WEDNESDAY: 3 August 2022. Afternoon paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings.

QUESTION ONE

1. The effective use of the control information provided by the management accounting department of an organisation to the operating managers depends on various factors.

Explain four actions that the management accounting department might take to enhance the effective use of the above information by the operating managers. (4 marks)

2. Describe three negative side effects which might arise from the imposition of budgets by senior management and propose ways to deal with them. (6 marks)

3. Many key business performance measures are not effective for most not-for-profit organisations (NPOs). For instance, the “bottom line” measurement of profit or loss indicates how effective a business is at achieving its goals of generating profit for the owners.

However, generating profit is not a goal for NPOs. These organisations have no owners, often provide goods and services to constituents free of charge and typically seek resources from people and organisations that do not expect economic benefit in return. Thus, the bottom line does not work for NPOs.

Required:

In the context of the above statement, evaluate four factors that make planning for NPOs complex. (8 marks)

4. Explain the following measures of divisional performance:

Return on capital employed. (1 mark)

Residual income. (1 mark)

(Total: 20 marks)

QUESTION TWO

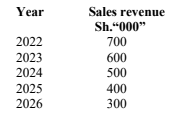

1. The Diamond division of a retailing group has five years remaining on a lease for premises in which it sells self- assembly furniture. The management is considering the investment of Sh.600,000 on immediate improvements to the interior of the premises in order to stimulate sales by creating a more fascinating selling environment.

The following information is available:

1. The forecast of the increase in sales revenue per annum from the premises is as follows:

2. The average contribution to sales ratio is expected to be 40%.

3. The cost of capital is 16% on the net book values of the investment at the beginning of the year.

4. At the end of the five-year period, the premises improvements will have nil residual value.

5. Depreciation is charged on straight line basis.

6. The Diamond division has a target return on capital employed of 20%.

Required:

Prepare summary performance statement for the years 2022 to 2026 showing:

Residual income (RI). (7 marks)

Return on investment (ROI). (7 marks)

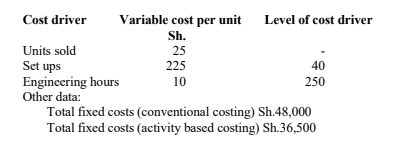

2. A manufacturing company produces Ball Pens that are printed with logos of various companies. Each pen is priced at Sh.50. Production costs are as follows:

Required:

Compute the break-even point using Activity Based Analysis. (6 marks)

(Total: 20 marks)

QUESTION THREE

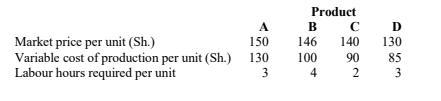

1. Division X is a profit centre which produces four products namely; A, B, C and D. Each product is also sold in the external market.

The data for the period ended 30 June 2022 is as follows:

Additional information:

1. Product D can be transferred to Division Y, but the maximum quantity that may be required for transfer is 2,500 units only.

2. The maximum sales in the external market are as follows:

Units

A 2,800

B 2,500

C 2,300

D 1,600

3. Division Y can purchase the same product at a price of Sh.125 per unit from external suppliers instead of receiving transfer of product D from Division X.

Required:

The transfer price for each of the 2,500 units of product D, if the total labour hours available in Division X are 20,000 hours. (10 marks)

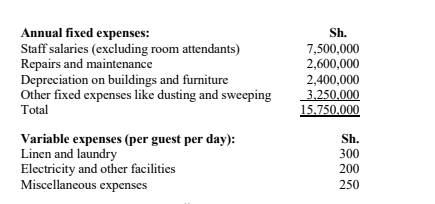

2. A hotel with 50 single rooms is recording 80% occupancy in normal season (8 months) and 50% occupancy in off- season (4 months) in a year.

The following information is provided:

The management wishes to realise a profit of 25% on total cost.

Assume a 30 day month in all cases.

Required:

The required tariff rate per room. (4 marks)

The break-even occupancy in normal season assuming 50% occupancy in off-season. (3 marks)

The management is proposing a 20% decrease in tariff to improve occupancy at 100% and 70% in normal season and off-season respectively.

Advise on the appropriateness or otherwise of the above proposal. (3 marks)

(Total: 20 marks)

QUESTION FOUR

1. Explain three areas where environmental management accounting (EMA) might be applied. (3 marks)

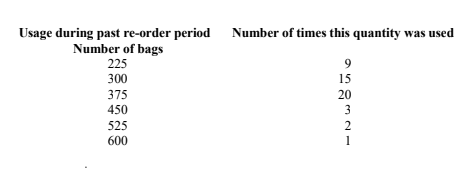

2.Mwamba County water-treatment plant purchases 100 kgs of lime bags for use in the water treatment process. The number of bags used per day varies on the basis of water consumption. Examination of past records discloses the following data:

The economic order quantity (EOQ) has been established at 2,500 units with an average daily usage of 25 bags and a lead time of 15 days for its single product X.

Additional information:

1. Stock-out cost is Sh.300 per bag.

2. The optimum number of orders based on the EOQ model is 6 times per annum.

3. The normal carrying cost is Sh.50 per bag.

Required:

Advise the management accountant of Mwamba County on the desired level of safety stock in order to minimise the total inventory cost. (6 marks)

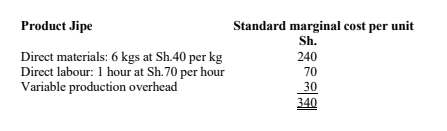

3. Ukunda Ltd. operates a standard marginal cost accounting system. Information relating to product Jipe, which is made in one of the company’s departments, is given below:

Additional information:

1. Variable production overheads vary with units produced.

2. Budgeted fixed production overhead per month amount to Sh.1,000,000.

3. The budgeted production for product Jipe amounted to 20,000 units per month.

4. Actual production and costs for the month of June 2022 were as follows:

Required:

Prepare in columnar form a statement showing:

1. Original budget by element of cost. (2 marks)

2. Flexed budget by element of cost. (2 marks)

3. Actual production statement by element of cost. (2 marks)

4. A reconciliation of the actual production cost with the budgeted production cost. (5 marks)

(Total: 20 marks)

QUESTION FIVE

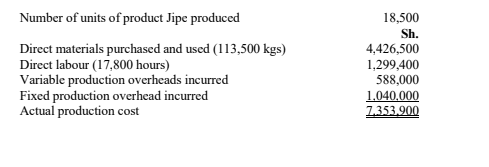

1. The table below shows Safaris Airline Ltd.’s framework to lay out its balanced scorecard model:

Required:

Identify the balanced scorecard perspectives S1, S2, S3 and S4 above. (4 marks)

For the mentioned perspectives, state one performance measure labelled M1 and M2. (2 marks)

Explain initiatives J and K that Safaris Airlines Ltd. should excel in, in order to meet objectives and create value. (2 marks)

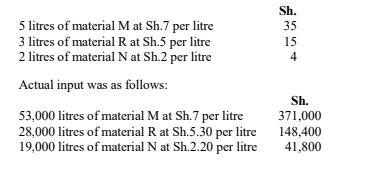

2. Moran Ltd. has established the following standard mix of producing 9 litres of product “MRN”:

Additional information:

1. A standard loss of 10% of the input is expected to occur.

2. Actual output for the period was 92,700 litres of product MRN.

Required:

Compute and interpret the following variances:

Material price variance. (3 marks)

Material mix variance. (3 marks)

Material yield variance. (3 marks)

Material usage variance. (3 marks)

(Total: 20 marks)