5.1 Introduction

One of the most important aspects of inventory control is to have the items in stock at the moment they are needed. This includes going into the market to buy the goods early enough to ensure delivery at the proper time. Thus, buying requires advance planning to determine inventory needs for each time period and then making the commitments without procrastination. For retailers, planning ahead is very crucial. Since they offer new items for sale months before the actual calendar date for the beginning of the new season, it is imperative that buying plans be formulated early enough to allow for intelligent buying without any last minute panic purchases. The main reason for this early offering for sale of new items is that the retailer regards the calendar date for the beginning of the new season as the merchandise date for the end of the old season.

For example, many retailers view March 21 as the end of the spring season, June 21 as the end of summer and December 21 as the end of winter. Part of your purchasing plan must include accounting for the depletion of the inventory. Before a decision can be made as to the level of inventory to order, you must determine how long the inventory you have in stock will last. For instance, a retail firm must formulate a plan to ensure the sale of the greatest number of units. Likewise, a manufacturing business must formulate a plan to

ensure enough inventory is on hand for production of a finished product.

In summary, the purchasing plan details:

- When commitments should be placed; ! When the first delivery should be received;

- When the inventory should be peaked;

- When reorders should no longer be placed; and

- When the item should no longer be in stock.

Well planned purchases affect the price, delivery and availability of products for sale.

5.2 What is a Procurement Plan?

A Procurement Plan defines the products and services that you will obtain from external suppliers. A good Procurement Plan will go one step further by describing the process you will go through to appoint those suppliers contractually. Whether you are embarking on a project procurement or organizational procurement planning exercise, the steps will be the same. First, define the items

you need to procure. Next, define the process for acquiring those items. And finally, schedule the timeframes for delivery. Procurement Plan helps the organization to procure products and services from external suppliers. It provides firms with a complete project procurement plan template, to help them to quickly and easily create a Procurement Plan for the business.

By planning procurement carefully, the firm can buy the right products for itself at the right price.

5.3 Importance of procurement plan

The Procurement Plan helps to:

- Define your procurement requirements

- Identify all of the items you need to procure

- Create a sound financial justification for procuring them

- List all of the tasks involved in procuring your products

- Schedule those tasks by allocating timeframes and resources

- Create a robust project procurement process for your business

Procurement Planning is critical if you want to get the most out of your supplier relationships. By using this Procurement Plan template, you can quickly and easily define your procurement requirements, the method of procurement and the timeframes for delivery.

5.4 Strategic purchasing plan

Manufacturers that plan, manage, and control their materials management and purchasing functions can significantly improve cash flow, profits, and customer satisfaction. A strategic purchasing plan can achieve these results. Establishing an effective strategic purchasing plan requires a manufacturer to undertake a five-step process of developing goals for improvement and monitoring its progress

1. Business Performance Measurement

The first step in developing a strategic purchasing plan is to establish and evaluate the company’s materials management performance measurements and identify areas of potential improvement; for example, inventory turns and payable days as they relate to measurements of cash flow. For every purchased product or service there is an opportunity for improvement in areas such as

price, quality, service, delivery, consignment, and supplier-value added. Profit improvement goals should be established to reflect what is possible and not what is easily attained. Most organizations can expect to achieve a 20 to 60 percent improvement for each performance measurement, depending on the particular goal, the creativity utilized, and the company’s commitment. It is

important that current performance levels and goals for improvement are communicated to employees. In addition, suppliers should be advised of goals that affect them. A good way to communicate these goals is to design a business performance measurement matrix

2. Organizational Strengths

Once the manufacturer has identified the areas it wants to improve, it must assess its organizational strengths to determine which assets will be needed to achieve those goals. Assets useful in strategic purchasing include material requirements planning software (MRP), business forecasting/budgeting methods, floor plans that promote timely communications, business teams, and cycle time compression. One of the most important strengths a company has is its personnel. Every organization has employees who not only understand the need for improvement but can also convert goals into reality. Employees that can accept responsibility for project leadership and completion should be recruited to serve on cross-functional business teams that will pave the way for the rest of the

company.

To get all employees involved in the improvement process, a manufacturer should implement a closed-loop management system that provides feedback to employees, encourages the setting of goals, and emphasizes the measurement of progress as it is made. This system can organize, train, and mobilize all employees with a focus on improvement. Above all, the crucial element for success in any strategic purchasing plan is management’s commitment to the process. A philosophical commitment is not enough-management must be ready to fully participate in the strategic purchasing plan. All employees will be asked to change the way they view the business and to develop a discipline of continuous improvement, and unless management actively participates and demonstrates its commitment, that change will not occur.

3. Supplier Integration

Suppliers are the single greatest underutilized business resource. Most manufacturers fail to see suppliers as an extension of their organization and don’t share information with them. A company’s suppliers share in its success and can be willing and valuable participants in the strategic purchasing plan. Suppliers are experts in their particular businesses and have knowledge and expertise that can be valuable to the company seeking improvement. The manufacturer should inform current suppliers of the company’s strategic purchasing plan, including the magnitude of improvement that is expected, and seek their input. It’s also a good idea to contact suppliers that might want to increase their level of business with the company and give them the opportunity to participate.

Suppliers can contribute to a manufacturer’s success in several ways:

• Assist in the forecasting of high dollar and long lead time purchases.

Results:

• supplier may commit to stocking materials

• improved on-time delivery

• reduced setup charges

• reduced transportation costs (e.g., emergency delivery)

• Identify areas of excessive specifications and other areas of high costs and provide input on lead time reduction.

• Aid in new product introduction.

• More accurate introduction lead times, estimated costs, and design/costs/specification relationships

• Reduced time-to-market cycle

4. Strategy for Improvement

After investing considerable time and effort into identifying goals and assessing its organizational strengths, a manufacturer must devise an implementation strategy that will foster the success of the strategic purchasing plan so that its efforts will not be wasted. A good method of ensuring success is to begin the improvement process with the “low hanging fruit”-that is, choose a goal that is sure to

be attained as the first step in the plan. When that goal is attained, it will gain momentum for the plan and inspire confidence among employees. It will also discredit any “doubting Thomases.”

5. Measure the Results

To ensure success, a method of measuring progress toward goals must be established. Measurement is important because it creates discipline and a routine of improvement. It identifies those teams and employees who may require help and provides an opportunity to recognize and reward achievement. To support the momentum and enthusiasm necessary for success, incremental progress should be conveyed to employees. A successful strategic purchasing plan is the result of a business that understands the magnitude of

change required, has the conviction to commit to the change process, and utilizes the tools and concepts of organized and controlled change management. As a result, the manufacturer will become financially stronger and more responsive to the marketplace, resulting in a larger market share.

5.5 MATERIALS PLANNING

Production planning is an area for top management decisions through which production plans, programmes and targets are spelled out. Production planning process starts well before the completion date so that sufficiently long time is given to the management to enable it to consider “alternative courses of action and authorize major commitments for materials, manpower, and plant facilities.”

Materials planning are a part of production planning. In fact for an effective inventory control, production plans should be converted into materials plans. This enables the management in clearly defining the quantity and schedule of the equipments. In the integrated materials arrangement, production and materials planning get a pride of place. Inventories consume a larger part of working capital. For best possible utilization of available capital resources, a material, planning is resorted to. It enables the management to anticipate the future materials demands. Such anticipation helps in managing the materials in a manner in which it enables the organization to

accomplish the given objectives. Infact, materials planning provides a mechanism for inventory control.

Materials planning defined

“Materials planning” is the scientific way of determining the requirements of raw materials, components, spares and other items that go into meeting production needs within the economic investment policies.” As the definition goes, materials planning are a function and are a system which evolves methodology to plan the requirements of materials in a scientific manner. It is positively related with production which follows market conditions and sales forecasts. Further it cannot ignore the economy and the investment policy of the organization. These two factors also go side by side.

Factors affecting Material Planning

The following are the two factors which affect materials planning substantially:

1. The external Factors, and

2. The Internal Factors.

In economic terminology, external factors may be termed as macro factors which may be enumerated as under:

1. National Economy

2. Price Trends.

3. Monetary and Fiscal Policy of the Government:

- Credit Regulations,

- Direct and Indirect Taxes,

- foreign Exchange regulations,

- Import Policy, and

- International Market, etc.

4. Business Cycles, and

5. Other factors which usually fall under factors not within the reach of the organization, that is, uncontrollable factors.

The internal factors, affecting materials planning may be termed as micro factors or incorporate factors, are as listed below.

1. Corporate objectives and plans;

2. Technology available;

3. Market demand

4. Lead time and rejection rates

5. Working capital available

6. Nature of the inventory required and help;

7. Plant capacity and its utilization

8. Inventory levels;

9. Seasonal variations and market supply position;

10. Information and data available;

11. Delegation of power;

12. Communication system

13. Warehousing facilities available; and

14. Overall materials policy

5.6 Purchasing and Materials planning

Main job of purchasing personnel is to get materials when needed and pay for them as little as possible considering quality, quantity and other requirements and prices trends. It is the efficiency of the purchasing personnel which makes the real difference on the profit by the industrial unit as well as a commercial unit. Specific technical knowledge cost analysis; value analysis and good judgment go a long way in making a purchasing efficient.

But conservative thinking that purchasing function is an order – placing activity still holds good. The modern thinking is yet to penetrate and wipe off the outside manufacture and hence we have to view it from materials planning point of view. This takes for granted a closer tie between purchasing and other functions. A close liacon between other departments of the organization on

the one hand materials department is a prerequisite for an effective materials planning. For smooth and an interrupted operation of the organization, it is necessary that every – one in the organization should be actively involved in the attainment of the objectives of the organization. It is this involvement which is important for any effective material planning since all the departments of the organization are somehow or other related to what is required and procured for the efficient running of the whole organization.

Here, we are faced with an awesome question: “in view of the wide diversity of responsibility( of the purchasing personnel)…., is it possible to formulate any unified procedure o the basis of which we may determine what is considered to be the escape of the purchasing for materials planning?”

Certainly it is possible. What is required is that we should follow well recognized principles of sound purchasing procedures, which are listed below.

1. The ascertainment of the need,

2. an accurate statement of the character and the quantity of goods desired,

3. The transmission of requisition,

4. Negotiation for possible sources of supply,

5. Analysis of the proposed purchase, selection of Vendors and placing of the supply order,

6. the follow up of the order,

7. The checking got the invoice,

8. The receipt and inspection of goods delivered, and

9. Completion of the records.

For any effective materials planning, it is necessary that purchasing functions should be well – organized and the department should follow well – recognized principles. Materials planning should be such which may enable the materials manager to cope with the demand for materials and as when it comes to him. Materials are basic to profitability. Raw materials, purchased materials

and other supplies are cost centre of the demand for materials planning is done in close cooperation and consultation with the purchasing department is we- equipped with the economies of purchasing. Hence, materials planning may carry meaning and prove result – yielding if purchasing department of the organization is actively associated at all the stages and at all the levels.

5.7 TECHINIQUES OF MATERIALS PLANNING

The under mentioned two techniques are usually used for materials planning:

1. Bill of Materials Technique, and

2. Past consumption Analysis Technique.

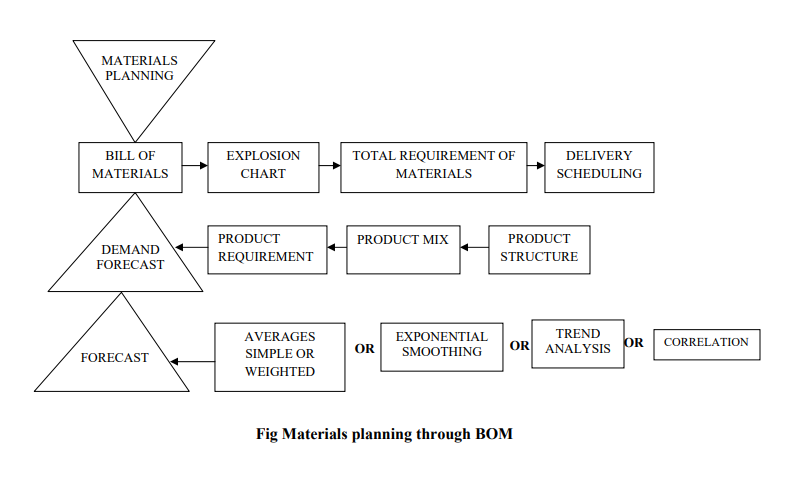

Bill of Materials Technique

A bill of materials indicates the name, part, and usage of each component and the sub- assembly in which it is to be used. Each product has a bill of materials since each of the products has its own equipments dependent on its design and according to the engineering designs and the components consisting of standard parts need for particular product to be manufacture. If a chair is to be prepared it can be split into legs , arms, seat, back rest. Each of the parts of the chair will have separate specifications and naturally each may have its own manufacturing design. According to the specifications and design, the bill of materials will be drawn on such composite

information for the product – the chair in this case. In a bill of materials for a product, the components required may be procured according to the specifications.

When any of the units of the organization receives a work order or production programme is finalized, the concerned foreman prepares a list of all the materials required for the execution of the order or manufacturing of the product as per production programme. The list of materials so prepared is known as a bill of Materials which includes all the details as regards to quality,

quantity, code number, and other necessary specifications, etc.

Once the production programme is finalized, each product is exploded (split) into its basic requirements with the help of it’s of materials. The number required per item is multiplied by the number to be produced in order to arrive at the total requirement. The total requirements are further adjusted for various losses. Rejections should also be provided for. Every care should make for them. Provisions for stock and lead time consumption should be made. Taking all these provisions into consideration the bill for materials should be drawn for each component and then through multiplication process total requirement should be obtained.

The bill of materials – known as BOM – is the simplest technique of materials planning .BOM with required lead -time and necessary contingency provisions is drawn which eventually turns into indents for procurement. it also acts as a guide to delivery and inventory requirement. BOM, therefore, helps in keeping watch over the delivery of matching equipments, spare part, and components and also over materials directly going into production. It enables the evaluation of the progress of the project undertaken and ensures the flow of need materials. Such an avoidance of capital blockage saves and diverts the working capital and reduces the inventory carrying cost to a larger extent.

Explosion of Bill of materials

Explosion of bill of materials refers to splitting of the requirements for the product to be manufactured into its basic components; then by multiplication process we get the total equipments. This is very effectively done with the help of “demand forecasts”. As we have seen earlier, the very basis for material planning is the forecast of demand for the end products. For calculation of equipments for various materials, explosion charts, are conveniently used by the materials department. An explosion chart is a series of bills of materials grouped together by combing the requirements for a particular end – product or group of end – products. The above

discussion may best be explained with help of the following chart;

Period and Suitability of BOM Technique

Bill of materials technique is ideally suited to engineering industries – both heavy and light since her large numbers of components are required for manufacturing or assembling and end-product which certainly required from various sources, which, as we have seen, is a convenient method of knowing the total requirements for an end product. There may be controversy so far as the period is concerned. It may vary from a month to a year depending upon the reliability of information and forecasts made. A forecast tends to become less

reliable as the period goes on increasing.

Forecasts amply prove that they are reliable only to the extent to which the information and data are reliable. If prejudices and personal pride has not crept in and the fed data are nearly absolute, unbiased, and are based on sound judgment, then the forecasts may serve the purpose well and period may even exceed one year. But seldom had these conditions adequately fulfilled. It is because of this reason that ideal period for materials planning are advocated to be of three months. Planning on a quarterly basis is also safe in the present state of Kenyan economy in which inflationary pressure is upsetting all calculations and market conditions are far from satisfactory from both demand and supply points of view.

Owing to error in forecasting or change in the market conditions and the national or state policy the materials (either all or some of them) may either be in short supply or in excess. This surely would upset the plans, programmes and schedules. A materials planning done on a quarterly basis may rectify the errors, apply the correctives and bring the operation on the right track which in case of annual (or more) planning is rather difficult, if not altogether impossible.

Past Consumption Analysis Technique

Where materials are consumed on continuous basis, the technique of past consumption analysis for materials planning is conveniently used by the organization. According to this technique, future projection is made on the basis of the past consumption data, which is analyzed taking into account the past as well as future production plans. Statistical tools like mean, median, mode and standard

deviation are used in analyzing the past consumption, projecting the future and tackling mild as well as wild fluctuations in consumption. This technique can be successfully used in process industries. This technique can be fruitfully used for materials being used on continuous basis for which no straightforward norms of consumption can be easily worked out in the organization, and also for those materials which are either used directly or indirectly in the production process.

5.8 SOME GUIDELINES FOR MATERIALS PLANNING

Though for every organization guidelines cannot be provided in a limited treatise like the present one but some of the general guidelines can be given which can be kept into mind and effectively used by a materials planner for effective and reliable planning.

1. A long lead time

Lead time should be kept as long as possible to provide cover for the unforeseen circumstances which may crop up during the planning period.

2. Analysis of operating environment

Careful analysis of operating environment of the firm is a must in order to guard against possible demand fluctuations and seasonal variations.

3. A shorter plan period

A shorter materials plan period ensures reliability. Fortnightly or monthly materials plan period is an ideal one. However, in Kenya quarterly plans are popular though a quarter is not considered to be a shorter period for a materials plan this is sorter one. For a quarterly materials plan analysis of operating environment becomes more or less a necessity. Also lead time calls for proper scrutiny

and sound judgment.

4. Computerization

Computerization of materials planning process saves time and energy and helps in accurate forecasting. A system effecting saving in time and energy and offering better scope for accurate forecasting is naturally ideal for any materials planning particularly when materials planning are being done in advesse conditions and where economy is fast changing and is not conducive to desired and healthy growth of industries, trade and commerce. In such an economy one is required to handle wild demand fluctuations, and a materials manager, in such a situation, is left with no alternative but to revise his materials plans off and on with every demand fluctuation and change in economic situation. Here computerization of materials planning process comes to the rescue of a

materials planner. Computerization of the process may help in effecting a change even within the shortest period of 24 hours. Obviously computerization goes a long way in proving the utility of materials planning and its fruitfulness in production planning programming and scheduling.

5.9 MATERIALS BUDGETING

A budget is a co-ordinated financial estimate of the income and expenditure of an organization related to a specified future period. It may be defined as “Budget is a plan of action quantified in money terms for some future period”

A budget serves the following purposes:-

- Planning the activities of various departments,

- Controlling such activities of the departments

- Fixation of objectives and targets of all such activities of the departments

- Closely watching the performance of various departments

- Detection of deviations etc, if there is any and

- Application of correctives so as to help in achieving the objectives and targets.

Materials budgets

A materials budget is coordinated estimate of the consumption and purchases of materials in an organizations relating to a specified period. The purp9ose of a materials budget is:-

1. To plan and control purchases

2. To asses and make a provision for the financial requirement of such purchases

3. To plan and control the production schedule.

4. To watch the activities of the purchases and materials control departments.

5. To suggest ways and means of improvements in the next budget estimate.

Factors governing drawing up of a materials budget

The following are the main factors which govern drawing up a materials budget

- The past rate of consumption and its ratio with production. The rate of consumption plays a vital role in framing a materials budget since it is a factor which gives two important points for careful study so as to help forming correct estimate of materials for the ensuing period that is period-to-period consumption of materials in relation to production programme and the product produced. And period-to-period investment made. The ratio of consumption and consequent production is also important as it helps in taking a decision on the future course of action, particularly production planning, purchases and sales planning which

are directly dependent on this ratio. - The production program me of the future specified period for which the materials budgets is intended. Production programme is obviously one of the important factors of the materials budget. It is the very basis of a materials budget. No one can plan anything or estimate a future course of action unless he is in the know of the objectives and targets to be achieved. And for achieving the target a budget is required. The rate of consumption may remain more or less the same for a labourer or a machine, but it often varies with the variance in production programme. The rate of consumption is directly related to the

production programme which one has set for oneself and a materials budget is governed and guided by this factor to a great extent. - The financial burden and investment pattern. No amount of good intention on the part of production programmes will help them in achieving targets and objectives unless backed by a good financial commitment and a well-set out investment pattern. The main task of the framers of materials budget is to allocate available funds in a manner in which maximum value is extracted from them without disturbing the production programme. Here the efficiency of the framers is put to test and the very success of a budget depends on the proper allocation of funds. The means in every organization are scarce and the uses numerous. Tactful and intelligent utilization will lessen the financial burden and set out a well-planned and effective investment pattern.

- The materials cost. This factor too affects the materials budget in the sense that it directly influences the financial commitment of the organization. A study, therefore, of the cost trend of the materials is required. Future trend has also to be studied and incorporated while preparing a materials budget.

- The demand and supply curve. Here also study of market conditions pertaining to the demand and supply trend is to be made before venturing to draw up a materials budget as the production schedule and financial commitments have to be adjusted according to the trend in the market. A forecast, correct one, may for a long way in achieving the purpose of materials budgeting. While setting a demand curve due care should be taken of the storage loss due to circumstances beyond human control, such as floods, transport bottlenecks, war etc.

5.10 Materials budgeting and accounting

From the above it is evident that accounting has to play a very important role in materials budgeting. The adequate help of cost and stores accounting by way of providing up to-date, reliable and required data to the materials control department enables it to base it forecasts on the data so supplied. The cost and stores accounting are both to supply the required information. Both of them are complementary to each other in this respect. To watch the performance and to suggest corrective measures, the help of accounting has to be taken. Hence accounting and materials budgeting together for achieving the set objectives of the organization.

Materials’ budgeting helps in controlling the cost and thus makes the organization cost conscious. Cost consciousness in turn makes the organization productivity conscious. Every material requisition is considered according to its necessity, every man-hour is utilized to its fullest capacity and every shilling spent is made to prove its worth. This is achieving through cost and result analysis which is possible only through accounting. Since materials budgeting aims at cost reduction, accounting again comes to the fore for making the budget result, producing.

Techniques of drawing up materials budgets

One of the following positively correlated techniques is generally made use of for drawing up a materials budget

- Budget summaries

- Manufacturing and trading account

- Savings on investments in materials

Budget summaries

Budget summaries are summaries of various individual budgets of the organizations. They placed in proper relationship with one another. They are viewed and analyzed and help is taken from them in arriving at a certain conclusion for the purpose of incorporation of a figure in a budget estimate. A material budget is grown up in relation to production, sales and purchase budgets. Budgets

summaries help in correlating each one of them in broader perspective as budget summaries, usually accompanied by reports, which at a greater length, deal with the variances and their reactions, and are helpful in drawing conclusion for the next budget estimates.

The merits of the technique

- Budget summaries are concrete numerical standards which provide a good base for the next budget estimates

- Budget summaries describe the position briefly and are arranged in such and analytical and comparable from that they help in drawing conclusions correctly.

- Budget summaries throw light on the activities of various departments. This makes planning effective. Also objectives get correct definition. Thus implementations part of the budget estimates becomes an easy task.

The limitations of the technique

- Budget variations are always there. The variations may be of minor as well as of major nature. Budget summaries may give equal importance to both types of variations which ought not to have been treated on equal terms. The conclusions and consequently, next budget estimates may give a picture which may not be a true one.

- Budget figures are often manipulated so as to balance the requirements and funds available. This may result in faulty conclusions and thus the next budget estimate may also become faulty. In such cases, budgetary control may also be a troublesome and irksome job.

- Budget summaries are merely numerical standards. They speak only about estimates and a little bit of performance, but they do not ensure profitable operations. No clear picture thus emerges from budget summaries so far as the profitable operation the business is concerned.

Manufacturing and trading account

This technique is comparatively result-oriented as it is based on the performance of the budget viss-vis the results. This account reveals in detail various items relating to the opening stock purchases expenses on purchases, production, closing stock, working –in-progress, etc, and finally the cost of production and profit made out of manufacturing and trading process. This account is a

good base, rather a good applied technique for budget estimates. Of course, budget summaries cannot be done away with. The positive help such summaries are of immense value for the framers of materials budget.

The merits of the technique

- This technique is result-oriented and thus a good base for budget estimates

- It stresses profitability aspect on each of the correlated budgets of the various departments.

Thus efficiency and performance become the keynote of various budgets. - Pro rata analysis of the result is possible. Thus periodical and flexible budgets become a possibility.

The limitations of the technique

- It involves much paper work and thus becomes too heavy a burden for an organization of relatively small size.

- There may be cases in which proper allocation of expenses to one or other of the items may not be feasible. Wrong inferences, thus may be drawn.

- The result-oriented budget framing technique may result in interdepartmental rivalry which ultimately may not prove to be good for the organization as a whole.

Savings on investments in materials

The overall performance of an organization can be judged by the profit it has made during a specified period and a budget is a means to setting the objective of profit-making in a right perspective through its estimates based on returns on investment. The materials budget consumes the major portion of funds available in the organization; hence it is appropriate to measure the performance of materials budget by finding out the savings on the investments made in the past and possible expected savings in future. The amount of savings achieved by any materials budget effectively is the success of any materials budget and this can be better judged by the ratio of savings and investment in materials.

The ratio of savings achieved to total investment as budget may be analyzed on the basis of the following equations.

Saving = Savings X Value of materials utilized

Investment Value of materials utilized Investment

Or

Value of products – cost of products = Value of materials utilized

Value of materials utilized Investment

The merits of technique

- Objectives are clearly defined, which give a realistic approach in materials budgeting.

- It can also be effectively used in other inter-related departments

- As detailed analysis is possible, a remedial action for disturbing trends may be taken.

- It makes possible the effective use of scarce means available to the organization.

The limitations of the technique

- It lays too much emphasis on the financial aspects. Other important factors which may curtail the investment and achieve savings are not taken care of.

- The savings so arrived at are based on past performances. Future budgeting is based on calculations. But the circumstances in which the savings are achieved may not be present in the budget year in question. The result, thus, may be misleading.

- Much paper work, labour and calculations are required, but they may not worthwhile for a small-sized business.

Before choosing any one of the techniques discussed above, the framers of materials budget should take into consideration the points enumerated below.

- The objective and policies of the organization. Budget is a means and not an end in itself, hence a well defined objective and policy will ensure effective materials budgets, otherwise, it will simply be a waste of time, money and energy.

- The period of budget: budget, whether material or any other, may be of short term or long term. Generally, a materials budget is of short term. The short term may also be of three months, six months or even one year. This makes a materials budget more effective and result producing.

- The data available. As has been discussed in the foregoing pages, the data, if available as required, may make or mar the success and the effectiveness of a budget. In all the three techniques discussed above the availability of reliable, perfect, up-to-date and analytical data is very essential.

- Flexibility of budget. The flexibility of budget, particularly materials budget, is one of the important points to be taken note of. The materials are subject to various kinds of losses during the storage process, their demand may increase or decrease according to changes in the production schedule. This requires flexibility so as to make adjustments according to circumstances.

- Repetition of past targets. Business is a growing and going venture. Repetition of past targets in any budgetary provision is always in bad taste. It reflects the unconcerned attitude of those who are responsible for running the organization. A change towards betterment should always be the motto of the framers of any kind of budget.

Purchasing Plan and Materials Budget can only be fixed to the accuracy of Sales and Production

Forecasts – normally not accurate to annual basis but requirement adjustment throughout the production year

Materials Budget contains information concerning:

• Estimated materials prices for the period

• Timing of purchases to establish obligation rates for the period .

Forward buying can be arranged commensurate with planning levels and accuracy.

• Forward buying attempts to purchase quantities to levels approximating foreseeable requirements.

• “Hand to Mouth” buying is buying material to satisfy current operating requirements, oftentimes at less than optimum economic quantities.

Forward buying consists of advanced arrangements such as:

• Blanket Purchase Agreements

• Contract Purchases (IDIQ, Requirements, etc.)

Long term forward buying arrangements should include provisions to mitigate risks associated with market volatility (swings either upward, to protect supplier, or downward, to protect buyer)

Market Stability influences purchase timing

• Stable markets may allow orderly purchases of uniform quantities

• Unstable markets may provide opportunities to be either seized or avoided

• Proper market timing can be a hedge against rising prices of commodities

Volume purchased can influence prices (and also the cost of capital) while avoiding the negative impact of numerous small purchases. Acquisition strategy and contract type are important here.

It is important to emphasize that Strategic Materials Planning considers long-term material requirements and market projections

• In strategic materials planning, the focus is on the corporate position over the long haul, not short term gratification

• Potentially critical materials for future needs are identified and sources developed

• Consumer demand and product/materials innovation must be considered

• Political and economic environments in source countries must be assessed

• Competitor demands for like commodities must be considered

• Strategic materials planning should maximize benefits derived from second or alternative sourcing agreements by injecting competition, ensuring product availability

• Materials projected in short supply should be considered for substitution/replacement and vice versa

• Make or buy decisions should be included where outsourcing of components is a concern or potentially risky