To survive or prosper in the global business environment, a firm must be skilful in how it applies its strategies to compete globally. Although global competitive strategies are imperative for firms operating in multiple countries, the solely domestic firm must keep a

global perspective to be prepared for foreign competitors entering its market in various forms (e.g. exports, franchising, FDI etc.). A global competitive strategy is the strategy a firm uses as it seeks to create or maintain an advantage over its global or international competitors. The strategies may be divided into those for creating competitive and those for avoiding competitive disadvantage.

Creating Competitive Advantage

The following are the major strategies for creating competitive advantage in the global market place.

1. Worldwide integration strategy

The firm‘s activities are integrated worldwide and it offers similar product to all its customers around the globe. Such a firm will enjoy economies of scale arising from various sources, and hence its product unit cost will be low. In such a strategy, the firm designates certain countries as the places where certain activities are performed, e.g production could be done in South Africa, financing in Europe, taxation in the Middle East, and the manufacture of parts in China, Korea, and Mexico. Activities are usually designated to be performed in countries where such activities can be performed cheaply. An example of this strategy was the attempt by Ford to make the Ford Escort a ―world car‖. Configuring its processes, resources and strengths in pursuit of advantages enabled Ford to produce the Ford Escort at a lower cost than cars produced by competitors.

National responsiveness strategy

Unlike the worldwide integration, this strategy allows subsidiaries much more autonomy to respond to local market conditions prevailing in a country. The ability to quickly respond to different preferences and regulatory changes across countries gives the nationally responsive firm an advantage over the firm pursuing a worldwide integration strategy. While the integrated firm cannot quickly alter its operations in one country without threatening the operations of other subsidiaries, the responsive firm can.

Administration coordination strategy

Refers to a strategy which combines both worldwide integration and national responsiveness. Since most industries are not entirely global or entirely multi-domestic, it is often necessary that firms develop the ability to both integrate globally and be locally responsive. The strategy, however, is quite difficult to implement because local responsiveness and worldwide integration are trade-offs between flexibility across countries and flexibility within countries, while the firm concentrates on internal efficiency. While trying to rationalize between the two trade-offs, internal efficiency often suffers. The strategy requires skill and a flexible organizational structure to respond adequately both to pressures for integration and responsiveness.

Collaboration strategy

In today‘s global business, firms often cooperate rather than compete to enhance their competitiveness. Collaboration may take the various forms e.g. strategic alliances, joint ventures etc.

Broad-line competitive strategy

Here a firm competes on a worldwide basis and offers a wide range of products in a given industry.

Global focus strategy

In this strategy, a firm competes worldwide, but only in a part of the industry.

National focus strategy

This strategy involves focusing on one or few particular national markets and trying to outperform global firms by concentrating on keeping costs low or differentiating products within those few markets.

Protected niche or shelter strategy

It is a strategy where governmental protection is sought from competition in certain countries in order to gain competitive advantage.

The strategy, however, does more to isolate a firm from competition than giving it a competitive advantage. Firms from smaller countries and developing countries often find this strategy particularly advantageous.

Avoiding Competitive Disadvantages

Firms often resort to the following strategies to avoid being placed at a competitive disadvantage in the global or international marketplace.

1. Oligopolistic reaction

Refers to the tendency of firms in oligopolistic industries to follow the moves of a major competitor in the industry.

2. Presence in competitor’s home markets

The simple presence of a firm in a competitor‘s home market, even on a relatively small scale, can pose a sufficient threat to a competitor that prevents the competitor from attacking the firm‘s primary markets.

Presence in key global markets

A firm cannot truly compete on a global scale if it is not present in the key global markets such as the Americas, Japanese, and Western European markets. These three markets account for about half of the world‘s total consumption, and share certain important economic and demographic conditions. If a firm does not have operations in all three areas of the triad, it may not be able to achieve maximum economies of trade.

MANAGING GLOBAL FUNCTIONS

By their nature, MNEs/MNCs are headquartered in one country but have operations in other countries. In carrying out business efficiently and effectively, MNEs/MNCs come up with appropriate strategies to manage the various functions efficiently and effectively in a global scale. The functions include but not limited to Marketing, HRM, Finance, and R&D,

Innovation and Production.

Marketing

Should be designed to help identify opportunities and take advantage of them.

Involves consideration of:

- The product or service to be sold,

- The way in which the output will be promoted,

- The pricing of the good or service, and

- The distribution strategy to be used in getting the output to the customer.

There is therefore need for MNEs/MNCs to consider fundamental of international marketing strategy. Marketing strategy begins with an international market assessment, the evaluation of the goods and services the MNE can sell in the global market place. Product strategies will vary depending on the specific good and the customer; some products need little or no modification, and others require extensive changes. There are a number of ways in which MNEs promote their products, although the final decision is often influenced by the nature of the product. Pricing in international markets is influenced by a number of factors including government controls, market diversity, currency fluctuations, and price escalation forces. Distribution strategies differ on a country-by-country basis, and MNEs ought to spend a considerable amount of time in examining the different systems in place, the criteria to use in choosing distributors and channels, and how distribution segmentation can be accomplished

Human Resource Management

International HRM entails the process of selecting, training, developing, and compensating personnel in overseas positions. HRM strategies involve consideration of staffing, selecting, training, compensating, and labour relations in the international environment.

Attention should be paid to language training, cultural adaptation, and competitive compensation among other things.

Finance

International financial management by MNEs should consider a number of critical areas:

- The management of global cash flows,

- Foreign exchange risk management,

- Capital expenditure analysis, and

- International financing.

R&D and innovation

R&D and innovation form the basis for new product development and modifications, business process reengineering, and knowledge creation. Therefore, central to R&D and innovations decisions is the product life cycle theory. The way MNEs manage these operations is determined by the extent of globalization and/or localization adopted by a specific MNE. Most MNEs manage their R&D and Innovations as projects, hence will involve substantial investments. R&D could be decentralized or centralized depending prevailing market conditions. MNEs need to continually research, develop, and bring new offerings to the market place due to proliferation of cheaper substitutes. In production of goods and services, MNEs ought to look at cost, quality, and well-designed production systems. To ensure efficiency in production, MNEs should manage their international logistics effectively. To improve production, MNEs pay critical attention to:

- Technology and design,

- Continuous improvement of operations, and

- The use of strategic alliances and acquisitions.

These are bound to help MNEs meet new product and service challenges while keeping costs down and quality up. Thus strategic decisions are a dynamic and complex process because of the impact of several factors. However, executives can reduce this complexity by putting a few questions while going for strategy.

- Does the strategy fit management’s values, philosophy, know-how, personality, and sense of social responsibility?

- Is the strategy consistent with the internal strengths, objectives and policies of the organisation?

- Does the strategy not conflict with other strategies of the organisation?

- Is the strategy likely to produce a minimum of new administrative problems for the organisation?

- Does the organisation have sufficient resources to implement the strategy?

- Does the strategy balance the acceptable minimum risk with maximum profit potential consistent with organization‘s resources and prospects?

- Does the strategy require too much or too large of organization‘s resources?

Environment has become so complex; predicting the future with accuracy is difficult. The number of variables to be considered in the decision making process are increasing. Production and related technologies become obsolete within a short span of time. The

number of events-both domestic and world-affecting the organization has increased. With all this happening over-reliance on experience prove to be costly. More reliance has to be placed on creativity, innovation and new ways of looking at the organization in the world in which we exist. A rapidly changing environment requires that managers to make a clear distinction between long range planning and strategic planning which is a component of strategic management. Strategic management sets the major directions for

the organization i.e., mission, major products/ services to be offered arid major market segments to be served. Without the major directions being set before, establishing objectives does not carry much sense. The Strategic management is the major tool for

planning and implementing major changes an organization must make. Many organizations tend to spend substantial amount of time and effort in developing the strategic plan, without devoting sufficient attention to the means and circumstances under which the strategic’ plan to be implemented. It has often been seen that changes come through the implementation thus the need for proper corporate culture, organization structure, rewards and recognition, and appropriate policies regarding performance appraisal need to be stressed.

STRATEGIC OBJECTIVES

Setting strategic objectives needs to be more of a top-down than a bottom-up process in order to:

- Provide guidance to lower level managers and units.

- Support Companywide interests.

- Be cascaded downwards

A strategic objective is an objective of medium and long term nature that aims either at exploiting an opportunity or strength, or deals with a threat or weakness facing the organization. Strategic objectives therefore are based on factors identified in environmental analysis. They take advantage of favourable factors and deal with unfavourable factors identified in external and internal analyses. For example, due to advancement in communication technology (opportunity), Kenya Airways may set for itself the following objective: In three years, at least 90% of Kenya Airways customers should be able to make bookings and reservations on-line. This objective

would be realistic if the airline is strong financially to be able to install the required information technology system (strength). The objective would be necessary if information technology was an area of weakness in the company (weakness). To respond

to the threat of competition (threat), Kenya Airways could set the following objectives:

- In three years, at least 70% of Kenya Airways employees should be professionally qualified in their jobs.

- In three years the airline should achieve at least 95% customer satisfaction.

These two objectives would be realistic if the airline is strong financially to be able to train its employees, as well as, improve on the airline‘s services (strength). Training employees would be necessary if lack of qualifications was one of the weaknesses of the

airline (weakness). As is evident from these examples, strategic objectives like strategies help align the firm‘s strengths and weaknesses to the environmental opportunities and threats.

STRATEGIC AND OPERATIONAL OBJECTIVES

Strategic objectives are different from operational objectives in a number of significant ways. Strategic objectives are of medium and long term nature, while operational objectives are short term, covering a period of one year or less. Strategic objectives are for the organization or business unit as a whole, while operational objectives provide guidance for specific functional or operational

units only e.g. marketing function. Strategic objectives are concerned with developing the organization‘s future potential, while operational objectives are concerned with current performance i.e. converting potential business into actual results.

Building a stronger long term competitive position benefits shareholders more lastingly than improving short term profitability. Strategic objectives focus mainly on effectiveness of the organization while operational objectives are for implementation of strategies and hence focus mainly on efficiency. Strategic objectives are derived from environmental analysis, while operational objectives are usually derived from strategic objectives

CHARACTERISTICS OF GOOD OBJECTIVES

Measurable

This may require:

- Operationalization of abstract concepts.

- Quantification of the objective.

- Giving time frame to the objective

Acceptable to those responsible for implementation

- If set participatorily

- If challenging i.e. difficult but attainable i.e. neither too difficult nor too easy.

Flexible

If can easily be modified to match changed circumstances or conditions i.e. not too rigid.

Motivating

- If challenging

- If linked to rewards i.e. contribution towards attainment is rewarded.

Consistent with the other objectives

If does not conflict with the other objectives.

In harmony with the vision and mission

If does not contradict vision and mission but leads to the realization of such vision and mission.

Not abstract, but are capable of being developed into strategies and actions. If capable of being operationalized i.e. translated into operational plans and tactics for implementation.

Relates directly to factors discovered in the SWOT analysis.

If aims at one or more of the following:

- Exploit an opportunity in the external environment.

- Exploit strength of the firm.

- Deal with a threat in the external environment.

- Deal with a weakness of the firm.

AREAS FOR STRATEGIC OBJECTIVES

- Strategic objectives usually are set on key aspects of the organization, such as:

- Profitability

e.g. to increase net profits by 30% by the end of three years from now. - Productivity

e.g. to improve the firm‘s rate of return on total assets by 50% in the next 3 years. - Competitive position

e.g. to improve the firm‘s leadership in the industry to at least position three in the next 3 years. - Employee development

e.g. in the next three years, at least 70% of the employees should be professionally qualified in their jobs. - Employee relations

e.g. to reduce employee complaints by 60% in the next 3 years. - Technology

e.g. in the next 3 years at least 70% of the firm‘s functions should be computerized. To double the number of computers in the next 2 years. - Public and social responsibility e.g. to increase the budget for public and social responsibility by 200% in the next 3 years

- Quality e.g. product/service quality E.g. to reduce the percentage of defective products by 50% in the next 3 years. To increase customer satisfaction by 100% in the next 2 years.

- Customer care or service e.g. in the next three years the organization should realize at least 95% customer satisfaction.

- Growth e.g. to increase total assets by 50% in the next 3 years. To increase market share by 30% in the next 3 years.

COMPETETITIVE FORCES AND STRATEGIES

Increasing competition demands more competitiveness from companies and constant and accurate information about competitors and the market place. This requires the development of performance evaluation methods. In accordance to RBV (Resource

Based View) approach, the main cause of the variety of firm‘s performance in the market lies in the specific nature of their resources, since this specificity makes them inimitable, un-transferrable and un-substitutable, consequently guaranteeing the obtainment of

differentiated profits. The fundamental basis of long-run success of a firm is the achievement and maintenance of a sustainable competitive advantage (SCA). A competitive advantage (CA) can result either from implementing a value-creating strategy not simultaneously being employed by current or prospective competitors or through superior execution of the same strategy as competitors. A resource-based view emphasizes that a firm utilizes its resources and capabilities to create a competitive advantage that ultimately results in superior value creation. In order to develop a competitive advantage the firm must have resources and capabilities that are superior to those of its competitors. The sustainable competitive advantage requires the long-time preservation of singularity or heterogeneity. This means that the nature of the assets should be analyzed not only through the obtainment factors (ex-ante) but also the factors of maintenance of the firm‘s competitive position over time (ex-post). Attaining and maintaining a sustainable competitive advantage is increasingly dependent on knowledge assets and as result, organizations need to assess and understand how knowledge management (KM) best contributes to organizational performance. When a firm sustains profits that exceed the average for its industry, the firm is said to possess a competitive advantage over its rivals. Porter identified two basic types of competitive advantage: cost advantage and differentiation advantage. Without this superiority, the competitors simply would replicate what the firm was doing and any advantage would quickly disappear. A company must possess some characteristics if it is to have resources and capabilities that are superior to those of its competitors. They are the qualities a company needs to possess if the cost, differentiation and resource factors that Porter identifies are going to manifest and sustain themselves:

- It has a clearly defined and compelling vision, purpose and value proposition that resonates both with its consumer audience and its employee base,

- Its value proposition is supported by a unique product or service that has significant (measurably significant) demand in the marketplace,

- It has a means of creating an experience with a product or service that is distinct and exceptional, and therefore enjoys significant (measurably significant) demand in the marketplace.

- The demand for the product or service (or experience) is anticipated, by all reasonable measures, to be sustainable for the foreseeable future.

- It has an infrastructure that will allow it to continue to deliver on its value proposition to the marketplace better and/or more cost effectively (both for the company and for its customer/client) than its competition.

- It has the ability to attract, retain and properly focus people of exceptional talent to deliver on and sustain the company‘s value proposition.

Assets that are imperfectly immobile and inimitable are sources of sustainable competitive advantage, as they are related to the company and available for its exclusive use over time. In this sense, innovation is an essential factor in the sustention of a competitive

advantage. The product of an innovation is the creation of new assets combinations, of high value, and specifically related to the company. By implementing innovations, companies establish a flow of resources that leads to the creation of stocks of specific assets that other companies will be unable to rapidly replicate.

To sustain competitive advantage, companies must institutionalize their innovation process by creating an environment in which creative thinking is central to their values, assumptions, and actions. The goal of innovation is to develop products that generate above-average returns. These returns allow companies to re-invest in activities designed to give them a competitive advantage in the marketplace. When the innovation cycle is disrupted, companies do not have this incremental capital base and, therefore, have to fund innovation-related activities with capital initially allocated for other purposes. Companies need to focus innovation-related activities around the three principal elements of corporate culture: core values, beliefs, and norms. Strong culture enhances performance in two ways.

- First, it energizes employees by appealing to their higher ideals and values, and by rallying them around a set of meaningful, unified goals.

- Second, it boosts performance by shaping and coordinating employee behaviour.

Businesses thrive because they sell as much of their value as they can to as many customers as possible. “Thriving” means setting realistic goals and meeting (or exceeding) them. Businesses meet their goals because they have a good business model supported

by good strategies (or good strategies supported by a good business model), and businesses that thrive make them work. The way they make them work is to make sure their value always has the right qualities needed for the markets they want. The quest for competitiveness is based on the obtainment of competencies in different focal points of action of the company:

- Allocative competence (related to the production and price formation decisions);

- Transactional competence (competence in the sphere of purchase and sale relations);

- Administrative competence (determination of the policies and of the organizational structure);

- Technical competence (related to the skill of developing and designing new products and processes) and

- Competencies related to the skill of changing existing competencies, through the innovative activity and learning

The coordination of resources is the key ingredient in the construction of competencies and in the definition of the firm‘s performance.

A high level of internal coordination provides the company with enhanced performance indirectly, because it creates the necessary environment for non imitability, non-transferability and non-substitutability of its resources, boosting the potential of its competitive advantages. Sustainable performance results when a firm is able to attain and sustain competitive advantage. The indicators of sustainable performance are developed using a sustainable balanced scored methodology.

The sustainable balanced scorecard encompasses indicators on six perspectives:

- Financial,

- Customer/market

- Internal processes

- Learning and development

- Social

- environmental

Financial

• Sales growth

• Return on sales

• Return on assets

• Return on equity

• Gearing etc

Customer/market

• Market share

• Number of new customers

• Product return rate

• Defects

• Order cycle time etc

Internal processes

• Productivity

• Labour turnover

• Capacity utilization

• Average unit production

• Working capital/sales etc

Learning and development

• R&D expenditure/sales

• New markets entered

• New products

• Investment/total assets

• Training expenditure/sales etc

Social

• Employee satisfaction

• Social performance of suppliers

• Community relationships

• Philanthropic investments/revenue or profit

• Industry-specific factor e.g. community open days

Environmental

• Key material usage/unit

• Energy usage/unit

• Water usage/unit

• Emissions, effluent & waste/unit or as % of total resources used

• Industry-specific factor e.g., GHG emissions

To improve competitive performance, there is need for organizations to address to sustained competitive performance.

• These include but not limited to:

• Inadequate or unavailable resources

• Poorly communicated strategy

• Actions required to execute not clearly defined

• Unclear accountabilities for execution

• Organizational silos and culture blocking execution

• Inadequate performance monitoring

• Inadequate consequences or rewards for failure or success

• Poor leadership

• Uncommitted leadership

• Unapproved strategy

• Other obstacles (including inadequate skills and capabilities)

Porter‘s model is the most popular and most relevant for open market economies. Porter discusses five forces that determine the nature of competition in an industry. These are: threat of new entrants, rivalry among industry competitors, threat of substitute products, bargaining power of suppliers, and bargaining power of customers. The power of each force tends to vary in different industries. Even in the same industry the power varies over time.

1. Threat of new entrants

This depends on entry barriers, such as:

- Economies of scale

- Proprietary product differences

- Brand identity

- Switching costs

- Capital requirements

- Access to distribution

- Government policy

2. Rivalry within the industry

This depends on factors such as:-

- Industry growth rate

- Product differences

- Brand identity

- Switching costs

- Exit barriers

3. Threat of substitute products

Substitute here refers to products of other industries that can be used to substitute the industry’s products e.g. gas is a substitute for electricity. Power or threat of substitutes depends on factors such as:

- Relative price performance of substitutes

- Switching costs

- Buyer propensity to substitute

4. Supplier power

This depends on factors such as:

- Differentiation of inputs

- Switching costs of suppliers and firms in the industry

- Presence of substitute inputs

- Supplier concentration

- Threat of forward integration relative to threat of backward integration by firms in the industry.

5. Buyer power

This depends on factors such as:-

- Buyer concentration versus firm concentration

- Buyer volume

- Buyer switching costs relative to firm switching costs

- Ability to backward integrate

- Substitute products

- Price sensitivity

- Product differences

- Brand identity

Porter‘s five-force model is most applicable in open-market economies where the forces are not constrained in any way.

The model does not apply in all industries equally because some industries may have restrictions.

In what industry in Kenya is the model least applicable? Scholars have modified the model in various ways by adding other

forces.

DOMINANT ECONOMIC FEATURES

A dominant feature in an industry is an outstanding factor that characterizes the industry. Extreme factors rather than moderate factors tend to be outstanding. For example, market size will be a dominant feature if it is too small or too large in the industry.

Dominant features usually include the following. The dominant features among these will depend on the industry. This is a checklist.

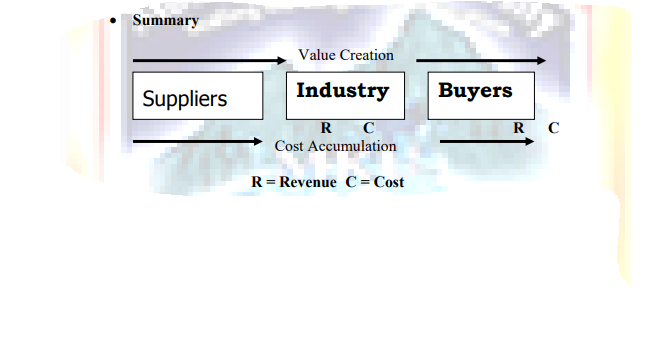

- Market size

Suppliers Industry Buyers - Market growth rate

- Scope of competitive rivalry e.g. whether local, national, regional, or global.

- Number of rivals and their relative sizes.

- Number of buyers and their relative sizes.

- Extent of product differentiation.

- Extent of vertical integration.

- Extent of horizontal integration.

- Distribution channels used

- Resource requirements

- Ease of entry or exit

- Learning and experience effects

- Industry profitability or attractiveness

- Capacity utilization i.e. levels required to achieve production efficiency

DRIVERS OF CHANGE

- A driver of change in an industry refers to what is causing change in the industry i.e. what is making the industry to change.

- It is meaningless to talk of a driver of change in a static industry.

- Drivers of change in an industry usually includes:-

- Changes in long term industry growth rate

- Changes in buyers or users of the product

- Changes in uses of the product

- Product innovation

- Market innovation

- Technological change

- Globalization

- Government policy changes

KEY SUCCESS FACTORS (KSF)

- A success factor in an industry is a factor that enables firms in the industry to succeed.

- In an industry, success factors may be many, but key ones or those with strongest effect are few.

- Key success factors vary across industries and includes:

- Management

- Human resources

- Equipment or facilities

- Cost of production and operations

- Prices or rates

- Product quality

- Service quality

- Customer care

- Volume of operations or sales

- Image or reputation

- Marketing effectiveness

- Finance

- Technology

- Research and Development

- Location

- Processes or systems

- Key success factors in an industry may be identified through:

- Experience or knowledge of the industry

- Expert opinion

- Research/survey

- Competence on key success Sound strategy incorporates efforts to be competent on all key industry success factors and to excel on at least one such factor.

- Factors determine a firm‘s competitive position in the industry.

Analysis of competitive position may be based on any one of the following:

- Sales volume

- Profits

- Firm size

- Technology

- Key success factors

- Key success factors is the best gauge of competitive position because it is a composite index unlike the others, which are single factor indexes (unidimensional indexes).

Competitive position analysis can be done as shown using key success factors.

COST LEADERSHIP

This is one of the generic strategies by Michael porter. This is organizations doing everything to achieve a CA through producing products or services at a lower unit cost (lowering cost structure) – charge a lower price. Increase efficiency and lower costs – the

manufacturing and materials management functions are the center of attention. A lowlevel of product differentiation, it means that you do not want to be the industry leader in differentiation. Target the average customer Scale and Focus, not Product Variety.

Ignores the different market segments and focuses on mass market. Generally, cost leadership is about being the lowest cost producer in the industry. For an organization to gain competitive advantage, it must achieve overall cost leadership in an industry it is competing in. For companies competing in a ―price-sensitive‖ market, cost leadership is the strategic imperative of the entire organization. It is vitally important for these companies to have a thorough comprehension of their costs and cost drivers in

order to pursue a cost leadership strategy. They also need to fully understand their targeted customer group‘s definition of quality, usually denoted in terms of design specifications, contractual requirements, delivery and services at the lowest possible cost.

Of particular importance will be for the company to attain a cost level that is low relative to its competitors.

Advantages

- charge a lower price yet make the same level of profit.

- win in the price war.

- low-cost as an entry barrier.

- protected from rivals.

- less affected by powerful buyers and suppliers.

- room to reduce its price to compete with substitute products.

Disadvantages

- technological advancement makes the low cost advantage outdated.

- imitation ability of competitors.

- lose sight of changes in customers‘ tastes

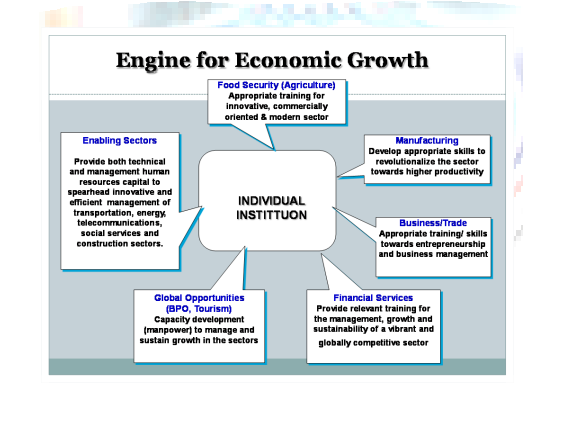

Cost leadership = aggressively seeks efficient facilities, pursues cost reductions, and uses tight cost controls to produce products more efficiently than competitors. Cost leadership does not only benefit the individual institution but also helps grow the economy because

economic activities are multiplied. For example a few sectors in Kenya Economy towards achieving Vision 2030 as shown below:-