TUESDAY: 6 December 2022. Afternoon Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Any assumptions made must be clearly and concisely stated. Do NOT write anything on this paper.

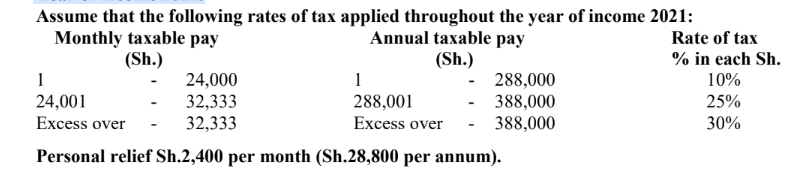

RATES OF TAX (Including wife’s employment, self-employment and professional income rates of tax).

Year of income 2021.

QUESTION ONE

1. The tax law envisages various approaches and levels of resolving tax disputes, including the administrative decisions, quasi-judicial process involving tax appeals tribunal (TAT), formal judicial process involving the High Court or appeal to the Court of Appeal and alternative dispute resolution. Some of the relevant laws include the Tax Procedures Act, Tax Appeals Tribunal Act and other relevant tax laws.

Required:

With reference to the above statement and quoting relevant tax provisions, explain the application of each of the following in tax disputes settlement:

Tax appeals tribunal. (3 marks)

High Court. (3 marks)

Court of Appeal. (3 marks)

Out of Court settlement. (3 marks)

2. Consider the following hypothetical case:

Axe Ltd., incorporated in your Country, signed a service agreement to provide marketing and liaison services to the related non-resident entities located in the United Kingdom (UK). Under the agreement, Axe Ltd. was to be compensated off cost plus mark-up basis. The related non-resident entities executed separate agreements with distributors of their products who they invoiced directly. The revenue authority imposed value added tax (VAT) on the above marketing services provided by Axe Ltd.

On the other hand, Axe Ltd. argued that the marketing support services enhanced brand awareness of the products sold by the non-resident entities in your country. On this basis, the services were exported, hence zero-rated. The above case has been bought before the tax tribunal.

Required:

Discuss TWO factors that the Tribunal might consider in ruling in favour of Axe Ltd. (4 marks)

3. Explain TWO ethical principles governing the services provided by tax practitioners. (4 marks)

(Total: 20 marks)

QUESTION TWO

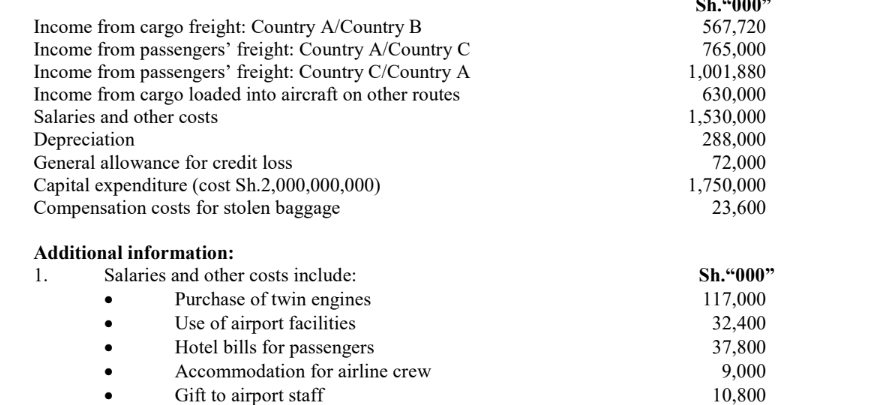

1. Mawingu Ltd. is a foreign subsidiary company operating a fleet of passenger and cargo aircrafts in Country A.

The flights are between Country A and other countries. The operating results for the year ended 31 December 2021 are as follows:

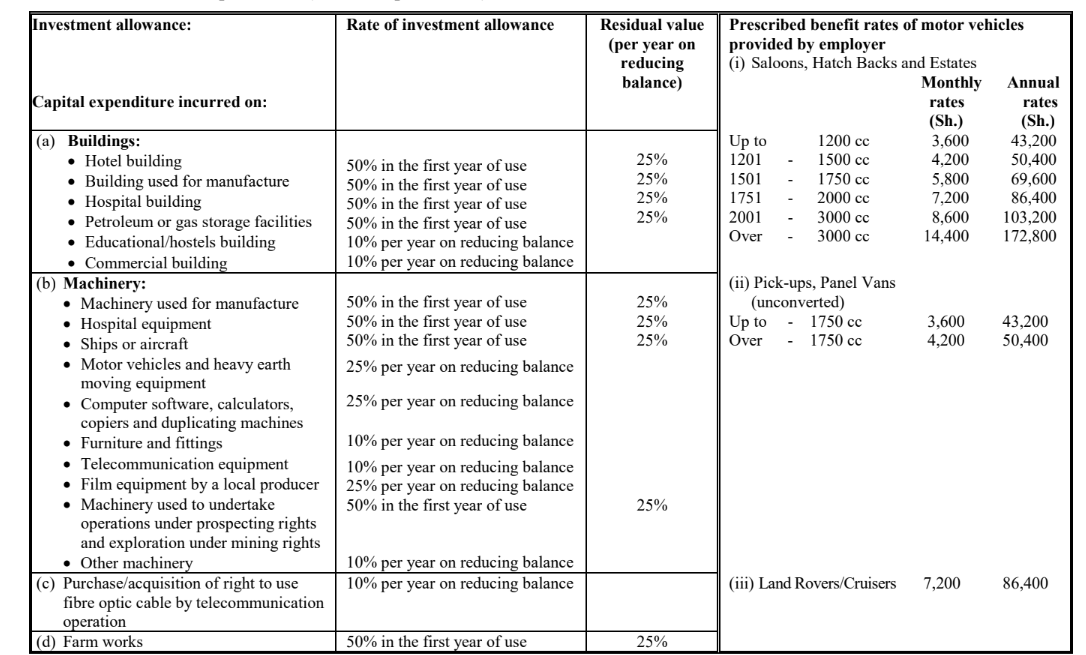

2. Investment allowances were agreed with the Revenue Authority at 85% of depreciation charged in the account.

3. Assume a corporation tax rate of 30%.

Required:

Compute adjusted taxable profit or loss of Mawingu Ltd. for the year ended 31 December 2021. (8 marks)

Compute tax payable (or refundable) for Mawingu Ltd. (2 marks)

2. ZamZam Company Ltd. purchased a property whose cash price was Sh.1,264,000 under the following terms:

1. The deposit paid for the purchase of the property was Sh.400,000.

2. The balance of the purchase price was to be paid over a 3-year period at a monthly instalment of Sh.40,000 inclusive of Sh.16,000 per month as mortgage interest.

Required:

Assuming the property was sold as follows:

Option I: For Sh.2,000,000 after payment of twenty-four instalments.

Option II: For Sh.2,680,000 after full payment of all the instalments, cost of valuation Sh.54,000 and legal fees Sh.72,000.

Calculate capital gains tax under each option. (6 marks)

3. Darubini Ltd. is under tax investigation by the Revenue Authority, accused of obstructing/hindering the investigation officer in the exercise of his function.

Highlight FOUR aspects that may constitute obstruction in the above case. (4 marks)

(Total: 20 marks)

QUESTION THREE

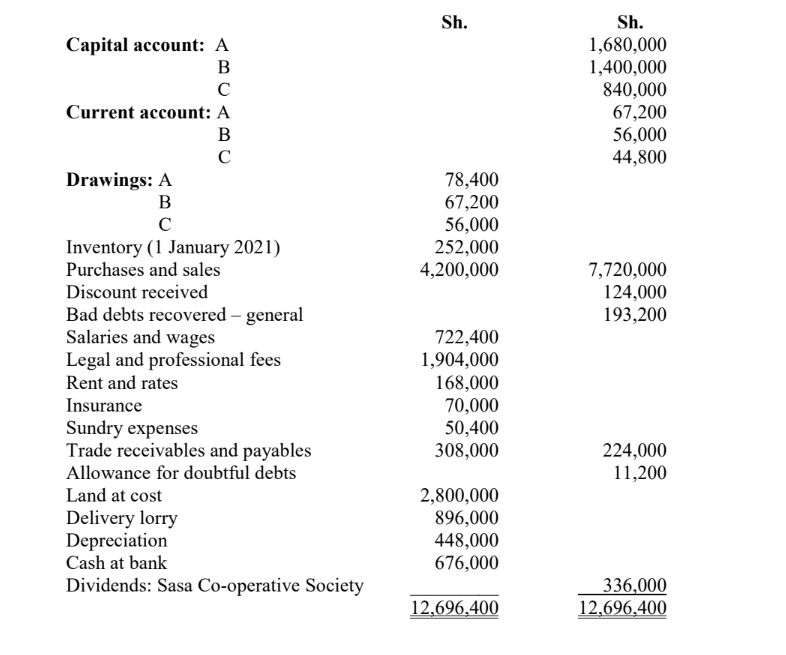

1. A, B and C have been trading in a small size partnership sharing profits and losses in the ratio of 2:2:1 respectively. C retired from the partnership on 31 August 2021 while A and B agreed to continue with the business charging interest on capital at the rate of 15% per annum as in the previous period when C was still in the partnership. Due to the changes in the partnership, goodwill was valued at Sh.1,200,000 and was to be written off immediately.

The following trial balance was extracted as at 31 December 2021:

Additional information:

1. Sales and purchases were inclusive of value added tax (VAT) at the rate of 16%. Cash sales amounted to Sh.358,400 (VAT inclusive) and were excluded from the above accounts.

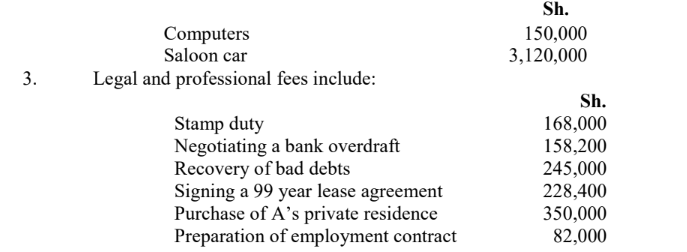

2. The following assets were acquired by the business immediately after retirement of C.

4. Interest on drawings was charged at the rate of 10% per annum.

5. Inventory at year end was valued at Sh.364,000 and the partnership had consistently undervalued inventory at each year end by 20%.

6. Salary and wages include partners’ salary of Sh.420,000 shared by the partners according to the profit and loss sharing ratio.

7. Allowance for doubtful debts was to be increased to Sh.24,800 at year end. Bad debts written off amounted to Sh.40,000 of which Sh.8,000 relates to general bad debts.

8. Prepaid insurance at the beginning of the year amounted to Sh.8,000 while insurance owing at year end amounted to Sh13,000.

9. Accrued sundry expenses as at 1 January 2021 and 31 December 2021 amounted to Sh.10,000 and Sh.2,000 respectively.

10. C was paid all his dues on 15 September 2021. The profits and losses were to be shared equally after C’s retirement.

11. Unless otherwise stated, assume that all revenues and expenses accrued evenly throughout the year.

Required:

Prepare a statement of adjusted taxable profit or loss for the partnership for the year ended 31 December 2021. (10 marks)

Determine the taxable income for each partner. (6 marks)

2. The Commissioner is empowered to cancel or terminate the license of any person acting as a tax agent at any time.

Summarise FOUR circumstances under which this may be possible. (4 marks)

(Total: 20 marks)

QUESTION FOUR

1. The African Growth and Opportunity Act (AGOA) is a United States Trade Act enacted in year 2000 as a legislation that significantly enhances market access to the United States for qualifying Sub-Sahara African countries.

Analyse THREE conditions that the above countries must meet in order to qualify and be eligible for AGOA consideration. (6 marks

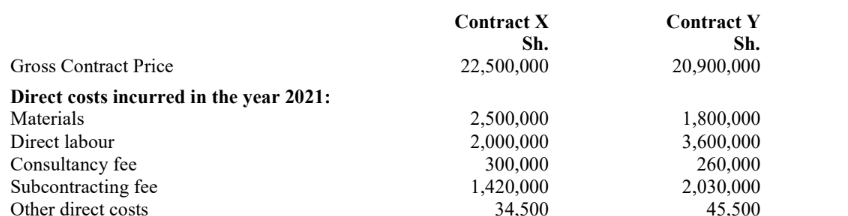

2. Mijengo Contractors Ltd. is a resident firm engaged in the property development business. As at 1 January 2021, the firm secured two construction contracts namely X and Y which are to be completed within a period of two years.

The information relating to the contracts is as flows:

Additional information:

1. Contract X’s material cost includes material costing Sh.240,000 that remained at the site as at 31 December 2021, while under contract Y, material costing Sh300,000 was sold during the year.

2. The company estimates that costs to be incurred to complete the contract work will be 150% of the contract costs incurred in the current year for both contracts.

3. The company computes taxable revenue on the basis of the percentage of completion method for the two contracts.

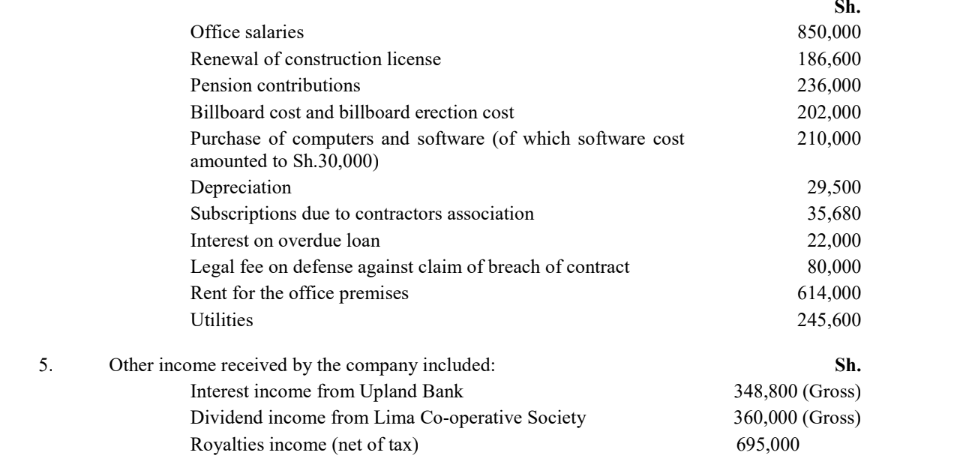

4. Analysis of general and administrative expenses for the year is as follows:

Required:

Compute the total taxable income for Mijengo Contractors Ltd. for the year ended 31 December 2021. (12 marks)

Compute the tax payable (if any) by Mijengo Contractors Ltd. (2 marks)

(Total: 20 marks)

QUESTION FIVE

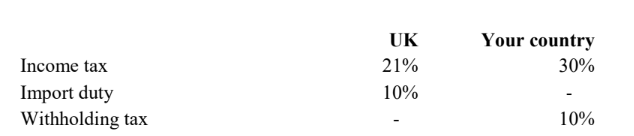

1. Zamon UK is a multinational corporation in UK with a wholly owned subsidiary, Zamon XL based in your country.

In the year ended 31 December 2021, Zamon XL produced 50,000 kilograms of coffee from its farm at a cost of Sh.200 per kilogram exclusively meant for export to Zamon UK at a predetermined price of Sh.300 per kilogram although the market price was Sh.600 per kilogram.

Zamon UK sold all the coffee in the UK market at Sh.1,200 per kilogram.

Additional information:

1. Tax rates are as follows:

2. The subsidiary repatriates all profits as dividends.

Required:

Compute the total tax lost by the Revenue Authority as a result of this transfer pricing arrangement. (5 marks)

2. Comparability analysis in transfer pricing arrangements involves comparison of the conditions in a controlled transaction with the conditions that would have been made had the parties been independent and undertaking a

comparable transaction under comparable circumstances.

Required:

Evaluate THREE comparability factors that could be identified in commercial and financial relations between related parties in determining the arm’s length price under transfer pricing. (6 marks)

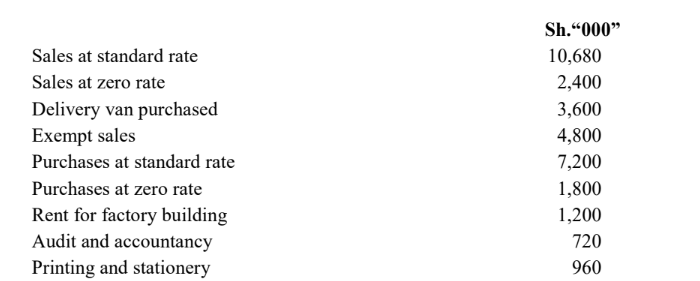

3. Popote Ltd. is a manufacturer of vatable goods and the company is fully registered for value added tax (VAT) purposes. The company had the following transactions for the year ended 31 December 2021 which included VAT at the rate of 16% where applicable.

Additional information:

1. Sales at standard rate include 20% which is in respect of export sales to another country.

2. Purchases at a standard rate include imported vatable raw materials of Sh.1,500,000 exclusive of duty at 25%.

3. The company confirmed that the value of goods purchased at standard rate and sold in the same state amounted to Sh.2,000,000 in the course of the year.

4. Bad debts recovered previously written off amounted to Sh.240,000.

Required:

Compute the following for Popote Ltd. for the year ended 31 December 2021:

Input tax claimable. (6 marks)

Output tax. (1 mark)

VAT payable or refundable. (2 marks)

(Total: 20 marks)