MONDAY: 5 December 2022. Afternoon Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Do NOT write anything on this paper.

QUESTION ONE

1. Explain the following terms in relation to term structure of interest rates:

Non-parallel shift. (2 marks)

Yield curve twists. (2 marks)

Butterfly shifts. (2 marks)

2. The current 6-month rate is 3.5% and the 6-month forward rates (all on semi-annual basis) are shown below:

A bond has 1.5 years to maturity and has an annual coupon of 4%. The bond has a par value of Sh.100.

Required:

Derive the spot rates from the forward rates. (4 marks)

Determine the value of the bond based on the spot rate in (b) (i) above. (2 marks)

3. A bond investor holds a three-year bond with an annual coupon rate of 12% and a yield to maturity of 9%.

The bond has a face value of Sh.1,000.

Required:

Calculate the bond’s convexity. (5 marks)

4. The flat price on a fixed rate corporate bond falls one day from 92.25 to 91.25 per Sh.100 of par value. This is due to poor earnings and unexpected rating downgrade of the issuer. The annual modified duration for the bond is 7.24.

Assume that the benchmark yields remain unchanged.

Required:

Calculate the percentage price change. (1 mark)

Determine the estimated change in the credit spread. (2 marks)

(Total: 20 marks)

QUESTION TWO

1. Explain THREE factors that might affect the spread on corporate bonds. (6 marks)

2. Outline THREE classifications of global bond markets. (3 marks)

3. A 3-year 4.25% coupon bond is puttable at par one year and two years from today. Coupon is payable annually.

Additional information:

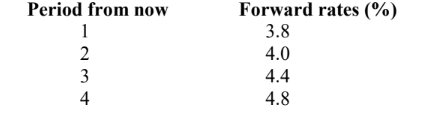

1. One year forward rates are as follows:

0 year from now 2.5%

1 year from now 3.518%

2 years from now 4.564%

2. The par value is Sh.100.

3. Assume that there is zero volatility.

Required:

Calculate the value of the investor put option. (5 marks)

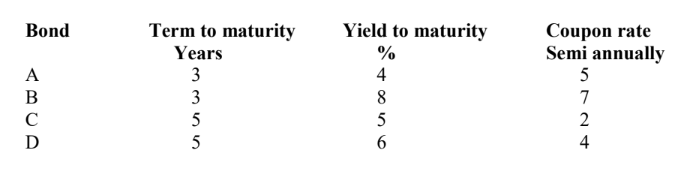

4. The following information is provided about four comparable bonds:

The bonds have a par value of Sh.100

Required:

Determine the price of a 4-year, 6% semiannual coupon rate bond. (6 marks)

(Total: 20 marks)

QUESTION THREE

1. Describe TWO methods used to estimate interest rate volatility. (4 marks)

2. Explain THREE characteristics of equilibrium term structure models. (6 marks)

3. Juma Ali decides to buy a four year zero coupon corporate bond and then sell it after two years. The bond’s par value is Sh.100. The swap rate is used as a proxy for corporate yields. He gathers the following information on spot rate for on the run annual coupon government securities and swap spreads.

Required:

Determine Juma Ali’s return. (3 marks)

4. James Bondoku purchased a bond between coupon periods. The period between the settlement date and the next coupon payment date is 120 days. There are 182 days in the coupon period. The bond has a coupon rate of 14% per annum and a discount rate of 12%. The bond has a face value of Sh.10,000 with five semiannual coupon payments remaining.

Required:

The accrued interest of the bond. (2 marks)

The full price of the bond. (4 marks)

The clean price of the bond. (1 mark)

(Total: 20 marks)

QUESTION FOUR

1. Explain the following types of bonds:

Samurai bonds. (2 marks)

Junk bonds. (2 marks)

Serial bonds. (2 marks)

2. A two-year floating rate note pays 6 month LIBOR plus 80 basis point. The floater is priced at Sh.97 per 100 of

par value. Current 6 month LIBOR is 1%.

Assume a 30/360-day count convention and evenly spaced periods.

Required:

Calculate the discount margin for the floater in basis point. (5 marks)

3. Bancy Ruri is valuing a floater issued by Biashara Bank. The floater has a par value of Sh.100, three-year life and pay based on annual LIBOR. Bancy has generated the following binomial tree for LIBOR:

1 year forward rates starting in year:

Required:

Calculate the value of a capped floater with a cap of 4%. (3 marks)

Determine the value of the cap in a capped floater with a cap of 4% (2 marks)

4. The following spot rates are available:

3-year spot rate 4.752%

5-year spot rate 5.2772%

Required:

Determine the 2-year forward rate three years from now on a bond equivalent basis. (4 marks)

(Total: 20 marks)

QUESTION FIVE

1. In relation to bonds with embedded options:

Citing two suitable examples, explain the term “lattice”. (4 marks)

Describe the concept of backward induction valuation. (2 marks)

2. The yield to maturity (YTM) for a benchmark one-year annual pay bond is 2% for a benchmark two-year annual pay bond is 3% and for a benchmark three-year annual pay is 4%. A three year 5% coupon, annual pay bond with the same risk and liquidity as the benchmark is selling for Sh.102.7751 today to yield 4%.

Required:

Determine whether the value is correct for the bond given the current term structure. (5 marks)

3. Lucy Biba, an investor buys the 10-year, 8% annual coupon payment bond at Sh.85.5031 per 100 of par value and sells it in four years. After the bond is purchased, interest rates go up to 11.40%.

Required:

Calculate Lucy Biba’s realised return four-year horizon yield. (5 marks)

4. A 90-day Treasury bill currently has a price of Sh.9,800 and a face value of Sh.10,000. There are 365 days in a year.

Required:

Calculate the yield on discount basis. (2 marks)

Calculate the yield on a money-market basis. (2 marks)

(Total: 20 marks)