THURSDAY: 4 August 2022. Morning paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Do NOT write anything on this paper.

QUESTION ONE

1. Explain the following terms as used in inventory management system:

Perpetual inventory system. (2 marks)

Periodic inventory system. (2 marks)

2. The following information relates to store receipts and issue of material R in a small manufacturing enterprise for the month of April 2022:

April: 1 Opening inventory 4,000 units at Sh100 per unit.

4 Issued 3,000 units.

5 Purchased 9,000 units at Sh.120 per unit.

9 Issued 3,200 units.

12 Returned to stores 2,000 units (from the issue of 4 April 2022).

15 Purchased 4,800 units at Sh.130 per unit.

18 Returned to supplier 400 units out of the quantity received on 5 April 2022.

25 Purchased 2,000 units at Sh.140 each.

28 Issued 4,200 units.

29 Purchased 2,400 units at Sh.150 per unit.

30 Issued 5,600 units.

It is the company’s policy to use the weighted average method when valuing the materials issued.

Required:

Store ledger account for the month of April 2022. (10 marks)

3. Turkwes Ltd. manufactures men suits for local market. Jobs are allocated to two operators; Njogu and Mabili with bonus paid for hours saved.

In the month of July 2022, Njogu made 100 units while Mabili made 105 units for which the time allowed of 60 standard minutes and 50 standard minutes per unit respectively was credited.

Additional information:

1. The basic wage rate was Sh.360 per hour for both employees.

2. For every hour saved, a bonus was paid at the rate of 25% of the basic wage rate.

3. Hours worked in excess were paid at the basic wage rate plus two thirds.

4. Njogu completed his job in 88 hours while Mabili completed his job in 78 hours.

5. A basic working week has 80 hours.

Required:

For each operator, determine:

Amount of bonus payable. (2 marks)

Total gross wage payable. (2 marks)

Wage cost per unit. (2 marks)

(Total: 20 marks)

QUESTION TWO

1. Distinguish between “flexible budget” and “activity based costing” as used in management accounting. (4 marks)

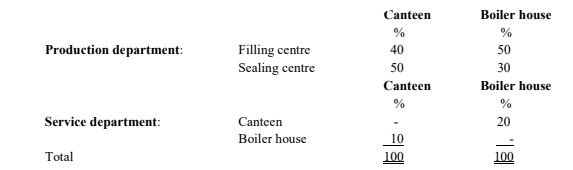

2. Betacare Enterprise produces several products which pass through two production departments in its factory. These two departments are concerned with filling and sealing operations. There are two service departments; canteen and boiler house in the factory.

Additional information:

1. Predetermined overheard absorptions rate, based on direct labour hours are established for the two production departments.

2. The budgeted expenditure for these two departments for the period just ended, including the appointments of service department overheads was as follows:

• Filling centre Sh.110,040

• Sealing centre Sh.53,300

3. Budgeted direct labour hours were 13,100 hours for filling cost centre and 10,250 hours for sealing cost centre.

4. Service department overheads are apportioned as follows:

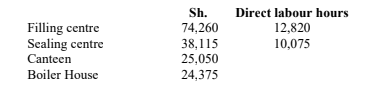

5. During the period just ended, actual overhead costs and activity were as follows:

5. During the period just ended, actual overhead costs and activity were as follows:

Required:

Reapportion and calculate the overheads absorption rates in each production cost centre using:

Stepwise technique. (7 marks)

Simultaneous technique. (7 marks)

Compute over or under absorption of overheads under 2 (ii) above for filling and sealing production departments. (2 marks)

(Total: 20 marks)

QUESTION THREE

1. Discuss six benefits that would accrue to a firm that uses break-even charts in making managerial decisions in its operations. (6 marks)

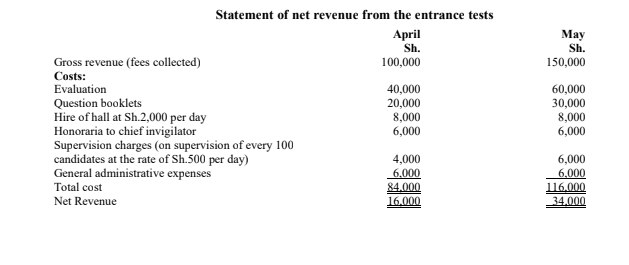

2. NIE Social Academy conducts an entrance test for every new student whereby a final selection of 100 students is made. The entrance test consists of four key areas and is spread over four days, one examination per day. Being a community based institution, each student is charged a fee of Sh.500 for taking up the test.

The following data relates to the two months in the previous holiday:

Required:

Budgeted net revenue for 4,000 students. (8 marks)

Break-even number of candidates. (4 marks)

Number of candidates to be enrolled if the net income desired is Sh.200,000 in the following month. (2 marks)

(Total: 20 marks)

QUESTION FOUR

1. Explain the term “industrial engineering technique” as used in cost estimation. (2 marks)

Highlight three advantages of the industrial engineering technique. (3 marks)

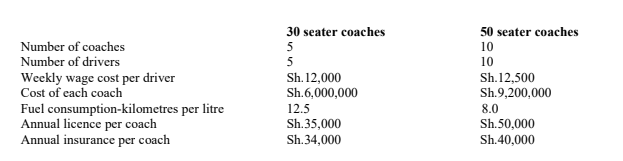

2.Zigzag Line Coaches Ltd. operates a fleet of executive coaches across the country.

The following information is provided:

Additional information:

1. Annual repairs and maintenance were budgeted at Sh.6,500,000 and are to be apportioned between the coaches in the ratio of their total mileage in kilometres covered.

2. Administrative expenses are budgeted at Sh.9,620,000 annually and are to be apportioned to each coach in the ratio of driver’s wage costs.

3. Each 30 seater coach is kept for 6 years at which it will have a resale value of Sh.2,400,000 while every 50 seater coach will be replaced after 7 years and have a resale value of Sh.2,900,000.

4. It is the policy of the company to depreciate the coaches on a straight line basis. Depreciation expense is charged annually.

5. It is envisaged that each 30 seater coach will travel 1,000 kilometres per week and each 50 seater coach will travel 800 kilometres per week.

6. The cost of the fuel is budgeted at Sh.120 per litre.

7. It is budgeted that each coach will be in operation for 50 weeks per year and the drivers will be paid for 52 weeks.

Required:

Cost per kilometer per passenger for:

30 seater coach. (8 marks)

50 seater coach. (7 marks)

(Total: 20 marks)

QUESTION FIVE

1. Describe four uses of management accounting information to a business entity. (8 marks)

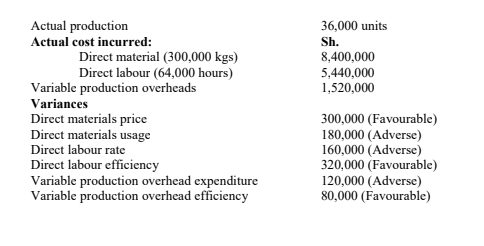

2. The following information relates to actual output costs and variances for the month of May 2022 for a single product branded “T” manufactured by KK Ltd.:

Additional information:

1. There was no opening or closing work-in-progress during the period.

2. Variable production overhead varies with labour hours worked.

3. The company operates the standard marginal costing system.

Required:

Standard cost card for product “T” for the month of May 2022. (12 marks)

(Total: 20 marks)