MONDAY: 5 December 2022. Afternoon Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings.

Do NOT write anything on this paper.

QUESTION ONE

1. Outline FOUR disadvantages of using the scatter graph as a method of cost estimation. (4 marks)

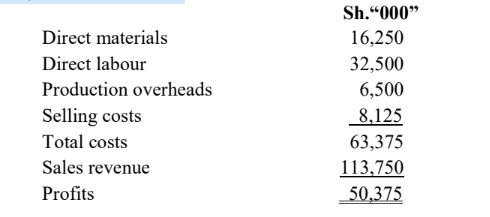

2. Remah Ltd has established the following information for the costs and revenues for the month of October 2022 at an

activity level of 500 units:

Additional information:

1. All direct costs are variable costs.

2. 20% of selling costs and 50% of the production overheads are fixed over all levels of activity respectively.

Required:

Determine cost estimation equation in the form Y = a + bx using the account analysis method. (4 marks)

Calculate the total profit at an activity level of 1,000 units. (3 marks)

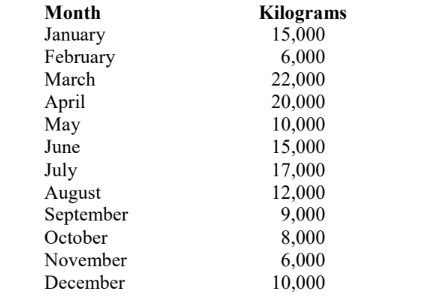

3. Moyalematt supermarket maintains a variety of inventory.

The following information is given for stock item “Z”:

1. Consumption in kilograms per month:

2. Lead time is 5 – 8 days.

3. Annual holding cost per unit per annum is Sh.26.60.

4. The purchase price is Sh.200 and discounts are not allowed.

5. The ordering cost per order is Sh.798.

6. The annual demand is the accumulated monthly consumption.

Required:

1. The optimal economic order quantity (EOQ). (3 marks)

2. Frequency of placing orders. (2 marks)

3. Reorder level. (2 marks)

4. Maximum inventory level. (2 marks)

(Total: 20 marks)

QUESTION TWO

1. Outline FOUR assumptions of cost volume profit (CVP) analysis. (4 marks)

2. Highlight FOUR factors influencing wage rate determination. (4 marks)

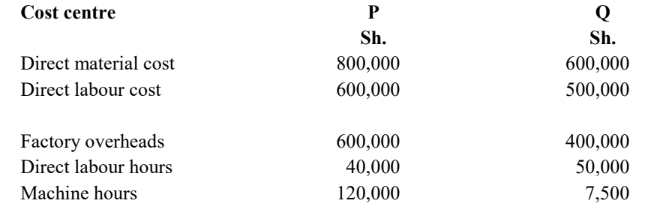

3. Toto enterprise manufactures dolly kits for children. It is currently considering various techniques of overhead

absorption that are more efficient to apply to job costing:

Required:

Calculate the overhead absorption rate (OAR) on the following basis:

1. Percentage of direct material cost basis for cost centre P. (2 marks)

2. Direct labour hours basis for cost centre Q. (2 marks)

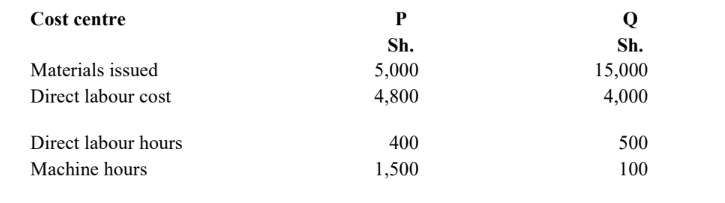

3. A particular job marked as Job number JB22 consumed the following inputs during the year:

Additional information:

1. Administration overheads are absorbed at the rate of 20% on factory costs.

2. Profit mark-up is 331/3 % on cost.

Required:

Calculate the total cost and total sales for Job number JB22. (6 marks)

Assuming the job number JB22 consists of 50 items, calculate the selling price per unit. (2 marks)

(Total: 20 marks)

QUESTION THREE

1. Explain FOUR functions of management accounting in decision making. (8 marks)

2. Identify FOUR sources of loss in process costing. (4 marks)

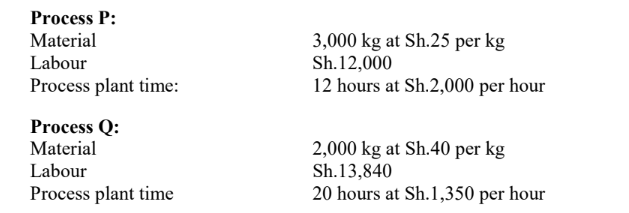

3. Oilivya Ltd. manufactures an industrial lubricant, which is formed by subjecting certain crude oil chemicals to two

successive processes namely; P and Q. The output of process P is passed to process Q where it is blended with other

chemicals.

The process costs for period 3 were as follows:

Additional information:

1. General overhead cost for the period amounted to Sh.27,200 and is absorbed into process costs on a process

labour basis.

2. The normal output of process P is 80% of input, while that of process Q is 90% of input.

3. Waste matter scrapped from process P is sold for Sh.2 per kg, while that from process Q is sold for Sh.3 per kg.

4. The output for period 3 were as follows:

• Process P 2,300 kg

• Process Q 4,000 kg

5. There was no stock or work in progress at either the beginning or the end of the period, and it may be assumed

that all available waste matter had been sold at the prices indicated.

Required:

Prepare the following process accounts:

1. Process P. (4 marks)

2. Process Q. (4 marks)

(Total: 20 marks)

QUESTION FOUR

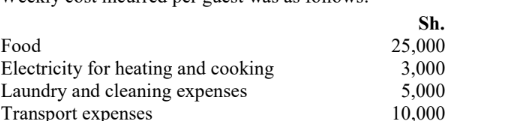

1. Kandogo guest house operates service costing system.

The following costs were incurred during a 30-week year:

1. Weekly cost incurred per guest was as follows:

2. The hotel operates for 30 weeks a year.

3. Fifteen guests are received per week.

4. Each guest is charged Sh.100,000 per week.

5. Fixed salary and supervision expenses are Sh.11,000,000 per annum.

6. Rent and rates for the property per annum is Sh.4,000,000.

7. Recreation and accommodation fixed costs are Sh.1,000,000 per annum.

Required:

Total cost per annum. (4 marks)

Cost per guest per week. (3 marks)

Hotel profit/(loss) per guest per week. (3 marks)

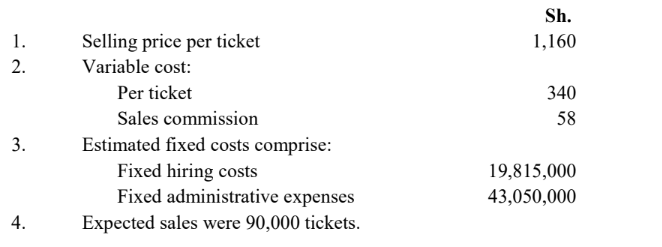

2. Furahia Ltd. operates in the entertainment and event organising industry and one of its activities is to promote

concerts at locations through-out the county.

The company is examining the viability of a concert in Raha County.

Selling price, fixed costs and variable costs will comprise of the following cost structure:

Required:

1. The number of tickets that must be sold to break-even. (4 marks)

2. The number of tickets to be sold to earn Sh.5,715,000 target profit. (2 marks)

3. The profit, assuming 85,000 tickets are sold. (2 marks)

4. The number of additional tickets that must be sold to cover extra cost of television advertising of Sh.13,335,000. (2 marks)

(Total: 20 marks)

QUESTION FIVE

1. By citing ONE example for each, define the following types of costs:

Avoidable costs. (2 marks)

Prime costs. (2 marks)

Marginal costs. (2 marks)

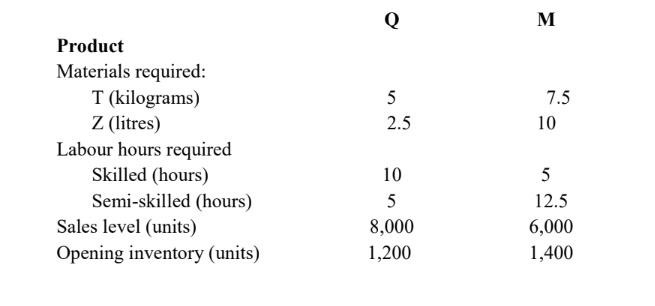

2. Derap Enterprise wishes to prepare a master budget for the forthcoming period. Information regarding products, costs

and sales levels is as follows:

Additional information:

1. Opening inventory of material T was 14,075 kilograms and for material Z was 15,750 litres.

2. Closing inventory of finished goods will be sufficient to meet 20% of sales demand.

3. Closing inventory of materials will be sufficient to meet 25% of production requirements.

4. Material prices are Sh.15 per kilogram for material T and Sh.12 per litre for material Z.

5. Labour costs are Sh.120 per hour for the skilled workers and Sh.80 per hour for the semi-skilled workers.

Required:

Prepare the following functional budgets:

1. Production budgets in units only. (3 marks)

2. Material usage budget in kilograms and litres. (3 marks)

3. Material purchases budget in kilograms, litres and shillings. (4 marks)

4. Labour budget in hours and shillings. (4 marks)

(Total: 20 marks)