Stock is the term used for all type of goods or materials in a stock room or store room until they are needed e.g.

- Manufacturing firms stock raw materials and finished goods

- Goods in a shop for sale are referred to as stock

- Offices have their own stationery stores and keep their own stock records. Office stationary or consumable office supplies comprise the materials which are used in the administration of office work.

TYPES OF OFFICE STATIONERY

- Types of paper sizes

- These are types of paper used and correspondence. There are two main kinds of paper sizes

- The traditional system of foolscap, quarto, sexton and octavo sizes dating back many years

- The more recently introduced international A, B and C sizes

- The most widely used of these is the A series

- The B series is intended for large items such as posters and wall charts

- The C series is used for envelopes

Here are examples of some of the common uses of the different sizes of paper

- A3 used for legal documents, balance sheets and financial statements

- A4 is used for business letters, reports, minutes, agenda, specifications, bills of quantities, estimates, invoices, quotations

- A5 used for short letters, memos, invoices (small), credit note, statements

- A6 used for postcards, index cards, requisition, petty cash vouchers, compliment slips

A7 used for business visiting cards, labels

- Types of Paper Quantities i.e. How are quantities of stationery measured

- Ream – 480 or 500 sheets of paper

- Quire – 24 or 25 sheets of paper, stencils or carbon paper

- Dozen – 12 sheets of paper

- Gross – 144 envelopes, memo pads, books, etc.

- Types of Paper Quality

The types of paper most frequently used in office work are:

- Blank (flimsy) paper – relatively cheap, soft kind of paper used for carbon copies and set of forms

- Bond – it is harder, whiter, smoother paper used for letter heads and typing top copies

- Air mail paper – a good quality, very thin, light weight paper used for correspondence sent by airmail

- Art paper – which is non-absorbent glossy paper and is used for spirit duplicating

- Duplicating paper – which is absorbent to permit rapid drying of ink and is used for stencil duplicating

- Carbon paper – which is thin, usually black paper coated with carbon deposit and is used to produce both handwritten and typewritten copies

- Copier bond – for use in copiers, that is, photocopying machine. Usually this paper is treated to reduce tendencies of sheets stinking together and jamming in the machine

- Envelopes

International envelope sizes

C3 324 mm x 458 mm

C4 229 mm x 324 mm

C5 162 mm x 229 mm

C6 114 mm x 162 mm

DL 110 mm x 220 mm

C7/6 81 mm x 114 mm

TYPES OF ENVELOPES

- Banker – the opening is on the longer side

- Window – contains a window opening with transparent material covering it for the typist to type the name and address on the envelope

- Pocket – the opening is on the shorter side

3. Aperture – the address panel is uncovered i.e. the window opening doesn’t have any transparent material covering it

4. Continuous stationery – refers to sets of printed forms joined together into a continuous strip and separated from one another by perforations. Reproduction of copies is usually by means of one-time carbon or carbon backing i.e. no carbon required. Continuous stationery is useful for any form which is pre-printed, frequently used and needs several copies at the same time.

Main uses of continuous stationery are sales invoices, cash sales, local purchase orders and wage sheets

Advantages of Continuous Stationery

- It saves in form filling

- Simultaneous copies can be obtained

- Helps to achieve uniformity in the use of forms

- Neatness is maintained because there is no handling of carbon copies

- No skill is required, office staff can use them easily

Disadvantages

- It is more expensive than ordinary forms

- Mistakes cannot be easily corrected

- Bottoms copies may appear faint

- Can be spoiled easily causing wastage

- Accidental pressure is likely to make marks on the copies

- OFFICE FORMS

A form is a printed piece of paper or card on which entries are made by hand or typing against marked headings e.g. invoices, debit notes, credit notes, local purchase orders, application forms, e.t.c.

ESSENTIALS OF A GOOD OFFICE FORM/FACTORS TO CONSIDER WHEN DESIGNING FORMS

- Proper title – every form should have a proper title so that the person who reads or records on it knows the purpose of the form. The title should be short, concise and clearly printed at the top

- Logical sequence – information should be arranged in a local order to enable information to be sought easily, quickly and correctly

- Spacing – spaces for entries should be adequate for information sought

- Adequate margins at the left – right, top and bottom. Left margins are punched for filing purposes

- Various sections of the form should be properly separated so that it is easy to complete and extract information from it

- Style of print used – should ensure the form is read with ease in natural and artificial light

- Proper size – as standard size of a form should be fixed to avoid wastage of paper

- There should be a distinction between forms e.g. credit notes printed in red, debit notes in blue

- Both sides printing – printing both sides of the form to eliminate additional sheet of paper. The word P.T.O should be printed on the bottom edge of the front of the forms

- There should be a distinction between forms e.g. credit notes printed in red, debit notes in blue

- Proper type of paper – this depends on the length of period of preservation, method of handling, appearance desired and impression desired

- Numerical identification – each form must have a control number of easy identification. This number is essential for requesting purchasing, storing and ordering

BENEFITS OFFICE FORMS

- Preservation of records – Forms help to preserve records of business for filing and future reference

- Aid to office systems and routines. No office system can afford to function smoothly without them

- Better customer service – customers can be served better if proper forms exist since their records can be preserved with greater ease

- Saving in time – they save time as they eliminate the need for recopying repetitive or standard information and thus prove economical in the long-run

- Goodwill – good forms also help project a good image of the organization amongst public. They are thus a good investment from the point of view of the organization

- Better human relations – Good forms also promote better human relations in the organization. The labor is assured of proper record-keeping of their work, wages, bonuses and retirement benefits

- Better services to shareholders and creditors – good forms make for better service to shareholders and creditors

COMMON FAULTS THAT MAY BE FOUND IN FORM DESIGN

- Insufficient horizontal space for filling the expected information

- Lack of printed lines where information is to be handwritten

- Too much printed information that tends to bore the person filling or reading the information

- Lack of proper identification of forms so that a form for one purpose can be confused for a form of different purpose

- Poor separation of various sections of the form which makes it difficult and confusing to complete and to extract information from it.

- Inadequate left margin which does not allow for filing without destroying some of the information

OTHER ITEMS OF OFFICE STATIONERY INCLUDE

- Pens, pencils, rubbers or erasers

- Paper clips, pins and staples

- Typewriter or printer ribbons

- Shorthand note books

- Files and folders

- Adhesive tape labels

- Books, fullscaps, writing papers

- Stencil correcting fluid

- Laser toner , petty cash vouchers

- Floppy disks, compact disks

- Post cards, memo forms

- Telephone message forms

- Computer printout paper

- String, compliment slips

WHATEVER TYPE OF STOCK EFFICIENT STOCK CONTROL INCLUDES THE FOLLOWING

- An efficient buying department. In most organization this is the responsibility of the purchasing department

- Proper storage facilities

- Keeping accurate stock records

- Efficiency in the issue of stationery

- Undertaking stock taking regularly and properly

- Carrying out stock valuation for the purpose of preparing financial account

MEASURES TAKEN TO ENSURE PROPER CONTROL OF OFFICE STATIONERY

- Ensuring there is an efficient buying department so that the organization can make bulk purchases and be able to obtain quantity discounts

- Having proper storage facilities for stationery to avoid damage and deterioration/theft

- Having an efficient issuing system where issues are made against requisitions signed by authorized officials to avoid abnormally large requisitions/ wastage/misuse

- Keeping proper stock records so as to be able to maintain stock levels. Maximum sock levels avoids overstocking which ties down capital and reduces office space, re-order levels ensures continuous supply of stationery so that firm’s activities are not held up due to stock running out and minimum levels avoids under stocking and it is a danger level to follow up orders on hand not yet delivered

- Undertaking stock taking regularly and properly in order to compare balances appearing on stock records with the actual stocks and if there is a difference, find out the cause e.g. frauds, misuse or wastage, misappropriation, pilferage/theft

- Carrying out stock valuation, that is, finding out the stocks worth in terms of money for the purpose of preparing the financial account

BENEFITS OF CENTRALIZED SYSTEM OF PURCHASING STOCK

- Lower cost – centralized buying means buying in bulk. Thus savings in costs are made. Buying in bulk means lower purchase price per unit, availing quantity discounts and saving on freight, insurance, etc. Buying can be directly from the suppliers assuming lower costs and constant supplies.

- Specialist function – centralized organized purchasing section or department allows for specialization of purchasing function. This allows the organization to evaluate various available supplies thoroughly and pick up the most reliable product and the source of supply

- Better budgetary control – centralized purchasing allows for better budgetary control since a single purchasing officer supervises the purchases

- Help in standardization of forms – central purchasing also makes it possible to standardize forms which may prove a great benefit to the organization.

Disadvantages

- Lack flexibility – centralization of stationery purchasing lacks flexibility in more than one aspect. Centralization may result in poor response to urgent requests for supplies. Besides the quality of supplies may not suit the purpose of which they have been purchased because of lack of knowledge of requirements

- Unsuited for dispersed units/divisions/branches/departments – the method may prove to be inadequate where different consuming departments are located wide apart e.g. in different cities

- Greater cost of organizations – the overhead cost of organizing centralized purchase may be very high since separate staff accompanying facilities will have to be provided for the purpose. Thus a smaller organization with scattered departments my find it very costly to have a centralize purchasing department

FACTORS TO CONSIDER WHEN ORDERING/BUYING STATIONERY

- Quality – material should be durable and presentable. Quality is greatly influenced by the purpose for which the item is going to be used

- Delivery dates – chooses a reliable supplier who will meet set dates

- Discount – buy large quantities of fast moving items to take advantage of quantity discounts

- Alternative suppliers – have an alternative supplier against the eventuality that the regular supplier is at one time unable to supply

- Stock level – set realistic figures for minimum levels and do not hold large stocks of slow moving items

- Consider the funds available in the business and buy stationery which is extremely needed.

METHODS OF PURCHASING STATIONERY

- Spot purchase e.g. from a sales representative who calls in an office.

- System of quotation – different firms submit quotations to the buyer. It takes more staff time than the tender system but ensures best market price is obtained for each item of goods required.

- Contract for a long period – go into agreement to supply for a certain stated period of time for a set price. Supplier offers good quality of goods and services.

- Tender of supply for a long period – buyer advertises in the newspapers and invites stationery manufacturers to offer (tender) their prices for the different lots. Buyer can get cash and quantity discounts. Lower tender not always the best supplier.

MEASURES TAKEN TO ENSURE EFFICIENCY IN THE STORAGE OF STOCK

- Allocate a central store room for housing stocks of stationery and other suppliers for easy reach.

- Stock is stored in a clean, dry, well lit room.

- Keep storage areas (they may be rooms or cupboards within a room) locked. Materials are often portable and liable to indiscriminate usage and pilfering.

- Stock is stored in open shelves or cupboards and printed matter in their own wrapping paper.

- All stock is clearly labeled for easy access

- News suppliers should go to the back, old stock should be brought forward. This is known as the FIFO principle (First In, First Out).

- Place heavy items on the lower shelves and arrange the items used frequently in the most accessible positions.

- Store any highly inflammable materials in sealed containers and preferably in a metal cabinet.

- Prohibit smoking in the store room.

TYPES OF STOCK RECORDS

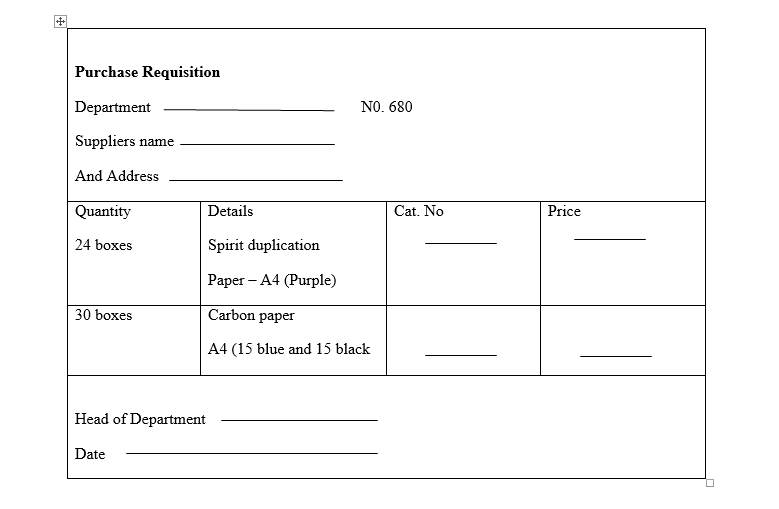

- Purchase Requisition – it is filled by the stationery clerk when making request for fresh supplies from the purchasing department to help them in replenishing the stock.

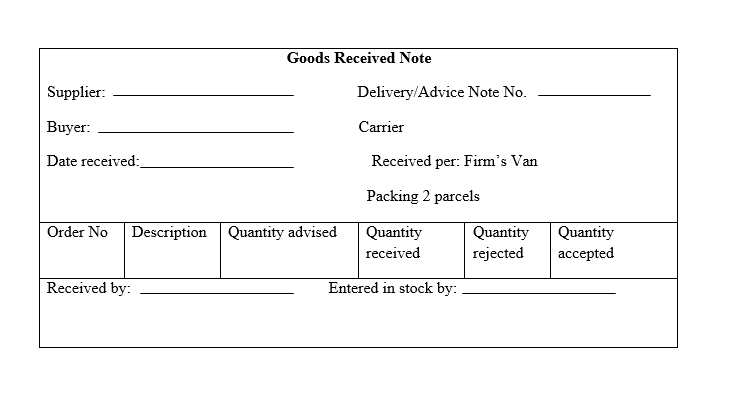

2. Goods Received Note – it shows receipts of stock from suppliers, that is, upon delivery of stock from suppliers the stock is checked and goods received note is prepared. This document shows the name of the supplier, the quantity and description of goods and the date on which they were received and signature of the checker.

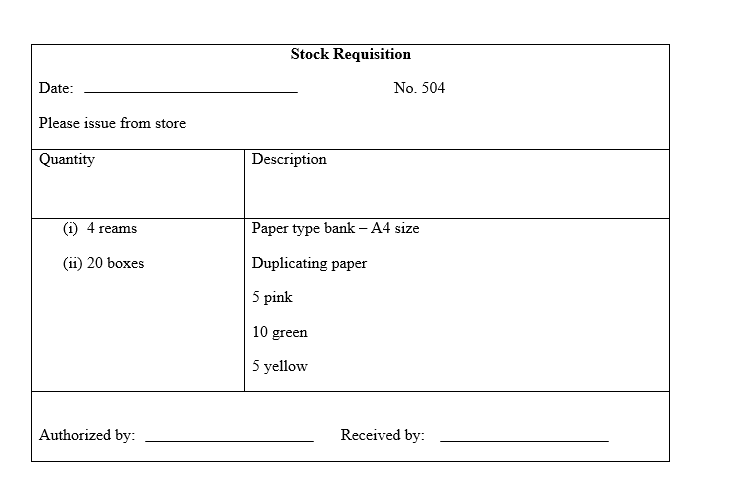

3. Stock Requisition Form – used to record issues or stock to users. Each requisition is numbered for reference purposes and a space is provided for the signature of the person authorized to sign it.

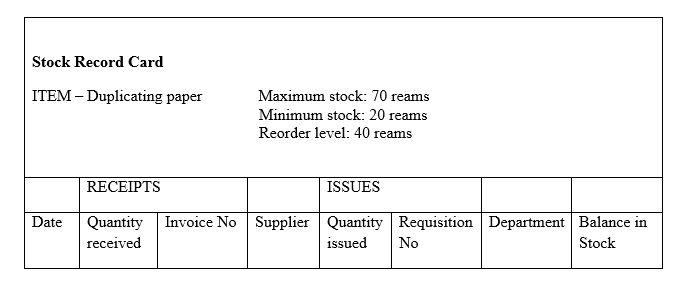

4. Stock Record Card – it is a document that shows clearly the stock receipts, issues and quantity of stock at a given time. The contents of a stock record card include:

- Date – there should be a date indicating when the goods were received and issued to respective departments.

- Stock reference number – this is a reference assigned to each item or group items. When stock is received or issued, the appropriate card is obtained and the new information is recorded in the card.

- Receipts – the stores clerk records the information from the goods received note to the stock record card. This information includes:

- The quantity received

- The invoice number

- The name of the supplier

- Issues – the stores clerk records the stock issued to respective departments. This information includes:

- Quantity issued

- The requisition note number

- The department requisitioning

- Balance in stock – this section shows how many articles remain in stock after the receipts have been added to the previous balance and the issues have been subtracted.

- Stock levels – this section is usually found at the top of the stock record card and it indicates

- Maximum stock level – this is the level beyond which stocks should not exceed

- Re-order level – this is the point at which new orders are placed to replenish the stock.

- Minimum stock level – the level below which stock should not go.

WHY IT IS IMPORTANT TO KEEP STOCK RECORDS

- To minimize overstocking which ties down capital and reduces storage space.

- To ensure a continuous supply of stationery so that a firm’s activities are not held up due to stock running out

- To help keep an accurate check on the quantities of stock to avoid theft.

- To avoid storing stock which is inactive or slow moving which can lead to obsoleteness (being outdated) or deterioration.

- To avoid wastage of stock by determining the consumption level of each department.

- Helps in the quick location of goods through the use of stock reference number.

MEASURES THAT WOULD ENSURE EFFICIENCY IN THE ISSUE OF STATIONERY

- Issues should only be made on written requisition signed by authorized officials

- Specific times should be set for stock issues e.g. one particular day in a week or between certain hours each day

- A signature should be obtained once stock has been issued

- Abnormally large requisitions should be queried to keep consumption down to a minimum. Therefore it is important to know size of departments and their usual requirements

- Keeping a record of each item of stock to indicate how much has been issued

- Staff should think of their stationery requirements ahead of time to avoid panic requisition

- The storekeeper should be trained and qualified to the issuing effectively

METHODS OF STOCK-TAKING

- Perpetual stock taking – it involves recording of all receipts, issues and balances of each item on a stock record card after each transaction

- Periodic stock taking – it involves ascertaining the physical quantities of stock in hand at fixed intervals e.g. annually, half yearly or quarterly. Business is closed so that stock is counted, classified and valued

- Continuous stock taking – this is checking continuously recorded balances on the stock record card of a few items against their physical balances at random by independent persons, for example, those from accounts department and not the store keeper. This is carried out until all items have been checked after some period and any discrepancies are investigated. It means, therefore, within a period of a year the items have been checked 3 – 4 (or even more) times

STOCK VALUATION

It means attaching a monetary value to the stock or finding the stocks worth in terms of money.

METHODS OF STOCK VALUATION

- The specific method – each item or batch of items is priced out at its specific cost. The method is most suitable for bulk stocks and for very expensive items of stocks

- First in, first out (FIFO) – old stock is used first before new stock. Values given is for news stock so stock reflects current prices

- Last in, first out (LIFO) – new stock is used first before the old stock. Values given is for old stock so stock doesn’t reflect current prices

- Average cost method – add up the value of the stock that came in last and that which came in first and divide by two

LIFO+FIFO = Average cost method

2

- Standard cost system – estimated standard prices are used over a period for valuing stock regardless of the actual cost

WHY A GOOD SYSTEM OF STOCK CONTROL IS IMPORTANT IN ANY ORGANIZATION

- To avoid having too much capital tied up in stock

- Excess stock requires additional storage space and space cost money. Therefore, there is need to avoid overstocking

- Too little stock (if held) can interrupt day-to-day running of business because of lack of supplies

- With incorrect records or no records at all it is easy to lose goods through damage, deterioration or pilferage/theft

- Good stock control reports on inactive stocks which can lead to being outdated/obsolete/deteriorate

- To enable stock to be valued

EXPLAIN HOW WASTAGE OF STATIONERY CAN BE CONTROLLED

Wastage of stationery can be cause by poor buying methods, overstocking, poor systems of control over issue, inadequate re-order and minimum levels, inadequate or unsuitable storage space and acceptance of unsuitable materials and substitutes.

TO REDUCE WASTAGE THE FOLLOWING STEPS CAN BE TAKEN

- Efficient buying – centralized buying ensures that stationery is bought in large quantities by coordinating all departments so as to get quantity discounts

- Stock room – some items of stationery require special storage to avoid deterioration hence items must be stored according to specifications of the manufacturers

- Stationery level – stock levels must be set to include maximum, minimum and re-order level, maximum levels should not be by passed because it will mean tying money unnecessarily by overstocking, minimum levels ensure there is no under stocking, re-order levels ensure there is no running out of stock before new stocks are delivered

- Issuing system – stationery is issued after written requisitions officially approved have been presented and stationery should be collected at given times of day or week

- Control of consumption – consumption of stationery should be kept to a minimum by making those who sign for it to be responsible. This can be done by informing all the consuming departments, how much they are consuming and asking them to make sure that their consumption is within their budget

- Stock should be inspected regularly to determine what is not being used and therefore reduce ordering of such items

- Physical stock-taking should be done to compare balances appearing on stock records with the actual stocks and any misuse or wastage or misappropriation should be addressed

REVISION QUESTIONS

- List three methods that a large firm may use to purchase stationery

- Explain four benefits that an organization may derive from centralized purchase stationery

- Explain four measures that may be taken by the Office Manager to ensure proper consumption of stationery or measures to control or avoid misuse of stationery.

- State three types of information contained in a stock record card

- Outline the characteristics of a well-designed form or the principles for designing office forms.

- Outline the reasons that make it necessary to control office supplies.

- Outline three faults that should be avoided in form design to allow for their effective use or the indicators of poorly designed office forms.

- Explain five benefits that an organization may derive from properly designed office forms.

- Outline five guidelines that an Office Manager should follow to ensure that the right level of stationery is maintained in the office

- Explain the factors that should be considered when buying office stationery

- Highlight six measures that a supplies officer may take to ensure office supplies are stored in good condition

- Explain four reasons why an organization may find it necessary to maintain stock records or benefits of keeping accurate record of stock in an organization

- Measures to control the cost of correspondence in an organization