WEDNESDAY: 7 December 2022. Afternoon Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Do NOT write anything on this paper.

QUESTION ONE

1. In the context of environmental management accounting, explain FOUR types of environmental costs. (8 marks)

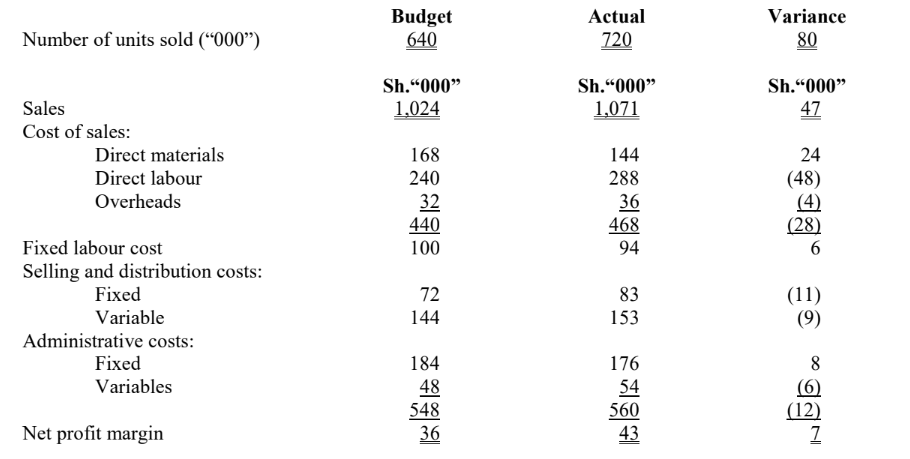

2. Trans Ltd. has provided the following operating statement, which represents an attempt to compare the actual

performance for the quarter which has just ended with the budget:

Required:

Using flexible budgeting approach, redraft the operating statements so as to provide a more realistic indication of the variances. (8 marks)

Discuss TWO problems associated with the forecasting of figures which are to be used in flexible budgeting. (4 marks)

(Total: 20 marks)

QUESTION TWO

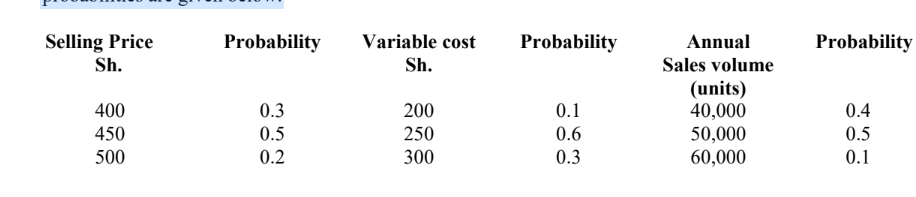

1. Lengo Ltd. is considering marketing a new product. The fixed cost of this product will amount to Sh.5,000,000.

There are three uncertain factors namely; selling price, variable cost and annual sales volume.

The product has a life of only one year and the various possible levels of these factors together with estimated probabilities are given below:

Additional information:

1. Assume that the three factors are statistically independent.

2. The company uses cost-volume-profit (CVP) analysis to make decisions.

3. The following random numbers are provided:

Required

Using CVP analysis criteria, simulate the problem and determine the average profits. (10 marks)

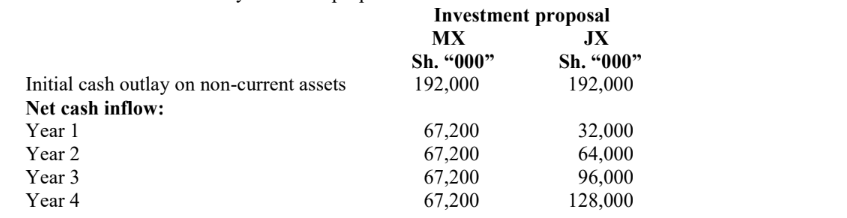

2. Jikaze Ltd. is organised into divisions. Divisional managers are rewarded through a remuneration package which is linked to accounting rate of return (ARR) performance measures. Venus Division of Jikaze Ltd. is currently investigating two mutually exclusive investment proposals namely MX and JX. If the proposals are viable, Venus Division wishes to assign priority in the event that funds may not be available to cover both proposals.

Details of the two mutually exclusive proposals are:

Additional information:

1. The management assesses the cost of capital to the company at 16%.

2. The Accounting Rate of Return (ARR) calculation is based on the accounting profit which is computed by adding back depreciation to net cash inflow of each year.

3. Depreciation is on straight-line basis over the assets’ useful life.

4. Net present value (NPV) method is used to estimate the most viable project when using project life cycle costing.

5. Ignore tax and residual value.

6. The present value interest factor (PVIF) of the proposal is as follows:

Required:

Advise the management of Jikaze Ltd. on the most viable investment proposal using the following performance appraisal measures:

Product life cycle costing. (5 marks)

Accounting rate of return (ARR). (5 marks)

(Total: 20 marks)

QUESTION THREE

1. The complex environment in which most businesses operate today makes it virtually impossible for most firms to be controlled centrally. This is because it is not possible for central management to have all the relevant information and time to determine the detailed plans for all the organisation. Some degree of decentralisation is essential for all but the smallest firms. Organisations decentralise by creating responsibility centres.

Required:

In the context of the above statement, identify FOUR responsibility centres. (8 marks)

2. Maono Ltd. is investigating the financial viability of a new product branded “Zem”. Product Zem is a short life product of six months.

The following estimated information is available in respect of product Zem:

1. Sales should be 10,000 units per month in batches of 100 units on a just-in-time production basis.

2. An average selling price of Sh.120,000 per batch of 100 units is expected for a six-month life cycle.

3. An 80% learning curve will apply for the six months’ life-cycle period.

4. The labour requirement for the first batch in month 1 will be 500 hours at Sh.500 per hour.

5. Variable overhead will be absorbed at a rate of Sh.200 per labour hour.

6. Direct material input will be Sh.50,000 per batch of product Zem for the first 200 batches. The next 200 batches are expected to cost 90% of the initial batch cost. All batches thereafter will cost 90% of the batch cost for each of the second 200 batches.

7. Product Zem will incur directly attributable fixed costs of Sh.1,500,000 per month.

8. The initial investment for the new product will be Sh.7,500,000 with no residual value irrespective of the life of the product.

9. A target cash flow required over the life of the product must be sufficient to provide for a 331 /3% target return for a six-month life cycle.

10. The learning curve formula is Y = axb

Where: Y = Cumulative average time per batch

a = time taken to produce initial batch

x = cumulative units of batches

b = learning curve index

Required:

The learning curve index and model. (4 marks)

Compute the cost gap or cost savings in the target cash flow of product Zem over its six-month life cycle. (8 marks)

(Total: 20 marks)

QUESTION FOUR

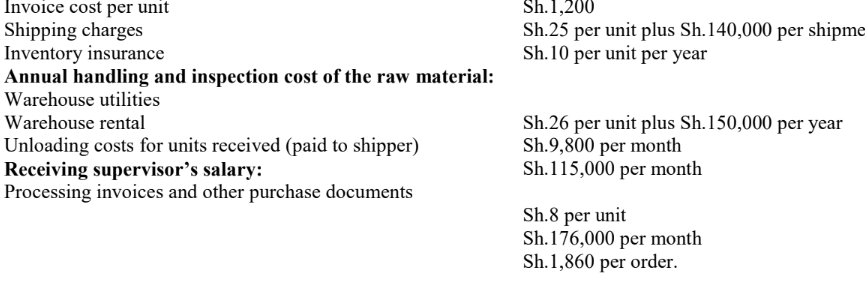

Huruma Ltd. is a client of ABX National Bank. The Managing Director of Huruma Ltd. visited the bank’s offices to seek for an additional line of credit. In the ensuing discussions, the bank credit officer noticed that Huruma Ltd. could save a substantial amount of money by improving on its inventory management.

The credit officer invited the Management Accountant of the company for further consultation. From the conversation, it emerged that the company holds a substantial quantity of a particular raw material in its warehouse. The Management Accountant provided the following information on the raw material:

The company’s policy is to order 5,000 units each time and maintain a safety stock of 3,000 units. The annual demand

for the raw material is 45,000 units. The lead time for an order is 10 working days.

The Management Accountant has also indicated that if there is a stock-out, it would be necessary to obtain the raw

material by a special courier service at an additional cost of Sh.81,000 per stock-out.

The probabilities of a stock-out at various safety stock levels were given as follows:

Additional information:

1. The company’s cost of capital is 10%.

2. You are advised that there are 250 working days in a year.

3. The raw material is ordered in multiples of 250 units.

4. For analysis purposes, a stock-out probability of 0.02 would be reasonable for order cost determination in an optimal inventory policy.

Required:

1. The annual cost of the company’s present inventory policy. (5 marks)

2. Recommend an optimal order quantity for the company based on the information provided. (5 marks)

3. Recommend an optimal safety stock level. (5 marks)

4. Advise the management of the firm on the savings to be realised from the optimal order quantity and optimal safety stock level in (b) and (c) above. (3 marks)

5. The reorder level for the company. (2 marks)

(Total: 20 marks)

QUESTION FIVE

1. Explain THREE conceptual differences between the following concepts as applied in strategic management for short term decision making:

Throughput accounting. (3 marks)

Limiting factor analysis. (3 marks)

2. Timiza Ltd. makes spectacles for a variety of customers. The spectacles pass through several production processes. The first process is fitting and the standard costs for fitting lenses on spectacles are as follows:

Additional information:

1. The overhead allocation rate is based on direct labour hours and comprises an allowance for both fixed and variable overhead costs.

2. With the aid of regression analysis, the fixed element of overhead cost has been estimated at Sh.90,000 per week and the variable overhead costs have been estimated at Sh.6 per direct labour hour.

3. The fitting department comprises its own premises, and all of the department’s overhead costs can be regarded as being the responsibility of divisional managers.

4. In week 5, the division casted 294 spectacles and actual costs incurred were:

5. The 1,520 hours worked by direct labour included 40 hours overtime, which is paid at a rate of 50% above the normal pay rates.

Required:

A reconciliation statement of actual cost and the standard cost. (Show all planning and operating variances). (14 marks)

(Total: 20 marks)