Economics essentially studies the way in which mankind provides for the material well being. It’s thus concerned with the way people apply their knowledge, skills and effort to the gift of nature in order to satisfy human their material wants. Economics is a social

science which studies the allocation of scarce resources which have alternative uses among competing and usually limitless wants of the consumers in the society.

Basic Economic Concepts

- Human wants This refers to people desires for goods and services and circumstances that enhance their material well being.

- Economic Resources These are ingredients that are available for providing goods and services in order to certify the human wants. A resource must be scarce and have money value. Resources can be categorized as natural, or man made.

- Natural Resources refer to anything given by God or nature such as fertile soil, rivers, lakes, mountains etc.

- Man Made Resources refers to anything created by man to assist in further production such as tools, equipments, roads and buildings etc.

N/B Economics resources also refer to as factors of production which includes land, labour, capital and entrepreneurship. - Scarce and Choice if the resources available are not enough to produce goods and services to satisfy all the wants then they are said to be scarce. As a result, individuals and society cannot have all the things that they want. Since resources are limited, choices have to be made. The choice to satisfy one want implies others are forgone. Individuals have to make choices e.g. consumers with their limited income and unlimited wants have to choose how they spent their income.

- Opportunity Cost refers to the value of benefit expected from the best second alternative forgone. It is based on the fact that resources being scarce have competing alternative uses. The choice to satisfy one alternative means that another is forgone. The value of the second best forgone alternative is the opportunity cost.

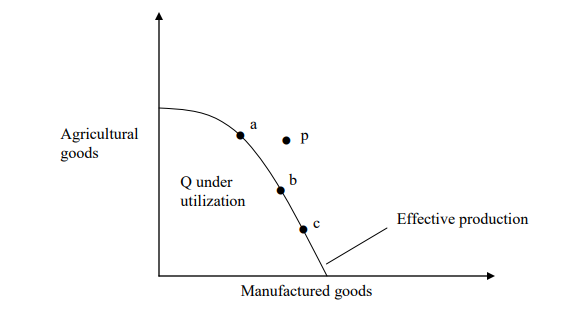

Production Possibility Frontier/Capacity (PPF/PPC)

It provides a graphical illustration of the problem of scarcity and choice which is the basic economic problem. The curve shows what a country produces with existing supply of land, capital and entrepreneurship ability. With limited supply of economics resources

a country has a wide variety of options and variety of goods and services it can produce. Assume a simple hypothetical economy where a country produces two types of goods i.e. agriculture and manufactured goods. The two extreme possibilities are:

- The country commits all its resources to the production of agriculture and non to manufacturing.

- All the resources are put to manufacture and non to agriculture.

These two extreme cases are unlikely and the country will most likely choose to produce goods of both commodities. The opportunity cost of producing either of them is increasing which the law of diminishing return.

The PPF is a locus of all combination point which represents goods and services that a country can produce if all resources are utilized fully and efficiently. Points on the curve such as A, B and C show maximum possible combined output of the two commodities.

The economy can produce any combination inside the curve such as point Q where it means some resources are unemployed. The resources in such a case will produce more commodities by moving either to point B or point A. The points outside the curve are not

attainable with the country’s present productive capacity. The country can only achieve this if its productive capacity has been increased and this will cause the curve to shift to the right as shown by the dotted curve. A country’s productive capacity can increase if there is advancement in technology or if there is a discovery of new resources. The PPF/C is concave to the original indicating the concept of increasing opportunity costs.

1.2 Scope of Economics

The main branches of economics are:

Microeconomics which is the study of the smallest economic decisions making units of the society. Microeconomics theory is a branch of economics that studies the behavior of individual decision making units such as consumers, resource owners and business firm

as well as individual markets in a free market economy. The aim of microeconomics is to explain the determination of prices and quantities of individual goods and services. Microeconomics also considers the impact of government regulation and taxation of

individual markets. For example, microeconomics analyses the forces that determine the prices and quantities of television sets sold. Microeconomics can be considered as the ultimate cellular structure of economics.

It is the study of individuals, households and firms. The major areas are

- demand and supply analysis

- market equilibrium

- consumer theory

- theory of the firm

- market structure

- distribution theory

Macroeconomics is the study of bigger and complex systems. Macroeconomic theory is the study of the behaviour of the economy as a whole whereby the relationship is considered between broad economic aggregates such as national income, employment and prices. The economy is disaggregated into broadly homogenous categories and determinants of the behavior of these aggregates are integrated to provide a model to the entire economy.

Macroeconomics focuses on the economic stabilization whereby government policy is used to moderate business cycles and encourages real economic growth. Macroeconomics became a separate topic of discussion in the aftermath of John Maynard Keynes and the great depression. The line between microeconomics and macroeconomics is, however, blurred and there are many areas of overlap between the two. Key areas of macroeconomics are:

- national income

- economic growth and development

- money and banking

- public finance

- unemployment

- inflation

- international trade

1.3 Why Study Economics?

It is useful to study economics for the following reasons\

- Economics provides the underlying principles of optimal resource allocation and thus enables individuals and firms to make economically rational decisions. Thus for example the preparation of budgets involves knowledge of demand and elasticity analysis. The making of price policy decisions draws heavily on the concept of elasticity in economics. Additionally, the theory of

production in economics is concerned with the principles that facilitate the optical combination factors of production. - A study of economics enables individuals and organizations to appreciate the constraints imposed by the economic environment within which any entity operates. Thus an individual or firm is more fully enabled to appreciate the implications of the annual budget considering how for example the increased liberation of the economy will affect a particular business entity and the

economy in general. Additionally, the student of economics is able to appreciate the effects of such economic variables as inflation, exchange rates, interest rates money supply and so on. - The area of development economics is fundamentally concerned with the reasons why societies develop and means of accelerating development. It is vital for individuals as citizens to appreciate the parameters that determine the development process so that they contribute more fully to facilitate and contribute to solving the economic problems that characterize their society.

- Economics is an analytical subject and its study can help develop logical reasoning which is never superfluous.

1.4 The Methodology of Economics

A useful insight into the methodology applied in economics can be gained by distinguishing between positive and normative economics. This enables one to appreciate the limitations and scope of economics. Positive economics is concerned with what is, or how the economic problem facing societies are actually solved. Positive statements therefore, only deal with facts for example; “Kenya is a member of the East African community” and “Uganda is currently Kenya’s major trading partner” are positive statements. For example a dispute over whether Uganda is currently Kenya’s major trading partner can be settled by looking at the statistics of Kenya’s trade with its partners. Normative economics refers to the part of economics that deals with the value of judgments. This implies that normative deals with what ought to be, or how the economic problems facing the society should be solved. Normative statements usually reflect people’s moral attitudes and are expressions of what particular individuals group thinks ought to be done. A statement such as “Uganda to should join the Southern Africa Development Community” or “upper income classes ought to be taxed heavily”, are normative statements.

Economics makes use of the scientific methods to develop theories. Scientific inquiry is generally confined to positive questions. One of the major objectives of sciences is to develop theories. A theory is a general or unifying principle that describes and explains

the relationship between things observed in the world around us. The purpose of a theory is to predict and explain. The search for a theory begins whenever a regular pattern is observed in the relationship between two or more variables and one asks why this should is so. A theory refers to a hypothesis that has been successfully tested. It is important to note that economics hypothesis is not tested by realism of its assumptions but its ability to predict accurately and explain.

The following procedures are adopted in the scientific method:

- The concepts are defined in such a way that they can be measured in order to be able to test the theory against the facts.

Whereas these facts may seem superfluous, in practice it is quite difficult to define many concepts in economics in a way that is agreeable to all schools of thought. It is often correctly postulated that when you want to argue, first define your terms. - A hypothesis formulated A hypothesis refers to tentative untested statement, which attempts to explain how one thing is related to another. Hypotheses are based on observation and upon certain assumptions about how the real world works. The assumptions may themselves be based upon prevailing theories that have proved to have a high degree of reliability. In a social science, the basic assumptions or paradigms about reality are vital. A discipline’s basic assumptions about reality determine what it focuses on. In economics for example, many theories are based on the rationality assumption. The formulation hypothesis is thus arrived at through a process of logical reasoning using observed facts and certain assumptions. As mentioned earlier, a hypothesis is not tested by the realism of its assumptions but its ability to predict accurately. Economic hypothesis must be framed in a manner that enables scientists to test their validity.

- The hypothesis is then used to make predictions.

If the hypothesis is correct, then if certain things are done, certain others will happen. For example hypothesis may predict the rise in the price of a given commodity may lead in the fall of the quantity demanded of that commodity. - The hypothesis is tested by considering whether its predictions are supported by facts.

In order to test a hypothesis and arrive at a theory, one must go to the real world and see whether the hypothesis is indeed true for various situations. The social scientists however cannot carry out controlled experiments in the laboratory. The laboratory of the social scientist in the human society and human beings cannot be put into a controlled situation to see what happens. Observed economic data is subjected to statistical analyses whose techniques help the economist to determine the probability that particular events have certain causes. If a hypothesis is supported by factual evidence we have a successful theory, note that a theory can never be true in all circumstances and new theories are developed as old ones are discarded because their predictions have become unreliable.

1.5 Economic Systems

These refer to the way in which different societies solve the three different basic economic problems which are:

- Which goods should be produced and in what quantities?

- How should various goods and services be produced?

- How should various goods and services be distributed?

These in turn determine various political and economic structures in the society. The economic systems are as follows:

1. Free market economy Also referred to as capital system or laiser faire economy. It refers to a system where decisions about allocation of resources are made by individuals on the basis of prices generated by forces of market prices of demand

and supply. A free market economy has the following features

- Private property individuals have the right to own or dispose off their property as they may consider it fit.

- Freedom of choice and enterprise Individuals have the right to buy or hire economic resources, organize them for production purpose and sell them in the market of their choice. Such persons are referred to as entrepreneurs.

- Self interest the pursuant of personal goals. The individuals are free to do as they wish and have the motive of economic activity in self interest.

- Competition There is a large number of buyers and sellers such that each buyer and seller accounts for but is insignificant to influence the supply and demand and hence prices.

- Reliance on price mechanism This is an elaborate system of commerce in which numerous choices of consumers and producers are aggregated and balanced against each other. The interaction of demand and supply determine prices.

- No government intervention Hence no price controls, taxes and subsidies.

- There are property rights provided and enhanced by the government through copy rights patents, trademarks etc.

Advantages of free market economy

- There is the matching of demand and supply. Production takes place in response to demand hence a balance between what is produced and consumed. No wastage.

- There is flexibility of the market in responding to changes in demand and supply conditions.

- There are no resources wasted in planning as no planning is required

- Consumer sovereignty and competition gives rise to a wide variety of goods and services giving consumers a wide range to choice from.

- Higher rates of economic growth due to the incentive available for hard work which is motivated by profits.

- No wastage of resources on unrealistic projects because investment decision are based on profits.

Disadvantages

- Income inequality the ability of some people and firms to acquire excessive market power leads to greater inequality in income and wealth.

- Monopoly power refers to the ability of a firm to control its prices

- Externalities spill over refers to social costs and benefits not taken into consideration when determining price levels.

- Public goods. The price mechanism on its own cannot allocate resources to the production of public goods such as roads, schools, security etc., which have no rivals and no excludability.

- Instability and unemployment due to the trade cycles of recession, depression, recovery and boom.

- The inability to deal with structural changes caused by wars, natural calamities among others.

- Inadequate provision of merit goods. Merit goods are goods of importance to the community such as health, education, security among others

2. Planned economy Also referred to as command economy or government controlled economy, socialism or communism. It refers to an economic system where the crucial decisions are determined a body appointed by the state. The body takes up the role of mechanism which prevails in a free market economy

Features of a command economy

- Leadership and control of economies. All important means of production (resources) are publicly owned such as land, power generation, housing among others.

- Rationing of certain commodities if supply of such fall bellow demand.

- Existence of production targets for different sectors of the economy. The government determines how resources are allocated through planning.

- Fixing of prices and wages

- Occasional existence of restricted labour market in which workers take up jobs assigned to them.

- Government decides what is to be produced

Advantage of planned economy

- Avoids economic instability

- Minimize negative externalities

- Makes adequate provision of public and merit goods

- Facilitate the shift of resources in pursuant of grand schemes such rapid industrialization

- Puts checks on monopoly power which are controlled by state monopolies (Parastatals).

Disadvantages of Planned economy

- There is wastage of resources in production because consumers demand is judged in advance without the use of price mechanism.

- The cost of gathering information for planning is expensive to the state.

- In absence of profit motive in production there is no incentives for hard work and innovation.

- The power of consumer sovereignty is curtailed

3. Mixed economy refers to an economic system where resource allocation is determined by the state and price mechanism. This form of economic system can exist in two ways:

- Where the means of production are privately owned but the government through fiscal and monetary policies regulate the working of price mechanism towards desired levels.

- The government does not only regulate the working of the price mechanism but also strategic resource thus taking part in production.

Fiscal policy refers to the policies which the government uses to stabilize the economy through government revenue and expenditure.

Monetary policy refers to the policies implemented by the central bank to stabilize the economy by use of money supply and interest rates. Both policies make up the budgetary policy of the government.

1.6 Why Intervene in the Economy

- To create a framework of regulations and rules to ensure fair competition thus promote competition between firms both small and big.

- Redistribute income through a system of taxation

- Prevent market failure of price mechanism

- Stabilize the economy

- Maintain competition by controlling monopoly

Partial Equilibrium refers to the study of the behaviour of individual decisions making units and the functioning of individual markets in isolation. General Equilibrium is the analysis of the behaviour of all individuals‟ decision making units on all individual markets simultaneously.

1.7 Specialization

This refers to the process where people concentrate on those activities where they are best at. It takes a form of division of labour which is dividing up of economic tasks of production into tasks which people specialize into. Division of labour therefore leads to

specialization which leads to increase in output.

Advantages of specialization

- It help individual development by exploring their talent

- It is possible to use machines to do specific/ particular task

- Increase in skills result in increased expertise and performance

- Time saving as a worker will accomplish more by doing a particular task.

Disadvantages

- Leads to loss of craftsmanship. Extensive specialization leads to increased use of machines which are more automated leading to loss of basic skills

- Production of standardized goods limiting the range of goods consumers can choice from. It does not cater for different tastes and preferences.

- Monotony and boredom due to repetitions of the same work. This leads increased accidents, absenteeism which are associated with lack of motivation.

- Increased inter-dependence as a specialized system of production increases the extent to which different sectors of the economy rely on each other. If mistakes are made in one production unit it may cause the fall of all or other organization which depend on items from that production unit.

- Increase in risk of unemployment if one’s skills are no longer required in the market they may get an alternative employment.