It helps in understanding the concept of cost. The following are necessary:

Opportunity Cost Assuming full resources allocation and employment in production of good and services increasing the production of any one product involves the sacrifice of an alternation product. The cost of producing a certain product is taken to refer to the forgone value of the alternative product

Private cost and social cost (negative externalities) private cost refers to these costs which relates to an individual producer. They include both explicit and implicit. While social cost refer to these costs which occur to the third party in the production

process.

Implicitly cost The explicit costs refer to the money paid out made by the firm. This includes payment for resources bought or hired e.g. wages, cost of raw materials, rent etc.

Implicit cost includes the resources owned and used by the firm‟s the owner. When the profits are calculated on the bases of explicit and implicit cost we obtain economic profit. When calculated only on basis of explicit cost we obtain financial profit.

Assumptions

- The firms take prices or input as determined by the market forces.

- Firms aim at minimizing the production cost.

Short Run Cost Function

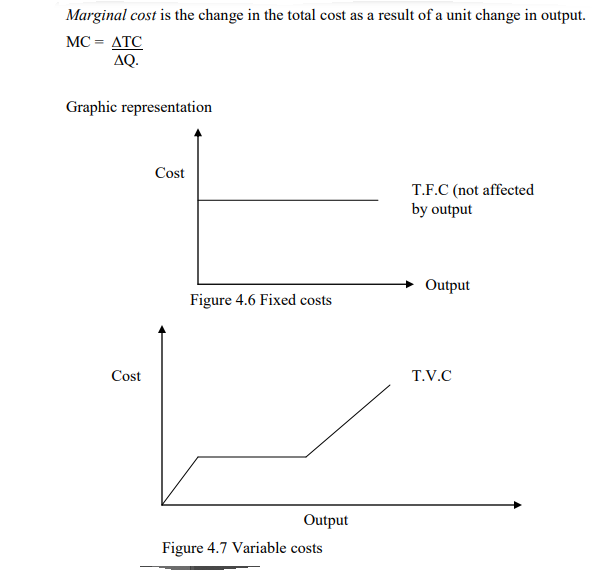

In the short run input levels will depend on output level that the firm wants to achieve. In short run not all factors will be varied. At least one must be fixed and therefore the cost incurred on it will be fixed cost. The total fixed cost will be constant regardless of the

output level e.g. rent for factory building, salaries of office staff etc.

Variable costs are incurred by the firm for its variable input. A firm wishing to increase its out put will require large variable input thus higher variable cost. The variable costs of a firm will increase as the output levels increase e.g. cost of raw materials, cost of direct labour and other direct running expenses.

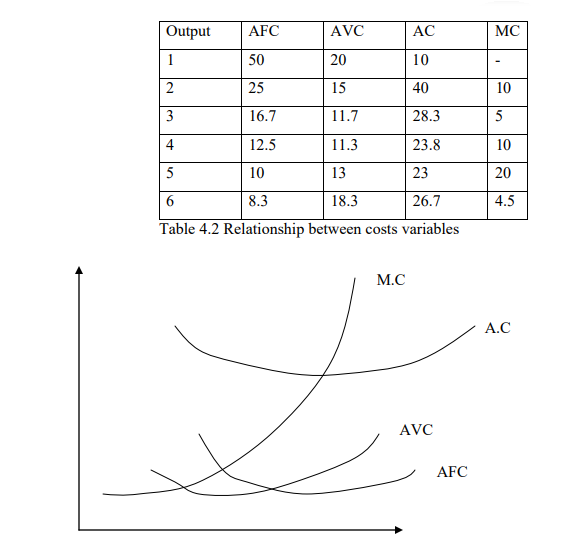

The relationship between average cost and marginal cost In most of case the marginal cost the average cost from below. The average cost must be failing as compared to marginal cost a) Mathematically it can be shown that, if the slope of average cost is less than zero, then the marginal cost will be less than average cost AC<0; MC0 ;MC>AC Since the average cost curve is U- shaped the slope of average cost becomes zero to its minimum and hence marginal cost is equal to costs at this point. T.F.C (not affected by output output) Output Cost Cost T.V.C Output The relationship between average total costs, average fixed cost, average variable cost and marginal cost is shown in Table 4.2.