised Cash Management

If an organisation has decentralised operations e.g. multiple branches, there may be advantages in centralising cash management at Head Office. These are:

- Economies of Scale – by avoiding duplication of skills among divisions.

- Expertise – specialist staff employed at Head Office.

- Higher Yield – increased funds available may provide a greater return and reduce transaction charges. Likewise, borrowings can be arranged in bulk at keener interest rates than for smaller amounts.

- Planning – a cash surplus in one division may be used to offset a deficit in another, without recourse to short-term borrowings.

- Bank Charges – should be lower as the carrying of both balances and overdrafts should be eliminated.

- Foreign Currency Risk – can be managed more effectively as the organisation‟s total exposure situation can be gauged.

Some disadvantages are:

- Slower decision making

- Loss of local market knowledge

- Demotivation of local staff

Computerised Cash Management

This allows companies via a computer terminal to get up-to-date information on cleared balances on their bank accounts. Three basic services are provided:

Account Balances – information provided on all accounts within a group (domestic and foreign). Details of un-cleared items which will clear the next day, forecast balances and individual transactions are available.

Decision Support – current money market and foreign exchange rates provided.

Funds Transfer – some services offer a direct link to brokers/banks, permitting instant deals to be made.

The service facilitates more efficient cash management as available cash balances are identified and utilised to the maximum. Thus, overall cash flow planning is more accurate. To obtain the full benefit cash management should be centralised. However, potential benefits must be compared with the additional costs incurred.

Cash Management Models

A number of cash management models have been developed to determine the optimum amount of cash that a company should hold. One approach is to use the Economic Order Quantity (EOQ) Model, which is used in stock management (see Stock Management section later). Another (and more sophisticated) approach is the Miller-Orr Model. This determines a lower limit, an upper limit and a normal level on cash balances. If cash reaches the lower limit the firm sells securities to bring the balance back to the normal level. On the other hand, if the cash balance reaches the upper limit the firm should buy sufficient securities to return to the normal level. The various limits are set by reference to the variance of cash flows, transaction costs and interest rates.

Investment of Short-Term Funds

In deciding the best approach consideration must be given to the quantity of funds; length of time for which available; certainty of the funds; rate of return; risk and variability of return; possibility and costs of early termination (liquidity).

Possible investments are:

- Short-Term Deposits – return depends on the period and amount.

- Certificates of Deposit (CD’s) – flexible as CD‟s are negotiable.

- Treasury Bills – known, fixed return if held to maturity. Early disposal may result in capital gain/loss.

- Reduction in Overdraft

C. THE MANAGEMENT OF DEBTORS

Excessive debt balances are a wasted resource which should be avoided by careful management. Good Management means reducing it to the practical minimum, consistent with not damaging the business. For example, it is no good simply refusing to give customers credit – they will go elsewhere. A balanced approach is required which will reduce debtors to a minimum acceptable level.

Debtors are often one of the largest items in a company‟s Balance Sheet and also one of the most unreliable assets, largely because company policies concerning them are often inadequate or poorly defined and in the hands of untrained staff. Typically, a company could have 20% – 25% of total assets as debtors.

Credit management is a problem of balancing profitability and liquidity. Extended Credit terms can be a sales attraction but higher debtors put a strain on liquidity. Management of debtors will be concerned with achieving the optimum level of investment. This requires finding the correct balance between:

- Extending credit to increase sales and, therefore profits and

- The cost of investment in debtors (cost of finance, administration, bad debts etc.)

By setting the “terms of sale” the company can, to some extent, control the level of debtors. However, the relative strengths of the credit-giver and the credit-taker are important. Consideration must also be given to the industry norm.

The company has at least four factors to control debtors:

- The customers to which it is prepared to sell.

- The terms of credit

- Whether cash discounts will be offered? 4. The follow-up procedures for slow payment.

Evaluating Credit Risk

Before extending credit to new customers management will assess the risk of default in payment/non-payment. This will be based upon experience and judgement but in addition, the following sources may be used:

- Trade References – from other suppliers (at least two).

- Bank References – may be of limited use as banks are reluctant to supply adverse references.

- Credit Agency Reports – specialist agencies (e.g. Dun & Bradstreet) will provide detailed reports on the history, creditworthiness, business etc. of individuals and organisations on payment of a fee.

- Published Information – annual accounts etc.

- Own Salesmen – useful source but views may not be objective (commission receivable?).

- Newspapers and Trade Journals.

- Other Credit Controllers – many trade associations where controllers meet regularly to exchange information about the state of the industry generally and slow/bad payers in particular.

- Own Information – check old customer files to see if you have ever done business in the past.

- Trial Period – on a “cash -only” basis.

- Credit Limit – fix at low level initially and only increase if payment record warrants.

- Site Visits – an opinion on the operations can be formed by visiting the premises.

- Credit Scoring – evaluate potential customer using credit scoring or other quantitative techniques. Credit scores are risk indicators – the higher the score, the lower the risk. Scores will be allocated based on the characteristics of the new customer (e.g. age, occupation, length of service, married/single, home owner, size of family, income, commitments etc.). Credit scoring is particularly suited to financial institutions and the amount of credit offered, if any, will depend on whether the credit score is above a predetermined cut-off level. Computerised systems (“expert systems”) are especially useful for this purpose.

Although terms and settlement discounts are often influenced by custom and practice within an industry it is still possible to change them. Once defined, ensure that the customers are aware of them – ideally, they should be informed when they order, when they are invoiced and when they receive statements. Always try to enforce the specified discount policy.

Discounts

As extended credit facilities may be expensive to finance the firm may offer customers a discount (cash/settlement discount) to encourage them to pay early. As with extended credit discounts may also be used as a marketing tool in an effort to increase sales. To evaluate whether it is financially worthwhile the cost of the discount should be compared with the benefit of the reduced investment in debtors.

In industries that deal with both trade and retail customers (e.g. building supplies) it is usual to offer trade discounts. This may reflect the economies of scale which derive from larger orders and the greater bargaining power of the customer. Trade discounts are frequently much larger than cash/settlement discounts and may be for as much as 25% of the quoted price.

Debt Control

Good debt control can be summed up as ensuring that all sales are paid for within an agreed period, without alienating customers, at the minimum cost to the company.

The company itself can take steps to “assist” the debtors to pay promptly:

- Issue invoices and statements promptly.

- Deal with customer queries/disputes immediately.

- Issue credit notes as agreed

- Be flexible in billing arrangements to accommodate customers.

There is no one debt collection policy that is applicable to all companies. Policies will differ according to the nature of the product and the degree of competition. Debt control system will probably include:

- Well trained credit personnel.

- Measures to ensure that credit limits are not exceeded.

- Formal set procedures for collecting overdue debts, which should be known by all staff and applied according to an agreed time schedule. Care must be taken that the cost of the debt collection does not exceed the amount of the debt, except where used as a deterrent. Also over-zealous collection techniques may damage goodwill and lose future sales.

- Computerised monitoring systems to identify overdue accounts as early as possible. For example, ratios, compared with the previous period to highlight trends in credit levels and the incidence of overdue and bad debts; statistical data to identify causes of default and the incidence of bad debts among different classes of customer and types of trade. An “Aged Analysis of Debtors” is particularly useful in this regard.

Among the many debt collection techniques that can be used are:

- Invoices – issued promptly following delivery of goods/service.

- Statements – at monthly/other intervals to draw attention to unpaid debts.

- Overdue Letters – carefully drafted to provoke an immediate response; individual rather than computer-produced; series of letters of varying degrees of severity.

- Telephone Calls – these ensure that customer has received the letter(s) and gives him an opportunity to raise any queries or advise of any difficulties which may cause a change of approach to help him out.

- Mail or Email Reminders.

- Visits by Sales Staff.

- Visits by Credit Control Staff.

- Use of External Agencies – debt collection agency; factoring company etc.

- Threaten Withdrawal of Credit Facilities/Discounts.

- Threaten To Withhold Future Supplies.

- Lawyer‟s Letter.

- Legal Action – beware cost of action does not exceed debt.

In most cases some extra spending on debt collection will reduce the overall cost of the investment in debtors (e.g. reduction in bad debts/average collection period etc.). However, beyond a certain level extra spending is not usually cost effective.

Factoring

This involves the sale of trade debts for immediate cash to a “factor” who charges commission. Factoring companies are financial institutions often linked with banks. Unlike an overdraft the level of funding is dependent, not upon the fixed assets of the company, but on its success, for as the company grows and sales increase the facility offered by the factor grows, secured against the outstanding invoices due to the company. Three basic services are offered, although a company need not use all of them:

- Finance – instruction on invoices that payment is to be made to the factor, who is responsible for collection of the debt. When the factor receives the invoices 80% approx. of value is advanced. The balance (less charges, including interest) is paid, either when the invoice is settled or after a specified period.

- Sales Ledger Management – the factor takes the place of the client‟s accounts department. Duplicate invoices are sent to the factor who maintains a full sales ledger for each client, handles invoices, chases outstanding payments etc. Commission of 1% – 2% is usually charged.

- Credit Insurance – in return for a commission the factor provides a guarantee against bad debts.

Recourse Factoring – the factor will reclaim the money advanced on any uncollected debt so the business will retain the risk of non-recovery and, depending on the contract terms, perhaps the administration burden as well.

Non-Recourse (Full) Factoring – the factor runs credit checks on the company‟s customers and agrees limits dependent on their creditworthiness. These can be adjusted in the light of experience, once a pattern has been established. The factor will protect the client against bad debts on approved sales and will also take on all the administration burden. The balance over the 80% advance is paid to the client an agreed number of days after the initial advance.

Recourse v Non-Recourse Factoring – with non-recourse factoring the business knows that it will get paid, no matter what happens but protection only applies to credit-approved debts and it is not always easy to get this approval for doubtful ones. Recourse factoring allows more funding to be made available against less credit-worthy debtors and the business is in control of when and how individual debts are to be pursued and collected.

The cost of finance through factoring is usually slightly above overdraft rates. The administration charges vary between 0.6% and 2.5% approx.

Advantages of Factoring

- It is an alternative source of finance if other sources are fully utilised, particularly for a company with a high level of debtors.

- It is especially useful for growth companies where debtors are rising rapidly and funds available from the factor will rise in tandem.

- Security for the finance is the company‟s debtors, leaving other assets free for alternative forms of debt finance.

- The factor may be able to manage the company‟s sales ledger more efficiently by employing specialist staff, leading to lower costs for the company and freeing management to concentrate on growing the business.

- Bad debts will be reduced or guaranteed by credit insurance.

- Due to the greater guarantee of cash flow the company will have a better opportunity for taking up cash discounts from suppliers.

- The factor will be more efficient in collecting monies. Evidence in Europe suggests that, on average, it takes over 75 days for an invoice to be paid, whereas the average debt turn of companies using factoring is 60 days.

- The company replaces a great many debtors with one – the factor – who is a prompt payer.

Disadvantages of Factoring

- It may be more expensive than other sources.

- When fixing credit terms and limits the factor will be concerned with minimising risk and, therefore, certain risky but potentially profitable business may be rejected.

- The factor may be “pushy” when collecting debts. This may lead to ill-feeling by customers.

- Use of a factor might reflect adversely on a company‟s financial stability in the eyes of some ill-informed people. Factoring is more acceptable nowadays but this problem could be overcome by undisclosed factoring, which leaves the company to collect payment as agent for the factor.

Invoice Discounting

This is similar to factoring but only the finance service is used. Invoices are discounted (like Bills Receivable) and immediate payment, less a charge, is received. The company still collects the debt as agent for the financial institution and is also liable for bad debts. The service tends to be used on an ad hoc basis and is provided by factors for clients who need finance but not the administrative service or protection. Invoice Discounting is confidential and solely a matter between the lender and borrower, unlike Factoring where the bank assumes a direct and visible role between the company and its debtors. Also, the company retains full control over the management of its debtor‟s ledger, including credit control.

THE MANAGEMENT OF CREDITORS

Trade credit is often used as a source of finance. The costs of this source of finance are the costs of any discounts forgone and any interest charges which the creditor charges on overdue bills. Of course, excessive use of this source may lead to poor relations with a supplier (or even no relations) which can be damaging.

Credit from suppliers is a very important source of short-term finance.

The credit is mistakenly believed to be cost-free. The costs include the following:

- Loss of Supplier‟s Goodwill – this is difficult to quantify. If the credit period is regularly overdone suppliers may put a low priority on the quality of service given; further orders may be refused; cash on delivery or payment in advance demanded.

- Higher Unit Costs – the supplier may try to recoup the cost of longer credit by charging increased prices.

- Loss of Cash Discounts – if the credit period is used then discounts are not being taken. Thus, the cost of credit is the cost of not taking the discount.

Example

Your company normally pays within 45 days. The supplier offers a 2% discount for payment within 10 days. If the company refuses the discount the implied cost of not taking the discount is:

2 365

—– x —– = 21.3% p.a.

98 35

The cost of not taking the discount (opportunity cost) is 21.3% p.a.

Despite the above costs trade credit is the largest source of short-term funds for companies. Among the advantages are:

- Obtaining credit is informal.

- It is a flexible source of finance – but payment should not be delayed regularly.

- It is a relatively stable source of finance – it is available continuously.

- No security is required – unlike other forms of credit.

THE MANAGEMENT OF STOCKS

In many organisations stock requires the commitment of a large amount of resources. The classic conflict often arises:

The Production manager desires a large stock of raw materials so that production is uninterrupted.

The Sales manager desires a large stock of finished goods so that no sales are lost.

The Finance manager desires a low level of all types of stock so that costs are minimised.

Ordering and Holding Costs

High levels of stock can only be achieved at a cost. The total cost of stock-holding has many elements:

- Cost of financing

- Storage (warehousing)

- Handling

- Insurance

- Administration

- Obsolescence

- Deterioration

- Pilferage

Sound stock control entails having the right product available in the right quantity, at the right time and at the right cost.

Fast and frequent replenishment of sales will minimise stock-holding.

Overall, reducing stock is likely to increase profitability rather than decrease it. Reducing stock is almost totally within the control of management – unlike reducing debtors or increasing creditors, it does not rely on the co-operation of third parties.

Economic Order Quantity (EOQ)

Total stock-holding costs could be broadly classified as “Holding” costs and “Ordering” costs. The EOQ model attempts to minimise total costs by balancing between holding and ordering costs. If large batches are ordered this will result in high holding costs and low ordering costs. Conversely, if small batches are ordered this will result in low holding costs and high ordering costs.

EOQ

h

where: c = cost per order d = annual demand for item of stock

h = annual cost of holding a unit in stock

The EOQ Model makes a number of assumptions:

- Order cost is constant regardless of the size of the order.

- Use of the item of stock is constant.

- No stock-outs occur. Purchase price is constant.

Discounts

If the supplier offers a discount for larger orders this may alter the position. The discount will offer two savings – a reduced purchase price and lower ordering costs because fewer orders are placed. Using the above example, suppose that a discount of 2% is offered on orders of 400 or more.

THE DISCOUNT IS WORTHWHILE

Just In Time Stock Management (JIT)

The main purpose of JIT purchasing is to ensure that delivery of supplies occurs immediately prior to the requirement to use them in manufacture, assembly or resale. Close co-operation between user and supplier is essential. The supplier is required to guarantee product quality and reliability of delivery while the user offers the assurance of firmer long-term sales. Users will purchase from fewer and perhaps, only a single supplier, thus enabling the latter to achieve greater scale economies and efficiency in production planning. The user expects to achieve savings in materials handling, inventory investment and store-keeping costs since (ideally) supplies will now move directly from unloading bay to the production line. There may also be benefits from bulk purchasing discounts or lower purchase costs.

With a JIT system there is little room for manoeuvre in the event of unforeseen delays – e.g. on delivery times. The buyer is also dependent on the supplier for the quality of materials, as expensive downtime or a production standstill may arise, although guarantees and penalties may be included in the contract as protection.