MONDAY: 5 December 2022. Morning Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Do NOT write anything on this paper.

QUESTION ONE

1. Identify the accounting principles applied in each of the following statements:

(i) John Mrefu withdrew Sh.200,000 from the business bank account for his personal use. (1 mark)

(ii) Rita Neno is confident that her business will be in existence in year 2035. (1 mark)

(iii) The accountant of one Traders did not pay the electricity bill last month, but has accounted for it. (1 mark)

2. Distinguish between the various needs and interests of the following users of accounting information:

(i) “Investors” and “lenders’. (4 marks)

(ii) “Employees” and “government”. (4 marks)

3.The following information is provided by the petty cashier of Dawa Traders for the month of November 2022:

November 1 Received Sh.206,400 from the chief accountant

November 2 Purchased newspapers and printing papers for Sh.4,800.

November 3 Paid for data bundles worth Sh.1,600.

November 7 Paid a supplier, Purity, Sh.12,800.

November 10 Paid an amount of Sh.21,600 for fuel.

November 11 Purchased stationery for Sh.24,000.

November 12 Purchased mops and cleaning detergents for Sh.5,440.

November 15 Paid for motor vehicle repairs for Sh.25,600.

November 22 Paid for fuel of Sh.16,000

November 28 Paid for cleaning services of Sh.6,400.

The petty cashier had Sh.33,600 on 1 November 2022.

Required:

Prepare a petty cash book with the following headings:

- Internet and stationery.

- Transport.

- Cleaning.

- Ledgers.

(9 marks)

(Total: 20 marks)

QUESTION TWO

- Citing relevant examples, explain the difference between “real accounts” and “nominal accounts”. (4 marks)

- Discuss FOUR limitations of the historical cost accounting method. (8 marks)

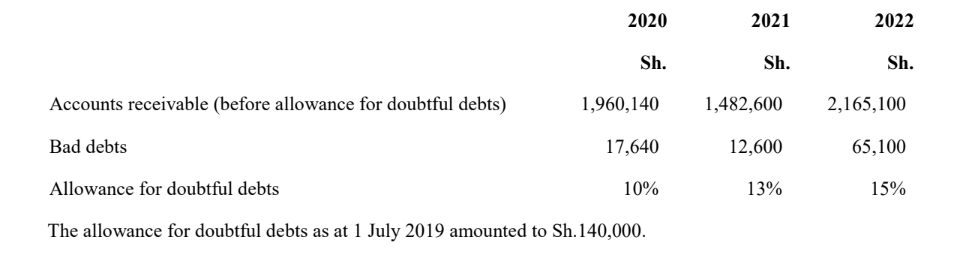

- Chakula Traders is a wholesale distributor of foodstuff. They offer credit terms to their customers. Allowance is

made for doubtful debts based on the outstanding accounts receivable and general economic conditions.

The following data was collected from the books of account of Chakula Traders for the year ended 30 June:

Required:

- Allowance for doubtful debts account for each of the three years. (4 marks)

- Extract of the statement of profit or loss for the years ended 30 June 2020, 2021 and 2022. (2 marks)

- Extract of the statement of financial position as at 30 June 2020, 2021 and 2022. (2 marks)

(Total: 20 marks)

QUESTION THREE

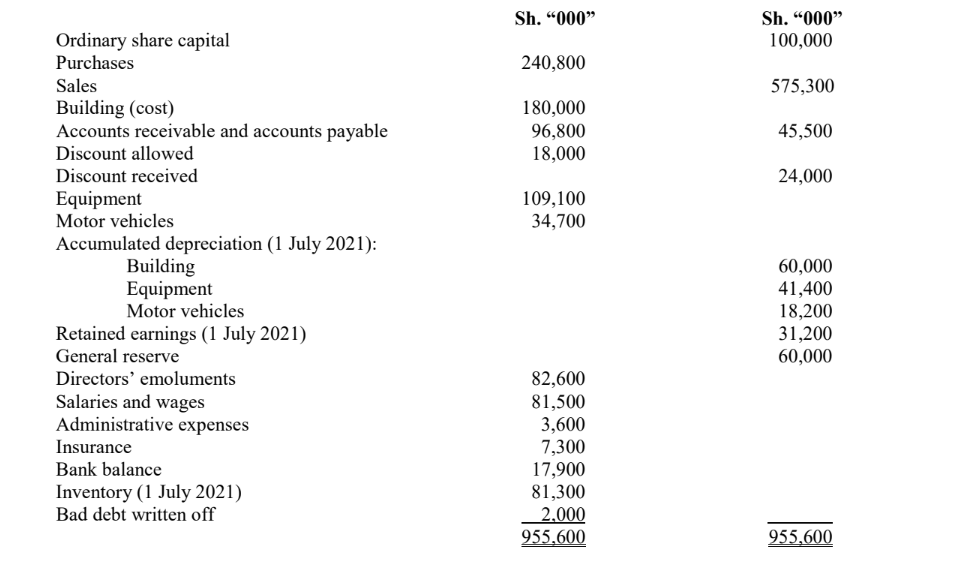

The following balances were extracted from the books of Pillar Limited as at 30 June 2022:

Additional information:

1. Inventory as at 30 June 2022 was valued at Sh.24,000,000.

2. As at 30 June 2022, accrued insurance expenses amounted to Sh1,700,000 while outstanding salaries and wages

amounted to Sh.4,500,000.

3. Depreciation is to be provided per annum as follows:

Building 2.5% on reducing balance

Equipment 10% on straight line basis

Motor vehicles 20% on reducing balance

4. Provide for audit fees and corporate tax for the year ended 30 June 2022 at Sh.6,000,000 and Sh.35,500,000

respectively.

5. Directors proposed:

Transfer of Sh.7,500,000 to the general reserve.

Dividend of 10% for ordinary shares.

Required:

- Statement of profit or loss for the year ended 30 June 2022. (12 marks)

- Statement of financial position as at 30 June 2022. (8 marks)

(Total: 20 marks)

QUESTION FOUR

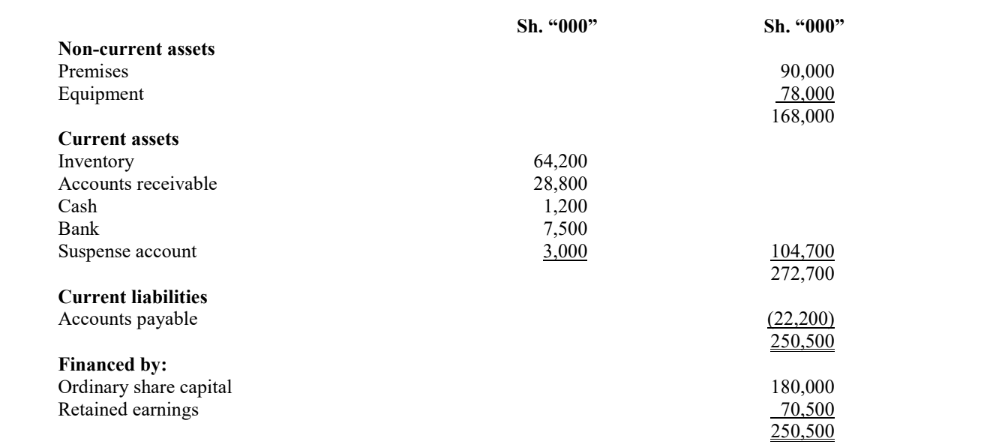

The trial balance of One Zero Ltd. did not balance and thus the difference was posted to a suspense account.

The following is One Zero’s statement of financial position as at 30 September 2022:

Additional information:

Thorough investigation of the books of account revealed the following errors:

1. Purchase day book entries for July 2022 had been undercast by Sh.1,200,000.

2. A receipt of Sh.2,400,000 from a debtor had been credited to sales.

3. An accrual of Sh.318,750 for insurance charges had been omitted from the books.

4. A bad debt of Sh.207,000 had not been written off from the books of account.

5. The sales account had been under cast by Sh.360,000.

6. The bank debit column in the cashbook for August 2022 was undercast by Sh.2,160,000.

7. On 30 September 2022 cheques of Sh.1,890,000 were received from customers and the transactions were not recorded in the books of account until 7 October 2022.

8. Discount allowed of Sh.1,020,000 had not been recorded in the books of account.

9. No entry had been made for a refund of Sh.2,190,000 paid by cheque to a customer who had returned some goods.

10. Payment to a supplier Sharon Lilo of Sh.2,300,000 had been erroneously entered in another suppliers account named

Sharon Jana.

Required:

- Journal entries to correct the above errors. (10 marks)

(Narrations not required) - Suspense account duly balanced. (2 marks)

- Corrected statement of profit or loss for the year ended 30 September 2022. (4 marks)

- Adjusted statement of financial position as at 30 September 2022. (4 marks)

(Total: 20 marks)

QUESTION FIVE

1. Distinguish between the following terms:

(i) “General ledger” and “subsidiary book”. (4 marks)

(ii) “Ordinary shares” and “preference shares”. (4 marks)

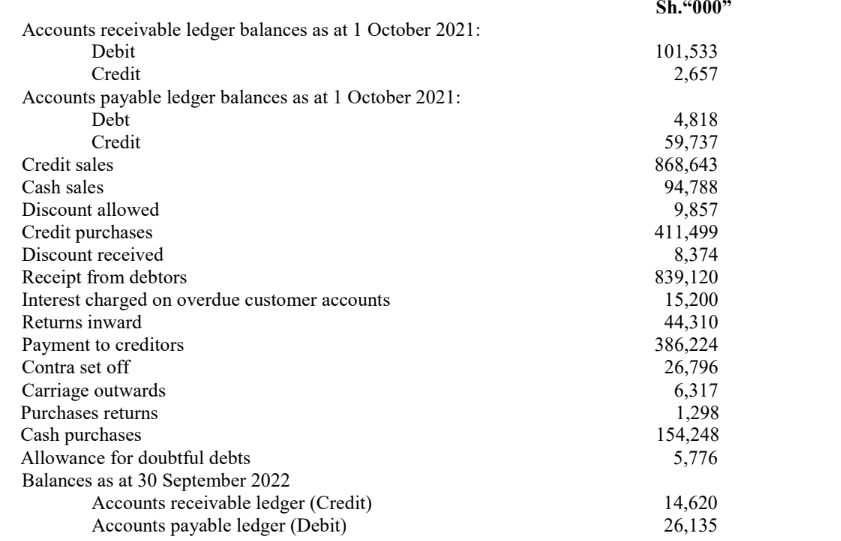

2. The following balances were extracted from the books of Kwale Wholesalers as at 30 September 2022:

Additional information:

1. A cheque for Sh.1,325,000 from Kiu Limited, a credit customer, has been returned by bank marked “refer to drawer”.

2. Bad debts of Sh.4,615,000 are to be written off and the allowance for doubtful debts is to be raised to 10% of the debts balances at 30 September 2022.

3. On 30 September 2022, a cheque for Sh.928,000 was received from the liquidator of Mirare Traders. This customer owed Kwale wholesalers Sh.6,800,000 when it ceased to trade in May 2020, at the height of Covid-19 pandemic. The debt had been written off as a bad debt in the year ended 30 September 2021. No entry in respect of this amount received has yet been made in the books.

Required:

- Accounts receivable control account for the year ended 30 September 2022. (6 marks)

- Accounts payable control account for the years ended 30 September 2022. (6 marks)

(Total: 20 marks)