TOPIC ONE

INTRODUCTION TO STRATEGIC MANAGEMENT

Meaning of terms

Strategic management is a set of management decisions and actions that determines the long-run performance of a corporation. It includes environmental scanning, strategy formulation, strategy implementation and evaluation and control to achieve the objectives of an organization Art & science of formulating, implementing, and evaluating cross functional decisions that enable an organization to achieve its objectives.

The basic concept of strategic management consists of a continuous process of planning, monitoring, analyzing and assessing everything that is necessary for an organization to meet its goals and objectives.

In simple words, it is a management technique used to prepare the organization for the unforeseeable future.

Strategy management helps create a vision for an organization that helps to identify both predictable as well as unpredictable contingencies. It involves formulating and implementing appropriate strategies so the organization can attain sustainable competitive advantage.

There is some of basic strategic management key terms that need to be considered at the beginning in order to completely understand strategic management. These strategic management key terms are nine in numbers and are the base of strategic management.

1. Strategy

Strategy is a tactical course of action which is designed to achieve long term objectives. It is an art and science of planning and marshalling resources for their most efficient and effective use in a changing environment.

2. Strategists

These are in the organization that is fully responsible for the failure or success of the organization. Strategies are formed by strategists. Examples of strategists include chief executive officer, chair of board, chief executive officer, president & owner, entrepreneur or dean etc

3. Vision & Mission Statement

The first step in the strategic planning is to develop the vision statement and after that mission statement is prepared

a. Vision statement

A vision statement describes what a company desires to achieve in the long-run, generally in a time frame of five to ten years, or

sometimes even longer. It depicts a vision of what the company will look like in the future and sets a defined direction for the planning and execution of organizational -level strategies.

b. Mission statement

A mission statement is a short statement of why an organization exists, what its overall goal is, identifying the goal of its operations: what kind of product or service it provides, its primary customers or market, and its geographical region of operation. Mission and vision are statements from the organization that answer questions about who we are, what do we value, and where we’re going

4. External Opportunities & Threats

All those trends & events those are related to the social, economic, environmental, cultural, demographic, political, legal, technology & technology & competitive that can harm or benefit an organization constitute external opportunities & threats.

5. Internal Strengths & Weaknesses:

Those activities of the organization that are under control of the organization, and may show good and bad impact on the organization are known as internal strengths & weaknesses of organization. These are present in the marketing, management, production/operation, finance/accounting, and information technology & research & development activities of the organization.

6. Long Term Objectives:

Long Term Objectives are referred to as particular results that organization wants to accomplish in targeting the mission.

7. Strategies:

The means through which allow the organization to achieved long term objectives.

8. Annual Objectives:

Those short term targets that are helpful in achieving long term objectives of the organization are called annual objectives.

9. Policies:

Annual objectives are accomplished by the means of policies. Policies contain rules, guidelines & procedures developed to assist efforts to accomplish stated

objectives.

Roles of strategic management:

1. Development of company strategy and vision – It involves defining the vision and mission of the organization, which in essence means the purpose of its existence. It also involves the development of the company‘s strategy in order to chart out its future growth pattern based on some specific actions. Strategic management identifies what those actions will be and then shares those with the teams that implement.

2. Identification of products and markets – Growth for an organization means constant innovation to maintain its competitive edge as well as market share. One of the functions of strategic management is to identify the new products and new geographies that the organization needs to explore. It also means the evaluation of the viability of existing product, service and market, and assessment of whether to continue or not.

3. Focus on Company’s brand positioning – The company has a brand value and position that people identify it by. Strategic management means upholding, sustaining and reinforcing this brand positioning. This is done by ensuring that the strategy is aligned to the brand, as well as all the internal and external actions.

4. Alignment across businesses or departments – Strategic management ensures that no business segment or department in the organization is working in silos. When planning takes place, the views of all departments and businesses are considered. The final decisions are shared and discussed to ensure that there is an alignment of organizational purpose and goals. This is the role of strategic management.

5. Planning and Course Correction – Strategic management is all about planning for the business. This planning is similar to a SWOT analysis which identifies the new opportunities and threats to existing business as well. It also means that one of the functions is to course correct the business performance in case it is not following the right growth rate.

Factors that Shape Strategy

Organizations do not exist in a vacuum. Many factors enter into the forming of acompany’s strategy. Each exists within a complex network of environmental forces.

These forces, conditions, situations, events, and relationships over which the organization has little control are referred to collectively as the organization’s environment.

In general terms, environment can be broken down into three areas:

1. The macroenvironment, or general environment (remote environment) – that is, economic, social, political and legal systems in the country;

Economic Forces

Economic forces refer to the nature and direction of the economy in which business operates. Economic factors have a tremendous impact on business firms. The general state of the economy (e.g., depression, recession, recovery, or prosperity), interest rate, stage of the economic cycle, balance of payments, monetary policy, fiscal policy, are key variables in organizational investment, employment, and pricing decisions.

The impact of growth or decline in gross national product and increases or decreases in interest rates, inflation, and the value of the dollar are considered as prime examples of significant impact on business operations.

To assess the local situation, an organization might seek information concerning the economic base and future of the region and the effects of this outlook on wage rates, disposable income, unemployment, and the transportation and commercial base. The state of world economy is most critical for organizations operating in such areas.

Political and Regulatory Forces

Political-legal forces include the outcomes of elections, legislation, and court judgments, as well as the decisions rendered by various commissions and agencies. The political sector of the environment presents actual and potential restriction on the way an organization operates.

Among the most important government actions are: regulation, taxation, expenditure, takeover (creating a crown corporation, and privatization. The differences among local, national, and international subsectors of the political environment are often quite dramatic. Political instability in some areas makes the very form of government subject to revolutionary changes.

In addition the basic system of government and the laws the system promulgates, the political environment might include such issues as monitoring government policy toward income tax, relative influence of unions, and policies concerning utilization of natural resources.

Political activity may also have significant impacts on three additional governmental functions influencing a firm’s external environment:

Supplier function. Government decisions regarding creation and accessibility of private businesses to government-owned natural resources and national stockpiles of agricultural products will profoundly affect the viability of some

firm’s strategies.

Customer function. Government demand for products and services can create, sustain, enhance, or eliminate many market opportunities.

Competitor function. The government can operate as an almost unbeatable competitor in the marketplace; therefore, knowledge of government strategies

can help a firm to avoid unfavorable confrontation with government as a

competitor.

Technological Forces

Technological forces influence organizations in several ways. A technological innovation can have a sudden and dramatic effect on the environment of a firm. First, technological developments can significantly alter the demand for organizations or industry’s products or services.

In formulating a strategy, the strategic decision makers must analyze conditions internal to the organization as well as conditions in the external environment, which are described in the following sections.

Social Forces

Social forces include traditions, values, societal trends, consumer psychology, and a society’s expectations of business.

The following are some of the key concerns in the social environment: ecology (e.g., global warming, pollution); demographics (e.g., population growth rates, aging work force in industrialized countries, high educational requirements); quality of life (e.g., education, safety, health care, standard of living); and noneconomic activities (e.g., charities).

1. operating environment – that is, competitors, markets, customers, regulatory agencies, and stakeholders; and

2. The internal environment – that is, employees, managers, union, and board directors.

Essential features of organization’s strategy

Every goal set should have all of the following features:

1. Specific: When specifying a goal, there should be no room for uncertainty. For example, ―We want to be industry-leaders,‖ sounds great, but what, specifically does that entail?

2. Measurable: Measurability helps a lot with specificity. Wherever possible, use quantifiable measurements. That doesn‘t entirely exclude qualitative goal-setting, but you will need to define how you will measure qualitative indicators.

3. Achievable: Reaching for the stars sounds great, but do you have what it takes to build a rocket ship? Set challenging goals but don‘t set yourself up for failure.

4. Realistic: Realism and achievability are closely related. That‘s why you need to look at where you are now before you can decide what you plan to achieve. Do you have the necessary capital at your disposal? If you raise funds, what will it take to cover loan repayments? Do you have adequately skilled staff? If not, what will it take to attract new talent or train your existing workforce?

5. Time-bound: Let‘s assume you‘re working on a five-year plan. You will identify several strategic priorities. Realizing these means setting a series of tasks and sub-tasks. And since you‘re looking at a three to five-year plan, each task must be completed by a certain time if you are to reach your target. Naturally, the time you set must also be achievable and realistic

Evolution of strategic Management

Strategic Management Evolution in terms of 4 Paradigm shifts- Ad Hoc policy, Integrated policy formulation, strategy and strategic management paradigm

Hofer and others have viewed the evolution of strategic management in terms of four paradigms shifts, which can also be considered the four overlapping phases in the evolution/development of strategic management. These developments have closely followed the demand of real-life business.

These paradigms are discussed below:

1. Ad Hoc Policy Paradigm:

The first paradigm was the era of ad hoc policy making. This phase can be traced back to 1900-1930. This was also the era of mass production and maximizing output. Normally, the firms commenced operations in a single product line, standardized the product and lowered the cost of production, catering to unique set of customers in a limited geographical area expanded in one or all of the three dimensions of business.

Informal control and co-ordination became partially irrelevant as expansion took place and the need to integrate functional areas arose. This integration was brought about by framing policies to guide managerial actions.

Coordination was the main concern of the management and there was hardly any element of the strategic management although the strategic planning focused on maximizing output.

2. Integrated Policy Formulation Paradigm:

The second paradigm was the era of integrated policy formulation. In the 1930- 1940 there were many environmental changes that took place in the US. These changes were in technology, turbulence in political environment, emergence of new industries, and demand for novelty products even at higher costs, product differentiation, and market segmentation in increasingly competitive and

changing markets.

All these made investment decisions increasingly difficult. The planned policy formulation replaced the ad hock policy making. This was the era of integrating all functional areas and framing integrated policies to guide managerial

actions. That is why it is called integrated policy formulation era.

3. Strategy Paradigm:

The third paradigm was the era of strategy. In the period of 1940-1960, planned policy became irrelevant due to increasingly complex and accelerating changes taking place in the environment and the needs of the business could no longer be served by policy making and functional area integration only. Firms had to anticipate environmental changes. By the 1960s, there was a demand for a critical look at the basic concepts of business and its relationship to the environment. The concept satisfied this requirement and the third paradigm based on strategy emerged in the early sixties.

4. Strategic Management Paradigm:

The fourth paradigm was the strategic management which emerged in 1980 and onwards. The initial focus of strategic management was on the interactions of two broad fields of enquiry- the strategic process of business firm and the responsibility of general management.

What to produce, where to market, which new business to enter, which one to quit and how to get internally stronger and resourceful are the new stakes.

Strategic planning is required to be done to endow the enterprise with certain fundamental competence/distinctive strengths which could take care of eventualities resulting from unexpected environmental changes.

However, the evolution of this fourth phase is still continuing and is yet not formed into a theory of how to manage an enterprise. But strategic management is a very important tool for and way of thinking to resolve strategic issues. The world is substantially compressed and managing the external and internal environment becomes a crucial function.

Strategic issues

What is a Strategic Issue?

A Strategic Issue is, first of all, an issue – an unresolved question needing a decision or waiting for some clarifying future event. Secondly, it is strategic and has major impact on the course and direction of the business. It probably relates directly to one or more of the fundamental ―Three Strategic Questions‖:

What are we going to sell?

To whom are we going to sell it?

How will we beat or avoid our competition?

There are two types of strategic issues; external and internal.

External strategic issues arise due to factors beyond your control.

Internal strategic issues are ones which your organization faces because of internal factors. That‘s an internal strategic issue. Simply put, internal strategic issues are the ―big problems‖ your organization faces that you have direct influence and impact over.

Identifying strategic issues is only the first step. Now, the planning team needs to decide how to analyze and collect the information needed to make informed

strategic decisions.

There‘s no right or wrong answer when it comes to how much analysis and data the team needs. A good rule of thumb to follow is to collect just enough to feel confident in making strategic decisions.

With strategic issues identified and data collected, next is to begin the analysis.

A great non-linear way to closely analyze strategic issues is to perform a SWOT

analysis on each. It gives the team the opportunity to really dive in and analyze it.

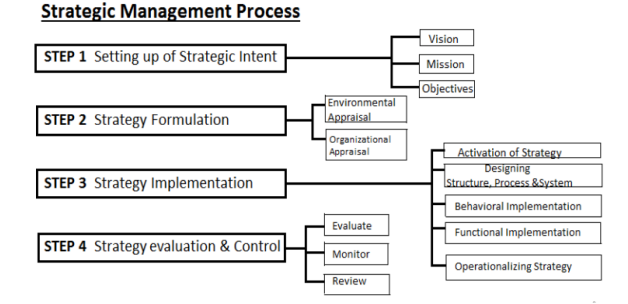

Strategic management process

Step 1: Setting up strategic Intent

• Vision- Vision is the statement that expresses organization‘s ultimate long-run objectives. It is what the firm ultimately like to become. Vision once formulated is for forever and long lasting for years to come. Vision is closely related with strategic intent and is a forward thinking process. Eg- Microsoft- ‘A computer software on every desk and in every home‘.

• Mission- It tells who we are and what we do as well as what we‘d like to become. Mission of a business is the fundamental, unique purpose that sets it apart from other firms of its kind and identifies the scope of its operations in product and market terms. Eg Microsoft- ‗Empower every person and every organization on the planet to achieve more‘.

• Objectives- These are the end results of planned activity that state what is to be accomplished by when and should be quantified if possible and their achievement should result in the fulfillment of a corporation‘s mission. Objectives state specifically how the goals shall be achieved. Following are the areas for setting objectives profit objective, marketing objective, production objective, etc.

2. Strategy Formulation

Strategy formulation refers to the process of choosing the most appropriate course of action for the realization of organizational goals and objectives and thereby achieving the organizational vision. For choosing most appropriate course of action, appraisal of organization and environmental is done with the help of SWOT analysis.

• Environmental Appraisal- The environment of any organization is “the aggregate of all conditions, events and influences that surround and affect it”. It is dynamic and consists of External & Internal Environment. The external environment includes all the factors outside the organization which provide opportunities or pose threats to the organization. The internal environment refers to all the factors within an organization which impart strengths or cause weaknesses of a strategic nature.

• Organizational Appraisal- It is the process of observing an organizational

internal environment to identify the strengths and weaknesses that may influence the organization’s ability to achieve goals. The analysis of organizational capabilities and weaknesses becomes a pre-requisite for successful formulation and reformulation of organizational strategies. This analysis can be done at various levels: functional, divisional and organizational .

3. Strategy Implementation

Strategy implementation is the action stage of strategic management. It refers to decisions that are made to install new strategy or reinforce existing strategy.

• Designing structure, process & system- Strategy implementation includes the making of decisions with regard to organizational structure, developing budgets, programs and procedures in order to accomplish certain activities.

• Functional Implementation- Functional implementation is carried out through

functional plan and policies in five different areas- marketing, finance, and

operation, personnel and Information management.

• Behavioral Implementation- It denotes mobilizing employees and managers to put and formulate strategies into action and require personal discipline, commitment and sacrifice. It depends upon manager‘s ability to motivate

employees.

• Operationalizing strategy- It includes establishing annual objectives, devising policies, and allocating resources.

Strategy Evaluation & Control

• Strategy evaluation- It is the primary means to know when and why particular strategies are not working well. It is the process in which organizational activities and performance results are monitored so that actual performance can be compared with desired performance. Thus strategic evaluation activities include reviewing external and internal factors that are the basis for current strategies.

• Strategic control- In this step, organizations Determine what to control i.e., which objectives the organization hopes to accomplish, set control standards, measure performance, Compare the actual with the standard, determine the reasons for the deviations and finally taking corrective actions and review the policies and activities if needed.