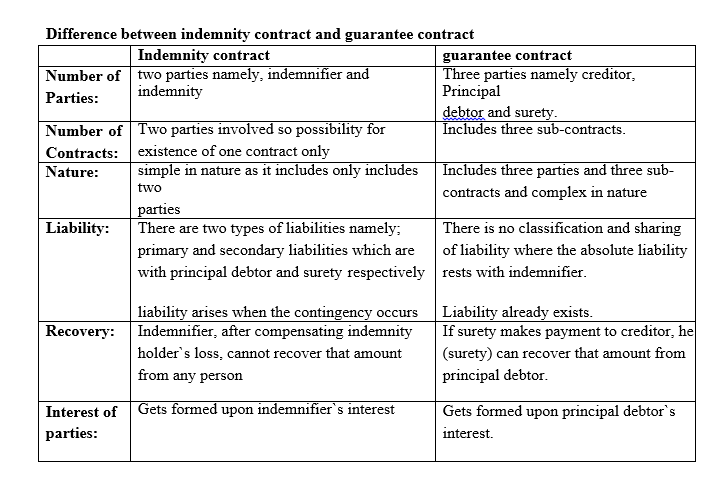

When one person signifies to perform the contract or discharge the liability incurred to the third party, on behalf of the second party, in case he fails, then there is a contract of guarantee. In this type of contract, there are three parties, i.e. The person to whom the guarantee is given is Creditor, Principal Debtor is the person on whose default the guarantee is given and the person who gives guarantee is Surety(Guarantor).

Three contracts will be there, first between the principal debtor and creditor, second between principal debtor and surety, third between surety and the creditor. The contract can be oral or written. There is an implied promise in the contract, that the principal debtor will indemnify the surety for the sums paid by him as an obligation of the contract provided they are rightfully paid. The surety is not entitled to recover the amount paid by him wrongfully.

- Example: Y is in need of ksh.. 10000/-. Upon guarantee by Z, Y has got the amount from Here X, Y and Z are creditor, principal debtor and surety respectively.

- Example: Here we have another example of the contract of guarantee, Mr. kamau takes a loan from the bank for which Njoroge has given guarantee that if

Kamau default in the payment of the said amount he will discharge the liability. Here Njoroge plays the role of surety, Kamau is principal debtor and Bank is the creditor.

Types of guarantee

- Sole Guarantee: This is a contract of guarantee whereby the guarantor’s liability is restricted to a single

- Continuing Guarantee: It is a contract of guarantee under which the guarantors to a series of transactions. This type of guarantee terminates on the death of the guarantor provided the notice is made know to creditor as was the case in Bradbury V. Morgan. The guarantor is also free to revoke the guarantee at any time.

- Fidelity Guarantee: It is a contract of guarantee whereby a person guarantees the honesty good behaviour of another purpose of employment

Characteristics of contract of gurantee

- It consists of 3 parties namely the guarantor, creditor and the principal

- The guarantor’s liability is secondary or collateral

- The guarantor has no interest in the transaction between the

- The contact must be evidenced by some note or

Discharge of the guarantor

The guarantor may be discharged in any of the following ways:-

- Payment of the amount due by the debtor or fulfilment of the obligation arising.

- If the creditors action against the debtor becomes statute

- If the transaction between the credit and the principal debtor becomes illegal by reason of change of law or

- Revocation of the guarantee by the guarantor

- Death of guarantor

- Variation of the terms of the contract without the guarantor’s consent

- If it is established that the guarantee was obtained by fraud, misrepresentation or concealment of material

- Failure by the creditor to take steps that was necessary to protect his own

- Discharge of a co-guarantor discharges

RIGHTS AND DUTIES OF THE PARTIES

Right of the indemnity holder/ indemnified

An indemnity holder (i.e. indemnified) acting within the scope of his authority is entitled to the following rights –

- Right to recover damages – he is entitled to recover all damages which he might have been compelled to pay in any suit in respect of any matter covered by the contract.

- Right to recover costs – He is entitled to recover all costs incidental to the institution and defending of the

- Right to recover sums paid under compromise – he is entitled to recover all amounts which he had paid under the terms of the compromise of such suit. However, the compensation must not be against the directions of the indemnifier. It must be prudent and authorized by the indemnifier

- Right to sue for specific performance – he is entitled to sue for specific performance if he has incurred absolute liability and the contract covers such liability. The promisee in a contract of indemnity, acting within the scope of his authority, is entitled to recover from the promisor-

- all damages which he may be compelled to pay in any suit in respect of any matter to which the promise to indemnify applies

- all costs which he may be compelled to pay in any such suit if, in bringing or defending it, he did not contravene the orders of the promisor, and acted as it would have been prudent for him to act in the absence of any contract of indemnity, or if the promisor authorized him to bring or defend the suit ;

- all sums which he may have paid under the terms of any compromise of any such suit, if the compromise was not

It is important to note here that the right to indemnity cannot be claimed of dishonesty, lack of good faith and contravention of the promisor’s request. However, the right cannot be negatived in case of oversight.

Right of Indemnifier –

Indemnifier’s right are similar to those of surety (discussed below)

Where one person has agreed to indemnify the other, he will, on making good the indemnity, be entitled to succeed to all the ways and means by which the person indemnified might have protected himself against or reimbursed himself for the loss. [Simpson v Thomson]

Rights of Surety/Guarantor

Rights of Surety can be classified into three groups, as follows;

- Rights against Principal

- Rights against

- Rights against Co-Sureties.

Rights against Principal Debtor

- Right to give Notice: Whenever creditor comes to surety, for the purpose of seeking payment, surety can give a notice to principal debtor to settle the

- Rights of Sub-rogation: Sub rogation is a process where rights will get shifted from one person to the other. If surety makes payment to creditor, surety gets all rights of creditor by sub-rogation and from then onwards surety can behave like a

- Right of Indemnity: Principal of indemnity operates between principal debtor and surety where principal debtor becomes implied indemnifier and surety becomes implied indemnity holder. Therefore, surety can make principal debtor answerable for all

- Right to get Securities: In case where surety makes payment to creditor, surety has right to get the securities given by principal debtor to

- Right to ask for Relief: From the date of guarantee, besides creditor, surety also can bring pressure on principal debtor in connection with settlement of

Rights against Creditor

- Right to get Securities: If Surety makes payment to creditor, surety can get all securities into his possession from

- Right to ask for Set-off: Surety can give advice to creditor to sell away the security and to utilize the amount thus realized for set

- Rights of Sub-rogation: When ever surety makes payment to creditor, creditor foregoes or looses all of his rights in his capacity as creditor and those rights will be attained by

- Right to advice to Sue Principal Debtor: Surety has right to give advice to creditor to proceed legally against principal debtor for the purpose of recovering the

- Right to insist on Termination of Services: In case where guarantee is with regard to conduct of an employee, surety can insist on termination of services of employee. Here employees status is equal to that of creditor and employee’s status is equal to that of principal

Rights against Co-Sureties

- Right to ask for Contribution: Surety can ask his co-sureties to contribute the amount when principal debtor comes across default. If they have given guarantee for equal amounts, they have to contribute equally. In case where guarantee is given for in equal amounts, the mode of contribution differs from England law to Indian law. As per England law contribution is to be made in the ratio of guarantee amounts. But as per Indian law the deficit amount is to be distributed to all sureties equally and every surety will contribute share of deficit or guarantee amount whichever is

- Right to claim Share in Securities: When co-Sureties make payment to creditor, they get securities from creditors procession. Then every surety can claim his share in those

ADVANTAGES AND DISADVANTAGES OF GUARANTEE AS SECURITY

Advantages

Following are the important advantages of the guarantee:

- It is very easier security as compared to mortgage of

- It gives maximum protection to the

- The sign can be easily obtain from the guarantor on the form by the bank and there is no need of preparing

- The banker may call guarantor and tell him about the default of

- By a simple court action a guarantee can be

- In case of default a banker and guarantor both pressurize the borrower to repay the debt.

Disadvantages

- If the guarantors property is destroyed or sold during the period of contract and borrower also fails to pay the debt. In this case it is very difficult to recover the amount from both the

- Sometimes if the bank changes the constitution then guarantee is

- Sometimes the loan is not returned and bank claims in the court against the guarantor but it is rejected on technical

- In case of amalgamation with other banks the guarantee is

Sureties Secondary Liability

Situations where sureties secondary liability comes to an End

In a contract guarantee surety comes across secondary liability. The following are situations where sureties secondary liability comes to an end.

- Discharge by revocation of

- Discharge by activities of

- Discharge by invalidation of guarantee

Discharge by revocation of guarantee: The following are Situations where revocation of guarantee takes place by terminating secondary liability of Surety.

- By Notice

- By Death

- By

- By Notice: Surety can revoke his guarantee by giving a notice to creditor. Guarantees are of two types. Namely; Specific guarantee and Continuing guarantee. If guarantee is given to a particular debt, it is called specific guarantee. Specific guarantee cannot be revoked by notice on the other hand if guarantee extends to a group of debts, it is called continuing guarantee. Continuing guarantee can be revoked by giving notice. But here surety will be held liable to debts borrowed by principal debtor before such

- By Death: Whenever surety comes across death, then his secondary liability comes to an end. But sureties legal representative will be held liable. In case where surety has given specific guarantee legal representative has to take up the secondary liability absolutely. In case where surety has given continuing guarantee, legal representative is liable to the debts granted by creditor to principal debtor till data of filing death notice by legal

- By Renewal: Whenever renewal of guarantee contract takes place, old guarantee comes to an end. For example: There is a contract of guarantee among X, Y and Z who are creditor, principal debtor and surety respectively. There after Y has arranged Mr. A as surety in place of Z. As a consequence Z`s guarantee gets revoked and Z`s secondary liability goes

Discharge by activities of creditor: Whenever creditor renders any of the following activities, surety gets discharges from his secondary liability.

- Realizing principal

- Improper dealings with principal

- Loosing

- Alterations: In case where creditor makes material alterations in guarantee contract deed, without consent of surety discharge of Surety takes place. A case on this point is Witcher Vs Hall. In this case, creditor fraudulently alters the deed and surety gets decree from the court saying that he has no secondary

- Releasing principal debtor: If creditor releases principal debtor from principal liability automatically sureties secondary liability also comes to an end. A case on this point is Hewson Vs Ricketts. In this case the creditor releases principal debtor and after coming to know about it, surety gets decree from court that he (surety) is also

- Improper dealings with principal debtor: If creditor collides with principal debtor and tries to defraud Surety, then also discharge of surety takes place. A case on this point is Midlon motor show rooms Vs Newman. In this case creditor joins hands with principal debtor and thus makes effort to cheat surety. Here court decides that surety has no secondary

- Loosing securities: At times the principal debts may give additional securities also in support of the death besides personnel validity. Whenever creditor looses such securities, both primary and secondary liabilities will go out of

Discharge by invalidation of guarantee contract: When guarantee contract becomes invalid and surety will have no secondary liability. The following are situations where guarantee Contract becomes invalid.

- Mis-Representation

- Concealment

- No flow of consideration

- Absence of other essentials of valid

- Co-surety not

- Mis-Representation: When surety is made involved in guarantee contract by means of fake representation, guarantee contract becomes invalid and Surety gets discharged.

- Concealment: When Surety is made involved in guarantee contract by concealing material facts, then also discharge of surety takes

- No flow of consideration: When creditor does not grant the loan as per the terms, there is no question of primary as well as secondary

- Absence of other essentials: Besides consideration, the contract should have certain other features also, to attain validity. When guarantee contract is deficient in any one of those features, guarantee contract becomes

- Co-surety not joining: At times the surety may insist on presence of another surety. Then the guarantee contract becomes contingent contract. In case where such condition is not full filed i.e. co-surety does not join, it becomes invalid.