MATCHING SUPPLY AND DEMAND

Definition of terms:

- Supplies: The term supplies refers to all the materials, goods and services used in the enterprise regardless of whether they are purchased outside, transferred from another branch of the company or manufactured in-house.

- Demand: Refers to an urgent or peremptory requirement or request. Demand may be either independent or dependent. Independent demand for an item is influenced by market conditions and not related production decisions for any other item held in stock. In manufacturing only end items i.e. the final product sold to customer, have exclusively independent demand. An item is said to have dependent demand if the demand for it is dependent upon the demand for another item. For instance demand for tyres to be used in a car assembly plant is dependent upon the number of cars that are to be produced.

- Inventory: This is an American accounting term for the value or quantity of raw materials, components, assemblies, consumables, work in progress (WIP) and finished stock that are kept or stored for use as the need arises.

- Inventory (or stock) control: Refers to the techniques used to ensure that stocks of raw materials or other supplies, work in progress and finished goods are kept at all levels which provide maximum service levels at minimum costs.

Inventory control methods:

There are two basic approaches on which inventory; control systems both manual and automatic are based. These are: the action level method and the periodic review approach.

- The action level method (Fixed order quantity): The action level method of controlling inventory is way of fixing each commodity and stock levels that are recorded in the stock control system and subsequently used as a means of indicating when some action is necessary. There are various kinds of stock levels, but the fundamental controls are: ordering, hastening and maximum levels. In order to keep abreast with the changing conditions after stock level have been established, they should be carefully reviewed at suitable intervals e.g. quarterly, monthly or weekly and should be adjusted to meet any changes as circumstances may require.

Advantages of fixed order point:

- On average, stocks are lower than with the periodic system

- Economic order quantity are applicable

- Enhanced responsiveness to demand fluctuations

- Appropriate for widely differing inventory categories

- Replenishment orders are automatically generated at the appropriate time by comparison of actual stock levels against re order levels

Disadvantages of fixed order point:

- The re-ordering system may become overloaded if many items of inventory reach re-order level at the same time

- Leads to random re-ordering pattern thus increasing ordering costs

2) The periodic review system: In this system an item’s inventory position is reviewed periodically rather than at a fixed order point. The periods or intervals at which stock levels are reviewed will depend on the importance of the stock item and the costs of holding that item. A variable quantity will be ordered at each review to bring the stock level back to maximum. Maximum stock can be determined by adding one review period to the lead time, multiplying the sum by the average rate of usage and adding any safety stock. This can be expressed as:

M-W (T+L) +S

Where: M= Pre-determined stock level

W= Average rate of stock usage

T= Review periods

L= Lead time

S= safety stock

Advantages of periodic review system:

- Greater chance of elimination of obsolete items owing to periodic review of stock

- The purchasing load may be spread with possible economies in placing orders

- Large quantity discounts may be negotiated

- Production economies due to more efficient production planning and lower set-up costs may result from orders always being in the same sequence

Disadvantages of periodic review system:

- On average, larger stocks are required than with fixed order point system

- Re-order quantities are not based on economic order quantities (EOQ).

- If the usage rate changes shortly after a review period, a stock-out may occur before the next review date

- Difficulties in determining appropriate review period unless demands are reasonably consistent.

- Material requirement planning (MRP1): This is a product- oriented computerized technique aimed at minimizing inventory and maintaining delivery schedules. It relates the dependent requirements for the materials and components comprising an end product to time periods known as ‘buckets’ over a planned horizon (typically of one year) on the basis of forecasts provided by marketing and sales and other input information.

While having elements common to all inventory situations, MRP 1 is most applicable where:

- The demand for items is dependent

- The demand is discontinuous that is ‘Lumpy’ and non-uniform

- In the job, batch and assembly or flow production or where all manufacturing methods are used

The aims of material requirement planning:

- To synchronize ordering and delivery of materials and components with production requirements

- To achieve planned and controlled inventories and ensure that required items are available at the time of usage or not much earlier

- To promote planning between the purchaser and the supplier to the advantage of each

- To enable rapid action to be taken to overcome material or component shortages due to emergencies, late deliveries etc

- Material resource planning (MRP 11): This is concerned with virtually any resource entering into production including manpower, machines and money in addition to materials. MRP 11 is an expanded system of MRP 1 which has to new capabilities that are first, financial interface which provides the ability to convert operating production plans into financial terms so that the data can be used for financial planning and control purposes of a more general management nature, then secondly provision of a simulation of capability that makes it possible for management to do more extensive alternative planning work in developing the marketing and the business plans. MRP 11 is concerned to be more comprehensive when compared with MRP 1 and many users MRP 11 as the umbrella system while MRP 1 as the major component of MRP 11.

- Distribution requirements planning (DRP): This is an inventory control and scheduling technique that applies MRP principles to distribution inventories. It may also be regarded as a method of handling stock replenishment in a multi-echelon environment. An echelon is defined by chambers dictionary as: a stepwise arrangement of troops, ships, planes etc. Applied to distribution the term multi-echelon means that instead of independent control of the same item at different distribution points using EOQ formulae, the dependent demand at higher echelon (e.g. a central warehouse) is derived from the requirements of lower echelons e.g. regional and local distributions and purely merchandizing organizations e.g. supermarkets.

6) Just-in-time system: This is an inventory control philosophy whose goal is to maintain just enough material in just the right place at just the right time to make just the right amount of product. For JIT to work two things must be happening that are:

(a) all parts must arrive where they are needed, when they are needed and in the exact quantity needed

(b) all parts that arrive must be usable parts. In achieving these requirements, purchasing has the following responsibilities:

- Liaison with the design function

- Liaison with suppliers

- Investigating of the potential suppliers within reasonable proximity of the purchaser to increase certainty of delivery and reduction of lead time.

- Establishing strong, long-term relationships with suppliers in a mutual effort to reduce costs and share savings

- Establishment of an effective supplier certification programme which ensures that quality specifications are met before components leave the supplier so that receiving inspections are eliminated.

- Evaluation of supplier performance and the solving of difficulties as an exercise in cooperation.

Benefits of Just-in-time:

- Quality– fast detection and correction of unsatisfactory quality and ultimately higher quality in purchased parts

- Design– fast response to engineering change requirements

- Productivity- reduced rework, reduced inspection, reduced parts related delays

- Capital requirements– reduced inventories of purchased parts, raw materials, work in progress and finished goods

- Part costs– low scrap costs; low inventory carrying costs

- Administrative efficiency: fewer suppliers, minimal expending and order release work; simplified communications and receiving activities.

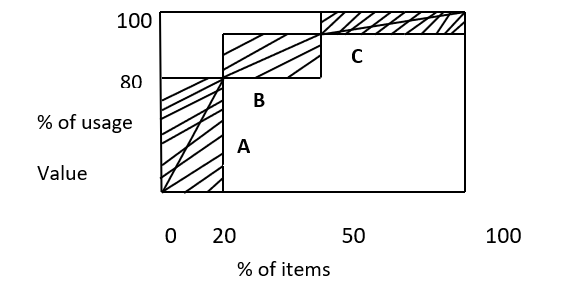

- ABC analysis: This is application to stock holding. ABC analysis shows that the high inventory is normally represented by relative few items and vice versa. While the percentage varies between organisations setup, the following presentation shows a proportion of how inventory is segmented:

Category (Usage) Approximate % of inventory Approximate % of usage value

A-High value 10% 60%

B-Moderate value 30% 30%

C-Low value 60% 10%

Category A: These are items which are small in number and high in value. They are essential to the operation of the production such that the absence of such materials can result to breakdown of pro duction.

Category B: They are medium in number and have medium usage value.

Category C: They are high in number and low in usage value. The absence of such items in the short-time cannot affect the performance of the company.

Conducting the ABC analysis:

It involves the following steps:

- Calculate the annual usage value of each stock item

- Rank the items in descending order of usage value i.e. from the most valuable to the least

- Prepare sub-totals of each usage value beginning with the biggest

- Plot a pareto curve

- Insert the ABC break points

The ABC curve:

Enterprise resource planning (ERP): This is a business management system that is supported by multi-module application software that integrates all the department’s functions of an enterprise. It is the latest and possibly the most significant development of MRP 1 and MRP 11. While MRP allows the manufacturers to track supplies, work in progress and the output of finished goods to meet sales orders, ERP is applicable to all organisations and allows managers from all functions or departments to have a consolidated view of what is or is not taking place throughout the enterprise. Most ERP systems are designed around a number of modules each of which can be stand-alone or can be combined with others.

Advantages of Enterprise resource planning:

- Faster inventory turn-over-manufacturers and distributors may increase inventory turns by tenfold and reduce inventory cost by 10 % to 40 %

- Improved customer service: In many cases an ERP system increase fill rates to 80 % or 90 % by providing the right product in the right place at the right time thus increasing customer satisfaction

- Better inventory accuracy, fewer audits: An ERP system can increase inventory accuracy to more than 90 % while reducing the need for fewer physical inventory audits

- Reduced set up times: ERP can reduce set up time by 25 % to 80 % by grouping similar production jobs together with the efficient use of equipment and minimizing down time through efficient maintenance

- Higher quality work: ERP software with a strong manufacturing component proactively pin points quality issues providing the information required to increase production efficiency and reduce or eliminate re-work

- Timely revenue collection and improved cash flow: ERP gives manufacturers the power to proactively examine accounts receivable before problems occur instead of just reacting. This improves cash-flow.

Disadvantages of enterprise resource planning:

- ERP implementation is difficult:

This is because implementation involves a fundamental change from a functional to a process approach to business

- ERP systems are expensive:

This is especially so when the customization of standard modules to accommodate different business process is involved

- Cost of training employees to use ERP can be high

- There may be a number of un intended consequences such as employees stress and resistance to change and the sharing of information that was closely guarded by departments or functions

- ERP systems tend to focus on operational decisions and have relatively weak analytical capabilities